The incidence of corporate taxation is a key issue in tax policy debates. According to surveys, most people think that capital owners bear the burden of corporate taxation. Since capital owners usually have high incomes, this suggests that the corporate tax is highly progressive. Business lobbyists challenge this view and argue that the tax reduces investment so that labour productivity and wages decline, which means that workers bear the tax burden.

Most economists take a middle ground and think that the tax burden is shared between labour and capital. But even among researchers in the field, there is substantial disagreement about how much of the burden is shifted to workers. The main reason is that credible empirical evidence on the causal effect of corporate taxes on wages is scarce. Some studies compare wage growth in countries after corporate tax reforms to wage growth in other countries where no reforms take place.

The trouble is that wage growth differs between countries for many reasons, and isolating the effect of the tax reform is challenging. In addition, countries do not change tax rates very often. Other studies focus on single countries and compare sectors or firms that face different tax burdens. Here the challenge is that the tax burden itself is usually influenced by the behaviour of firms.

In our paper, we avoid these difficulties by exploiting the specific institutional setting of the German local business tax (LBT) to identify the corporate tax incidence on wages. There is substantial tax variation at the local level in Germany. Our analysis combines administrative panel data on the universe of German municipalities with administrative linked employer-employee micro data from social security records. In this data, we observe firms in 3,522 municipalities, leaving us with 6,802 tax changes for identification. About 90 per cent of the tax changes are LBT increases.

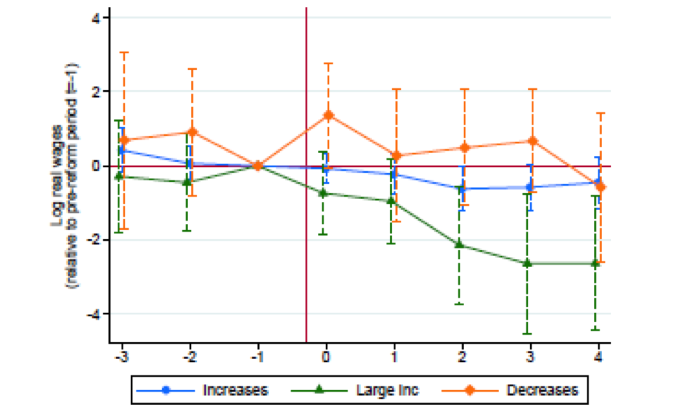

The blue line in Figure 1 shows that wages decrease significantly after tax increases. At the same time, our event study estimates are flat and insignificant in the periods prior to a tax reform, supporting our identifying assumption and the causal interpretation of our estimates. We also show that tax reforms are not driven by local business cycles. Intuitively, we find a larger wage response for large tax increases as indicated by green line, but we do not find significant effects for the few tax decreases.

Figure 1. Event study estimates

Source: Fuest, Peichl and Siegloch (2018) based on LIAB and Statistical Offices of the Laender

Our estimates imply that, on average, 51 per cent of the corporate tax burden is passed onto workers. This average effect is similar to other studies analysing the corporate tax incidence on wages (such as Arulampalam, Devereux and Maffini, 2012; Liu and Altshuler, 2013; Suárez Serrato and Zidar, 2016).

Note that the overall tax burden includes the excess burden of the corporate tax. Empirical estimates suggest that the marginal excess burden of the corporate tax is roughly 30 per cent of the revenue raised (Devereux, Liu and Loretz, 2014). This implies that raising one euro of tax revenue via corporate taxes reduces wages by roughly 65 cents or two-thirds of the revenue raised.

We find that different types of firms and employees are affected differently by tax changes. First, labour market institutions matter. In particular, collective bargaining agreements play a key role (as emphasised by Arulampalam, Devereux and Maffini, 2012 and Felix and Hines 2009): if wages are set via collective bargaining at the firm level, wage responses are larger than in cases where wages are set at the sector level or without collective bargaining. The higher the rents to be shared between firms and workers, the higher the pass-through on wages. For instance, wages are more sensitive to tax changes in more profitable firms. However, we find that wage effects are close to zero for very large firms, foreign-owned firms and for firms that operate in multiple jurisdictions. This can be explained by better profit-shifting capabilities of these firms.

Second, different types of workers are affected differently. We show that higher taxes reduce wages most for the low-skilled, for women, and for young workers. These results qualify the widespread view that the corporate income tax is highly progressive.

We assess the implications of these findings for tax progressivity in a back-of-the-envelope calculation. Our starting point is the study on the progressivity of the US tax system by Piketty and Saez (2007) who assume that corporate taxes fall entirely on capital income. We take their data and estimates as a benchmark for the US and use comparable data for Germany. We then compute two counterfactuals where 50 per cent (or 100 per cent) of corporate taxes fall on wages. Our calculations show that the progressivity of the overall tax system in both countries would decline by between 25 and 40 per cent if we account for our incidence estimates.

To sum up, our results confirm the view that labour bears a substantial share of the corporate tax burden. This reduces the overall progressivity of the tax system. Importantly, our results are obtained by exploiting variation at the local level. Corporate taxes levied at the subnational level exist in many countries, and our results are likely to be relevant in these countries as well. At the same time, it is important to discuss how our findings are related to settings with state-level or national corporate taxes. Two differences are important. On the one hand, labour is likely to be more mobile at the local level, which attenuates the incidence on wages. On the other hand, focusing on tax changes at the municipal level implies that changes of prices other than wages, in particular output prices and prices of intermediate goods, are probably much smaller than in the case of national corporate tax changes. This would imply that wage effects of local tax changes are larger.

