Market liberals assume that people can look after themselves. But much of the time they cannot. Dependency on others is inevitable during motherhood, infancy and childhood, education, illness, disability, unemployment, and old age. There may be no agency, no two feet to stand on, nothing to sell, no bargaining power and limited cognitive capacity. The welfare challenge is not primarily redistribution, but dependency over the life cycle.

The market solution is for individuals to transfer money to themselves over the life cycle by means of savings and insurance. In contrast, social democracy pools the risks for society as a whole. Transfers are made in the present from producers to dependents, by means of progressive taxation. Between the 1920s and 1970s this social democratic solution prevailed, as public expenditure more than doubled in most countries up to levels close to 50 per cent of GDP. It has largely stayed there.

Since the 1980s, property ownership has been held out as an alternative source of economic security. A new financial innovation came to the fore. It took the form of household debt rising threefold from about 50 per cent of income to some three times as much in the UK (and similar increases elsewhere), with most of it invested in housing. There are two stories to tell about this innovation: money and housing.

Money first. The strategy of household debt was facilitated by the end of the Bretton Woods system of fixed exchange rates. In 1971 the Bank of England set lenders free. This reform was abortive and culminated in a banking crisis. In the 1980s the Conservative government liberalised credit again, especially for housing, and terminated the building society monopoly of mortgage lending. These mutual societies had rationed credit since they could only lend their shareholders’ deposits. In contrast, banks could extend loans at the stroke of a pen to borrowers with housing collateral and other good security. Between 1980 and 2008 UK bank assets increased tenfold as a proportion of national income. Domestic borrowing rose fourfold from about one half of GDP to more than 200 per cent, with similar increases in the European Union and the US. Household debt rose about threefold in the UK and by similar magnitudes in other OECD countries.

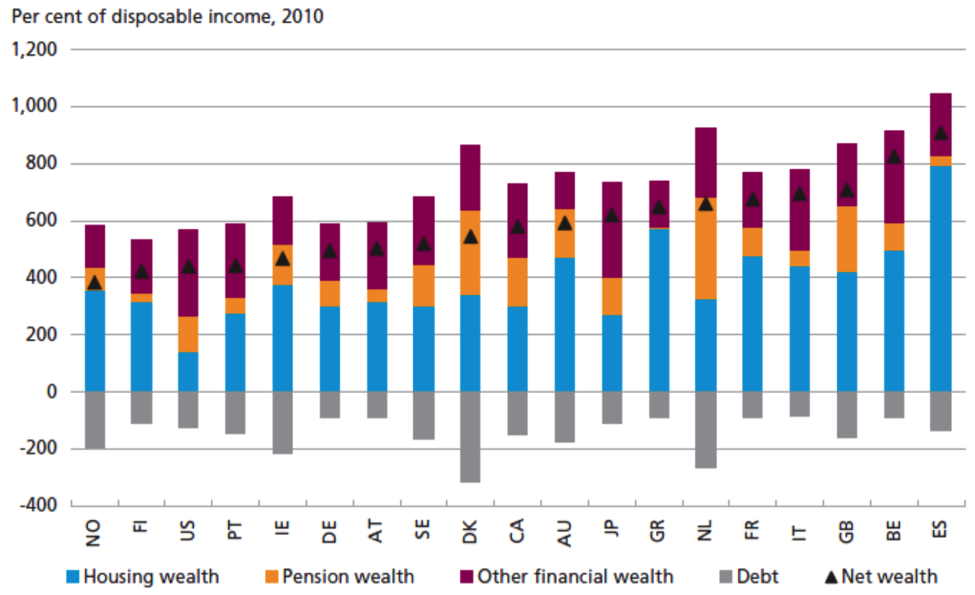

This debt paid off handsomely for borrowers. The aggregate of housing wealth was much larger than the debt (figure 1).

Figure 1. Household wealth and gross debt, selected OECD countries, 2011.

Source: Jakob Isaksen et al., ‘Household balance sheets and debt – an international country study – part 2’, Danmarks Nationalbank Monetary Review, 4th Quarter 2011, p. 52.

In figure 1, the bottom part of the columns (in grey, below the zero line) represents household debt. The blue segment above it is housing wealth, which rose as debt was paid down over time. The next segment up (in orange) is pension wealth. The top one, made up mostly of financial wealth is a balancing item for debt, and most of it is held by a small minority.

Housing credit gave rise to a property windfall society. In the quest for economic security, the best personal strategy is to be rich. Housing held out the promise of financial security as a complement to social insurance. It may even be regarded as the next progressive innovation beyond social insurance.

