Cryptocurrencies have been a staple of news headlines in 2017. As the price of one bitcoin has risen 12-fold in sterling terms during the course of 2017, the number of Google searches for bitcoin has increased 14-fold. There are now more than 2,000 cryptocurrency ATMs across the globe, with the United States (1,107), Canada (293), the UK (97) and Austria (91) leading the way.

A great deal has been written about bitcoin, in many cases speculating on whether there is a bubble in its price and what might happen if and when the bubble bursts. A Google search for ‘bitcoin bubble’ produces 17.8 million page hits. This survey eschews the bubble question and asks instead whether cryptocurrencies are a threat to the financial system and therefore deserving of greater regulatory oversight by policy-makers.

Cryptocurrencies and the financial system

In 2012, a working paper published by the European Central Bank (ECB) concluded that, in the current situation, virtual currency schemes: ‘do not pose a risk to price stability, provided that money creation continues to stay at a low level; [and] tend to be inherently unstable, but cannot jeopardise financial stability, owing to their limited connection with the real economy, their low volume traded and a lack of wider user acceptance.’

The ECB returned to the theme in a working paper in 2015: ‘For the tasks of the ECB as regards monetary policy and price stability, financial stability, promoting the smooth operation of payment systems, and prudential supervision, the materialisation of risks depends on the volume of virtual currency issued, their connection to the real economy – including through supervised institutions involved with virtual currencies – their traded volume and user acceptance. For the moment, all these risk drivers have remained low, which implies that there is no material risk for any of the central bank’s tasks as yet.’

The main argument of the ECB and other central banks is that cryptocurrencies are too small and too detached from other financial markets to be a systemic risk. As reported by the Wall Street Journal, the top 1,000 or so cryptocurrencies are worth $350 billion, less than Facebook Inc., and if they all went to zero tomorrow, banks would barely notice.

One reason for cryptocurrencies remaining small is current technological constraints, which show up as high transaction fees and limit the use of cryptocurrencies as a medium of exchange. The maximum seven-transactions-per-second capacity of bitcoin compares with a peak processing capacity of 47,000 transactions per second at Visa. Chiu and Koeppl (2017) estimate that the current bitcoin scheme generates a flow welfare loss of 1.4 per cent of consumption in a general equilibrium monetary model.

A less sanguine view is that bitcoin’s increasing market capitalisation and trading volumes reflect accelerating professionalisation of investment in cryptocurrency markets, leading to a disruption of financial markets that poses risks for the stability of prices and the financial system.

In the latest evidence that cryptocurrencies are pushing deeper into the mainstream, recent months have seen asset management company Tobam launching Europe’s first bitcoin mutual fund and US regulators giving the green light for two of the world’s largest futures exchanges – the Chicago Mercantile Exchange (CME) and the Chicago Board Options Exchange (CBOE) – to list futures contracts on bitcoin.

Concerns about bearing the risks of uncovered short selling in cryptocurrency markets have been expressed by the Futures Industry Association, a lobby group representing some of the world’s largest brokers, including Goldman Sachs, Morgan Stanley, J.P. Morgan and Citigroup.

Some authors see cryptocurrencies entering the mainstream markets as beneficial to the stability of the financial system. Dyhrberg (2016) explores the financial asset capabilities of bitcoin in GARCH models and finds that it may be useful in risk management and ideal for risk-averse investors. She classifies bitcoin as somewhere between gold and the US dollar in terms of its use as a medium of exchange and a store of value.

Bianchi (2017) finds a similar relationship between returns on cryptocurrencies and commodities such as gold and energy, consistent with existing models in which trading is primarily driven by investor sentiment.

The first question of the latest CFM-CEPR expert survey asked panel members the following:

Question 1: Do you agree that cryptocurrencies are currently a threat to the stability of the financial system, or can be expected to become a threat in the next couple of years?