♣♣♣

Notes:

- This blog post is based on the author’s paper Do Higher Corporate Taxes Reduce Wages? Micro Evidence from Germany, American Economic Review, February 2018

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Capital and labour, by Henry Stacy Marks, Public domain, via Wikimedia Commons

- When you leave a comment, you’re agreeing to our Comment Policy

Clemens Fuest is President of the ifo Institute, Professor for Economics and Public Finance at the Ludwig Maximilian University of Munich, Director of the Center for Economic Studies (CES) and Executive Director of CESifo GmbH. Since 2003 he is a member of the Academic Advisory Board of the German Federal Ministry of Finance (head of the board from 2007 to 2010). He is a member of the European Academy of Sciences and Arts, the German National Academy of Science and Engineering (Acatech) and the Bavarian Academy of Sciences and Humanities. His research areas are Economic and fiscal policy, international taxation, taxation, and European integration. Before he was appointed ifo President in April 2016, he was President of the Centre for European Economic Research (ZEW) in Mannheim and professor of economics at the University of Mannheim. From 2008 to 2013 he was professor of business taxation and Research Director of the Centre for Business Taxation at the University of Oxford. He taught as a visiting professor at the Bocconi University in Milan in 2004. From 2001 to 2008 he was professor of public economics at the University of Cologne.

Clemens Fuest is President of the ifo Institute, Professor for Economics and Public Finance at the Ludwig Maximilian University of Munich, Director of the Center for Economic Studies (CES) and Executive Director of CESifo GmbH. Since 2003 he is a member of the Academic Advisory Board of the German Federal Ministry of Finance (head of the board from 2007 to 2010). He is a member of the European Academy of Sciences and Arts, the German National Academy of Science and Engineering (Acatech) and the Bavarian Academy of Sciences and Humanities. His research areas are Economic and fiscal policy, international taxation, taxation, and European integration. Before he was appointed ifo President in April 2016, he was President of the Centre for European Economic Research (ZEW) in Mannheim and professor of economics at the University of Mannheim. From 2008 to 2013 he was professor of business taxation and Research Director of the Centre for Business Taxation at the University of Oxford. He taught as a visiting professor at the Bocconi University in Milan in 2004. From 2001 to 2008 he was professor of public economics at the University of Cologne.

Andreas Peichl is Director of the ifo Center for Macroeconomics and Surveys and professor of economics (macroeconomics and public finance) at the University of Munich, and a research fellow at the Institute for the Study of Labor (IZA) in Bonn. He is also research associate/fellow at Center for Economic Studies (CESifo) of the University of Munich, Germany, Centre for European Economic Research (ZEW), Mannheim, Germany, Institute for Employment Research (IAB), Nuremberg, Germany, Institute for Social and Economic Research (ISER), University of Essex, UK, and VATT Institute for Economic Research, Helsinki, Finland. Dr Peichl has been involved in various research projects conducted on behalf of national ministries, the European Commission, the European Parliament, the European Central Bank, and the OECD. His current research interests include (empirical) public economics, labour economics, and welfare economics, with particular reference to optimal taxation, tax reforms and their empirical evaluation, tax benefit microsimulation, and the analysis of income distributions.

Andreas Peichl is Director of the ifo Center for Macroeconomics and Surveys and professor of economics (macroeconomics and public finance) at the University of Munich, and a research fellow at the Institute for the Study of Labor (IZA) in Bonn. He is also research associate/fellow at Center for Economic Studies (CESifo) of the University of Munich, Germany, Centre for European Economic Research (ZEW), Mannheim, Germany, Institute for Employment Research (IAB), Nuremberg, Germany, Institute for Social and Economic Research (ISER), University of Essex, UK, and VATT Institute for Economic Research, Helsinki, Finland. Dr Peichl has been involved in various research projects conducted on behalf of national ministries, the European Commission, the European Parliament, the European Central Bank, and the OECD. His current research interests include (empirical) public economics, labour economics, and welfare economics, with particular reference to optimal taxation, tax reforms and their empirical evaluation, tax benefit microsimulation, and the analysis of income distributions.

Sebastian Siegloch is an assistant professor of economics at the University of Mannheim since August 2014. He is currently on leave, visiting UC Berkeley and SIEPR at Stanford University during the Academic Year 2017-2018. He received his PhD from the University of Cologne in July 2013, and was a research associate at the Institute of Labor Economics (IZA) in Bonn until July 2014. Sebastian‘s research is on the intersection of public, labour and Urban Economics. He is currently studying the effects of local policy variation on local labour markets. His work has been published in the American Economic Review, the Journal of Public Economics and the European Economic Review among others.

Sebastian Siegloch is an assistant professor of economics at the University of Mannheim since August 2014. He is currently on leave, visiting UC Berkeley and SIEPR at Stanford University during the Academic Year 2017-2018. He received his PhD from the University of Cologne in July 2013, and was a research associate at the Institute of Labor Economics (IZA) in Bonn until July 2014. Sebastian‘s research is on the intersection of public, labour and Urban Economics. He is currently studying the effects of local policy variation on local labour markets. His work has been published in the American Economic Review, the Journal of Public Economics and the European Economic Review among others.