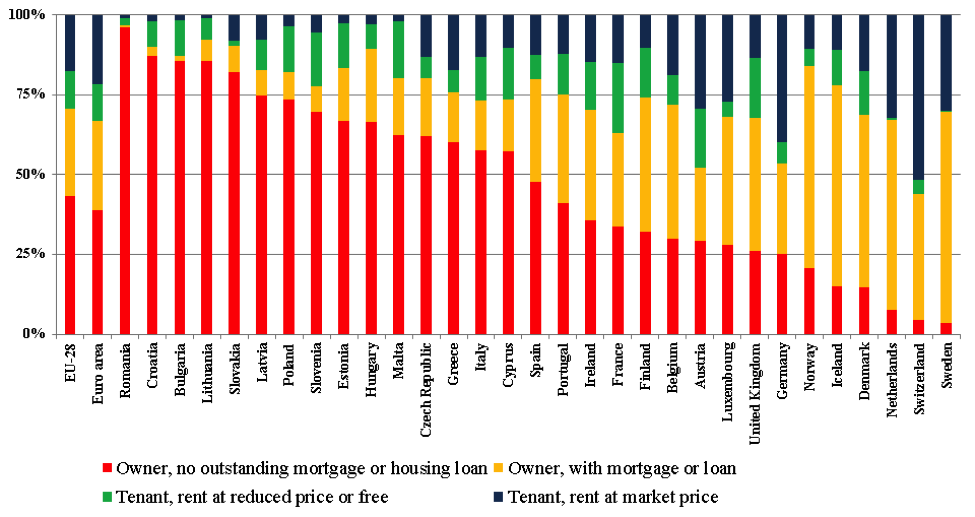

The quest for owner-occupation of housing was underpinned by political majorities and bi-partisan consensus. Typically more than half of all households signed up for owner occupation (figure 2). It is a curiosity that the highest levels of owner occupation can be found in the successor countries of the Soviet bloc, due perhaps to the way in which housing was privatised. Elsewhere the proportion of fully paid-off ownership was never more than half, and only about a quarter in the UK. This fraction of households gained the most.

Figure 2. Percentage of households in different tenures, Europe 2011.

Source: Eurostat, http://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=ilc_lvho02&lang=e. Figure in Offer, ‘The market turn’, p. 18, fig. 5.

Early movers did best. The ‘great moderation’ of low inflation and interest rates since the 1980s acted automatically to raise house prices. Ample credit gradually pushed prices up and beyond the reach of low earners. A social divide opened up between those on the property ladder and those unable to attain it. A new ‘generation rent’ suffered insecure, expensive and inadequate housing with little hope of ownership except by means of bequest.

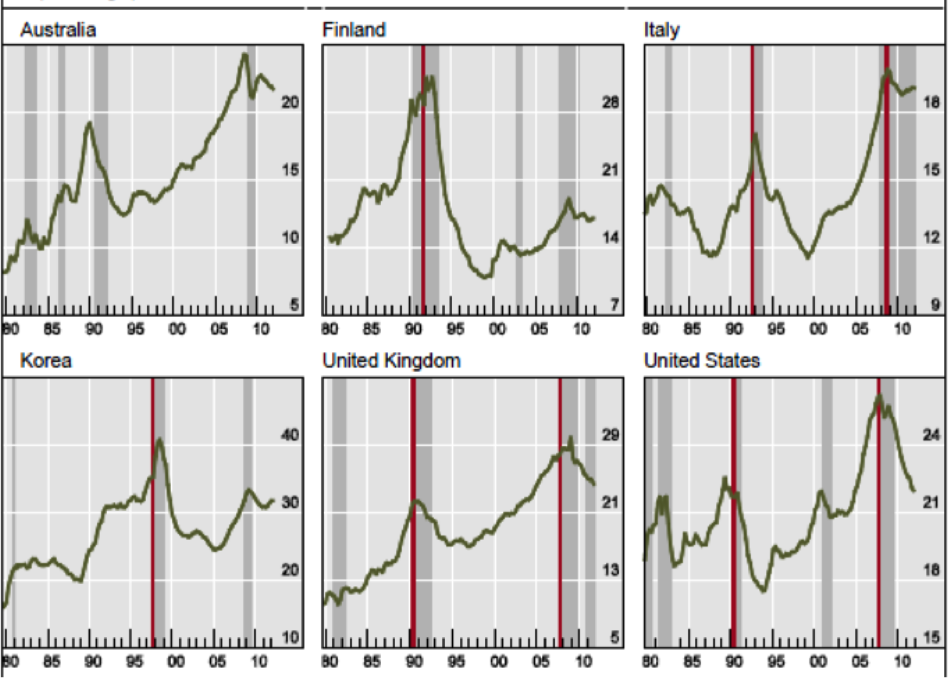

When economic growth is less than the average level of debt service, debt repayment captures an ever-growing share of output, reducing the payoffs to work and enterprise, and contracting overall demand. In figure 3 below, high debt service appears to trigger financial crises.

Figure 3. Debt ratios as percentage of private sector non-finance income. (Vertical lines and strips indicate financial crises).

Source: Mathias Drehmann and Mikael Juselius, ‘Do debt service costs affect macroeconomic and financial stability?’, BIS Quarterly Review (Sept. 2012), graph 1, p. 26.

Both social democracy and market liberalism are currently in crisis. The immediate problem is debt overhang and the long-term one is to prevent its recurrence. Both call for drastic action. Debt reduction may be achieved by monetary expansion or debt write-offs. Central banks have applied these measures without much effect. Another remedy, higher capital requirements for the banks, has not been effective in the past. In a boom it is easy to raise capital, and during slumps the benefit is limited by the scale of bad loans.

Rationing credit away from financial speculation might help, as well as the massive construction of affordable housing. The argument that rigid planning inhibits housebuilding requires a proper estimate of all the putative costs and benefits. There is a choice between drastic action now and a drastic crisis later. Action is hard, and the choice appears to be for a drastic crisis later.

♣♣♣

Notes:

- This blog post is based on the authors’ paper “The market turn: from social democracy to market liberalism“, Economic History Review vol. 70, 4 (2017), pp. 1051-1071. Discussion paper version.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: St George Wharf, by Mariano Mantel, under a CC-BY-NC-2.0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Avner Offer is Chichele Professor of Economic History, Emeritus and Fellow of All Souls College at the University of Oxford. His most recent book is The Nobel Factor: The Prize in Economics, Social Democracy, and the Market Turn, co-authored with

Avner Offer is Chichele Professor of Economic History, Emeritus and Fellow of All Souls College at the University of Oxford. His most recent book is The Nobel Factor: The Prize in Economics, Social Democracy, and the Market Turn, co-authored with