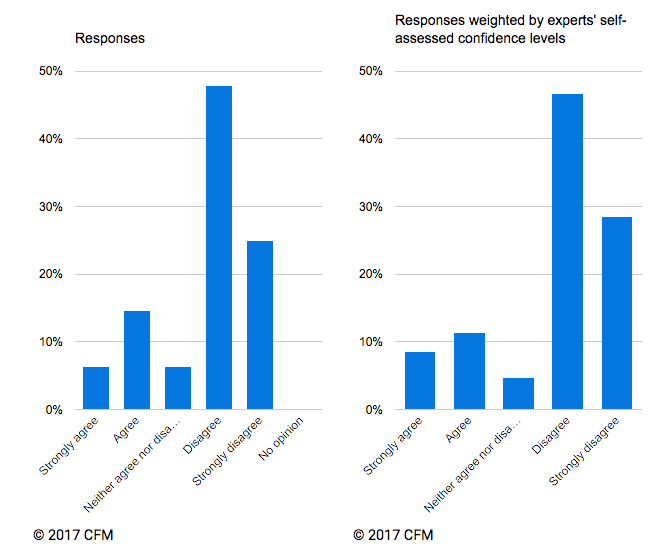

Forty-eight panel members answered this question. A large majority did not see cryptocurrencies as posing a threat to financial stability either now or in the next couple of years: 71 per cent of respondents either disagree or strongly disagree with the statement; 23 per cent either agree or strongly agree; and 6 per cent neither agree nor disagree. Those who disagree are the most confident in their assessments, raising the proportion of panel members disagreeing or strongly disagreeing to 73 per cent when responses are weighted by self-reported confidence.

Forty-eight panel members answered this question. A large majority did not see cryptocurrencies as posing a threat to financial stability either now or in the next couple of years: 71 per cent of respondents either disagree or strongly disagree with the statement; 23 per cent either agree or strongly agree; and 6 per cent neither agree nor disagree. Those who disagree are the most confident in their assessments, raising the proportion of panel members disagreeing or strongly disagreeing to 73 per cent when responses are weighted by self-reported confidence.

A common argument of those who disagree with the statement is that the total value of cryptocurrencies is too small to be a systemic risk to financial stability. As Robert Kollman (Université Libre de Bruxelles) puts it, ‘Despite recent growth, the market cap of cryptocurrencies remains modest, compared to the size of “conventional” financial markets. Hence, cryptocurrencies do not seem to represent a threat to financial stability – for now.’

Jordi Galí (Universitat Pompeu Fabra) is similarly relaxed, neither agreeing or disagreeing with the statement, while contending that ‘It depends on the volumes they end up representing relative to the size of the economy and the characteristics (e.g. degree of leverage) of their holders. In their current state they seem largely innocuous for financial stability.’

Many of those who disagree with the statement believe that the financial system is largely insulated from developments in cryptocurrency markets. Michael McMahon (University of Oxford) thinks cryptocurrencies are ‘still too small and lacking in widespread ownership, especially among large investment groups, to be a serious risk to the overall financial system’; and Ethan Ilzetzki (London School of Economics) asserts that at this point ‘bitcoin and other cryptocurrencies remain a toy for a very narrow segment of investors and are detached from the financial system and the real economy.’

A note of caution is sounded by Wouter den Haan (LSE), who in agreeing with the statement recalls that ‘The LTCM crisis has taught us that it takes just one key financial institution taking on large risky positions to put the system at risk.’

In justifying why they disagree with the statement, Richard Portes (London Business School) argues that ‘cryptocurrencies have few attributes of money’; and Ricardo Reis (LSE) points out that ‘Bitcoin is inadequate as a currency.’ The latter sees cryptocurrencies as no more a threat to financial stability than gold, saying that ‘Like gold, [bitcoin] fluctuates wildly in value and it is subject to fads and manias. As long as regulators treat it as a highly speculative investment, like so many other investments out there, then it should pose as much risk to the financial system as so many of these do.’

Those who agree with the statement stress the unprecedented uncertainties surrounding the future of cryptocurrencies. Etienne Wasmer (Sciences Po, Paris) worries that ‘this is radical uncertainty, nothing close in history as far as I can tell’, while Stefan Gerlach (BSI Bank, Switzerland) warns that ‘Cryptocurrencies are currently not a threat to the financial system but could very well become a serious concern in the near future if they become more important.’

Some of those who disagree with the statement accept that cryptocurrencies may eventually threaten the stability of the financial system. While David Smith (Sunday Times) believes that cryptocurrencies only have limited ability to damage the financial system now, ‘That will change, though not over the next two years.’ Tony Yates (longandvariable blog) is similarly unconvinced of the current threat but suggests that, ‘I doubt the situation would change much in two years. Perhaps in 10.’

Jürgen von Hagen (Universität Bonn) has a different reason for strongly disagreeing with the statement, maintaining that causation may run from instabilities in the financial system to the use of cryptocurrencies rather than the other way around. He does not consider cryptocurrencies as a threat to stability, writing ‘The financial system is still based on currencies issued by central banks. Cryptocurrencies would become attractive if central bank issued currencies became very unstable. Their widespread use in the financial system would be a result not a cause of instability.’

Cryptocurrencies and economic policy

Bitcoin is currently classified as a commodity in the United States, so its trading is covered by the Commodity Exchange Act and overseen by the Commodity Futures Trading Commission. In common with other commodities such as gold or oil, there is no traditional management structure behind cryptocurrencies. They are typically launched through an ‘initial coin offering’ (ICO), which allows investors to purchase cryptocurrencies in advance, an arrangement similar in spirit to an initial public offering (IPO) but bypassing the rigorous capital-raising process required by venture capitalists or financial intermediaries.

Bianchi (2017) ultimately sees holding bitcoin as investing in the blockchain technology, since it shares more similarities with equity investment in a company than investments in traditional fiat currencies.

The UK and other European Union (EU) governments are responding to concerns that cryptocurrencies are being used for money laundering and tax evasion. In the UK, the Treasury will bring regulation on cryptocurrencies in line with anti-money laundering and counter-terrorism financial legislation. Anonymity will be lost as traders are forced to disclose their identities.

The EU plan will require online cryptocurrency trading platforms to carry out due diligence on customers and report suspicious transactions. In her speech at the conference to mark 20 years of independence of the Bank of England, Christine Lagarde proposed the International Monetary Fund as the ideal platform to coordinate regulatory policy on new models of financial intermediation.

If the current interest in cryptocurrencies is a precursor to their wider use as alternatives to the dollar, the pound, the euro and the yen, then this may threaten the monopoly on money creation that is held by policy-makers. Central banks cannot print bitcoins, so if the world switches away from fiat currencies, then they would be unable to print money to stimulate the economy. Conventional monetary policy would be ineffective, as would quantitative easing.

According to this argument, increased regulation of cryptocurrencies is needed so that central banks do not lose control of the money supply. Tony Yates, who was formerly a Bank of England economist, as well as former president of the Bundesbank Axel Weber, doubt that this would a problem, arguing instead that cryptocurrencies will fail to take off because they lack any ‘lender of last resort’ function. There will always be boom and bust in cryptocurrencies, unlike for fiat currencies backed by central banks as lender of last resort.

Supporters of cryptocurrencies argue that the lack of regulation has been instrumental in their successes to date, often presenting cryptocurrencies as the digital version of the nineteenth century gold standard when no attempt was made to equate the supply of money with demand.

A working paper from the Bank of Finland in 2017 concludes that bitcoin cannot be regulated and does not need to be regulated in any case. Regulation is appropriate for monopolies run by management organisations, but not for monopolies run by protocols. Speaking at a press conference in October 2017, ECB president Mario Draghi reasoned that cryptocurrencies are not mature enough to be considered for regulation, although they should be critically assessed for risk.

The second question of the latest CFM-CEPR expert survey asked panel members the following:

Question 2: Do you agree that the regulatory oversight of cryptocurrencies needs to be increased?

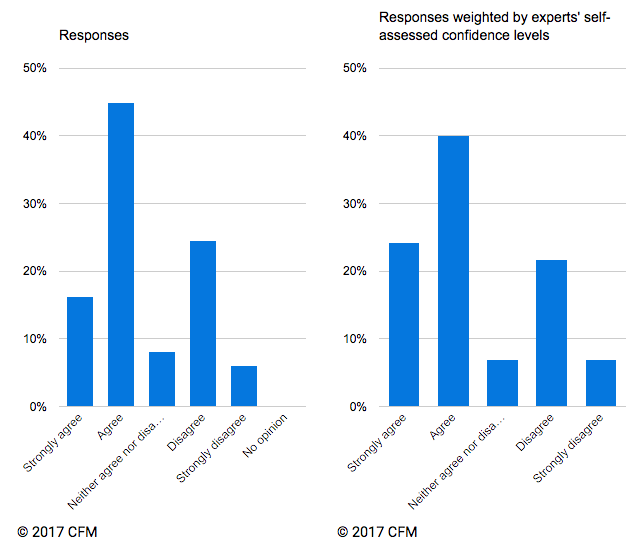

Forty-nine panel members answered this question. A clear majority wished to see greater regulation of cryptocurrencies: 61 per cent of respondents either agree or strongly agree with the statement; 31 per cent either disagree or strongly disagree; and 8 per cent neither agree nor disagree. Those who agree are most confident in their assessments, raising the proportion of panel members agreeing or strongly agreeing to 73 per cent and decreasing the proportion disagreeing or strongly disagreeing to 29 per cent when responses are weighted by self-reported confidence.

The most common reason for agreeing with the statement is a concern that the anonymity of cryptocurrencies promotes nefarious activities. Fabrizio Coricelli (Paris School of Economics) is worried about the ‘likely use of bitcoin for recycling revenues from illegal transactions’; while Franck Portier (University College London) advocates greater oversight of cryptocurrencies because ‘as cash, they are used for tax evasion and criminal activities.’

For Nicholas Oulton (LSE), cryptocurrencies should be subject to additional supervision because ‘One strand of current policy is to crack down on money laundering and tax evasion through tax havens. So it would seem odd to let cryptocurrencies get around these restrictions.’

There is some support for increased regulatory oversight to preserve the effectiveness of monetary policy, although this is far from being a widespread belief among respondents. Sylvester Eijffinger (Tilburg University) agrees with the statement because he sees cryptocurrencies as ‘undermining the monopoly of money creation by the central banks and [leading to] the ineffectiveness of conventional and unconventional monetary policy.’

But Pietro Reichlin (Università LUISS G. Carli) disagrees, arguing that the power of monetary policy may not be affected by cryptocurrencies because ‘Central Banks (or governments) are the only authorities able to provide the fiscal backing required to offer safe assets and generate lender of last resort type of policies.’ He concludes that more oversight is unnecessary ‘as long as bitcoin holders are aware of what [the] risks are.’

Thorsten Beck (Cass Business School) also disagrees with the statement, but recommends a cautious approach in which ‘regulators should carefully watch the development’ and there is ‘careful monitoring of “this space”.’

A different argument for disagreeing with the statement is provided by Jon Hassler (Stockholm University), who is worried that ‘there is a risk that regulatory oversight may create a perception that cryptocurrencies are legitimate investments. They should not be perceived like that.’

Jürgen von Hagen (Universität Bonn) goes further in defending cryptocurrencies by asking ‘What is the point of a privately issued currency regulated by the government? Such currencies are created to avoid the supposed evil effects of government regulation on monetary and financial stability.’ Francesco Lippi (Università di Sassari) doubts that regulation would be possible in any case, concluding that ‘None of the arguments… proves more regulation is desirable, nor that it would be effective.’

♣♣♣

Notes:

- This blog post is based on Bitcoin and the City, a survey of the Centre for Macroeconomics (CFM).

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Bitcoin, by tombark, under a CC0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Wouter Den Haan is Professor of Economics at LSE and Co-Director of the Centre for Macroeconomics. HIs main research interests are in macroeconomics, the role of frictions in financial and labour markets for business cycles, business cycle models with heterogeneous agents and computational economics. He holds a PhD in Economics from Carnegie Mellon University.

Wouter Den Haan is Professor of Economics at LSE and Co-Director of the Centre for Macroeconomics. HIs main research interests are in macroeconomics, the role of frictions in financial and labour markets for business cycles, business cycle models with heterogeneous agents and computational economics. He holds a PhD in Economics from Carnegie Mellon University.

Ethan Ilzetzki is Assistant Professor of Economics at LSE. He is an Associate at the Centre for Macroeconomics and the Centre for Economic Performance. HIs research interests are in macroeconomics, international finance and fiscal policy. He holds a PhD in Economics from the University of Maryland.

Ethan Ilzetzki is Assistant Professor of Economics at LSE. He is an Associate at the Centre for Macroeconomics and the Centre for Economic Performance. HIs research interests are in macroeconomics, international finance and fiscal policy. He holds a PhD in Economics from the University of Maryland.

Martin Ellison is Professor of economics at the University of Oxford and a Fellow of Nuffield College. He gained his PhD in economics in 2001 from the European University Institute in Florence. Ellison has worked as a consultant for the Bank of England and as a Professor at the University of Warwick before his current affiliation at the University of Oxford. He is specializing in macroeconomics; his PhD thesis was titled “Money Matters: Four Essays on Monetary Economics”. His main research interest is monetary policy and he is editing several journals in the field of economics.

Martin Ellison is Professor of economics at the University of Oxford and a Fellow of Nuffield College. He gained his PhD in economics in 2001 from the European University Institute in Florence. Ellison has worked as a consultant for the Bank of England and as a Professor at the University of Warwick before his current affiliation at the University of Oxford. He is specializing in macroeconomics; his PhD thesis was titled “Money Matters: Four Essays on Monetary Economics”. His main research interest is monetary policy and he is editing several journals in the field of economics.

Michael McMahon is Associate Professor of Economics at Warwick University. He is also a a Research Associate with the Centre for Macroeconomics (CFM), Research Affiliate with the Centre for Economic Policy Research (CEPR) and the Centre for Applied Macroeconomic Analysis (CAMA, ANU), International Consultant Economist at the IMF’s Singapore Training Institute and a Visiting Scholar at the Bank of England. He holds a PhD in Economics from LSE. Dr. McMahon’s research interests are macroeconomics of business cycles; monetary economics; inventories and applied econometrics.

Michael McMahon is Associate Professor of Economics at Warwick University. He is also a a Research Associate with the Centre for Macroeconomics (CFM), Research Affiliate with the Centre for Economic Policy Research (CEPR) and the Centre for Applied Macroeconomic Analysis (CAMA, ANU), International Consultant Economist at the IMF’s Singapore Training Institute and a Visiting Scholar at the Bank of England. He holds a PhD in Economics from LSE. Dr. McMahon’s research interests are macroeconomics of business cycles; monetary economics; inventories and applied econometrics.

Ricardo Reis is Professor of Economics at LSE, on leave from Columbia University. He received his PhD in Economics from Harvard University in 2004. He has published extensively and has had a number of editorial positions in leading academic journals. He is a Research Associate at CFM and NBER, a Research Fellow at the Centre for Economic Policy Research, and is also a member of NBER’s Macro Annual advisory board. Dr Reis is an academic consultant of the Federal Reserve Board of New York and Richmond.

Ricardo Reis is Professor of Economics at LSE, on leave from Columbia University. He received his PhD in Economics from Harvard University in 2004. He has published extensively and has had a number of editorial positions in leading academic journals. He is a Research Associate at CFM and NBER, a Research Fellow at the Centre for Economic Policy Research, and is also a member of NBER’s Macro Annual advisory board. Dr Reis is an academic consultant of the Federal Reserve Board of New York and Richmond.

Hello all,

Do you think regulation at this moment of development of the blockchain technology would generate perverse incentives for investors to stop doing it or do you think it is neccesary at this stage to create a legal framework that can give certainty to the financial system?