In the quest for identifying barriers to firm growth, much attention has been paid to barriers that act at the level of the individual firm. But firms do not operate in a vacuum: business relationships are potentially central. We conducted an intervention in China to measure their importance.

A field experiment with 2,820 firms

In 2013 we invited tens of thousands of young firms in Nanchang, in China’s Jiangxi province, to participate in business meetings. From the pool of applicants, 2,820 were randomly selected as the study sample. These firms were small, but not tiny: on average, they employed 36 workers and had an annual profit of £93,000.

In our main intervention we randomly divided the 2,800 managers into a treatment group and a control group. Within the treatment group, the managers were randomly split into subgroups of ten people. Each subgroup was then tasked with holding monthly business meetings for one year. Managers in the control group were not tasked with holding meetings. All the firms were surveyed before (baseline), immediately after (mid-line) and one year after (end-line) the intervention.

Effects on firm performance

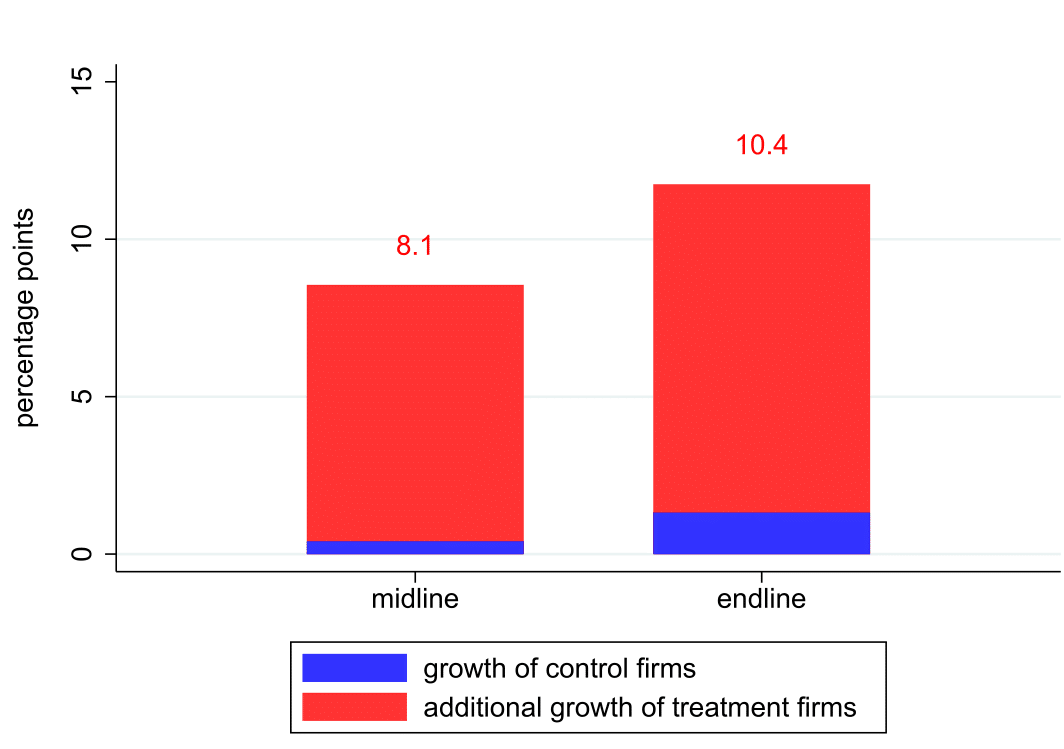

Figure 1 shows the effect of business meetings on firm revenue. The blue bars act as a benchmark by showing revenue growth for control firms which did not participate in the meetings. The red bars measure the additional growth of treatment firms that did participate in the meetings. Growth rates are measured relative to revenue at baseline, that is, the fiscal year before the intervention.

Figure 1. Effect of meetings on firm revenue

The figure shows large, significant, and persistent revenue effects of the treatment. By the midline, revenue increased by only 0.4 percent in the control group, but it increased by an additional 8 percentage points in the treatment group. The bar for the endline shows that this increase persisted in the year after the intervention.

We found similarly large and persistent effects for a wide range of firm performance measures: profit, factors of production (employment and fixed assets), as well as inputs of production (materials and utilities). All these effects are statistically significant.

Intermediate outcomes

We also found significant effects for several intermediate outcomes: a survey-based management score; the number of suppliers and clients; and the probability of borrowing. These outcomes are suggestive of two possible channels by which the meetings may have improved performance:

- Learning from peers leading to improved business management; and

- Better firm-to-firm matching leading to establishing more business partners.

But these results are only suggestive; it is also possible that another channel created firm growth, which then improved these outcomes. Below we discuss more direct evidence on the channels.

Whom you know matters

How did group composition, that is, the type of peers, affect performance? We can answer this question because, by the nature of randomly grouping firms, some firms ended up with better peers than did others. Proxying peer quality with size (employment) before the intervention, we found evidence for significant and persistent peer effects. For example, being randomized into a group in which the average peer firm was 10 per cent larger significantly increased revenue by more than 1 per cent. We found similar effects for a number of outcomes. This result further confirms that the meetings mattered. What’s more, it highlights that the identity of peers mattered.

Channels

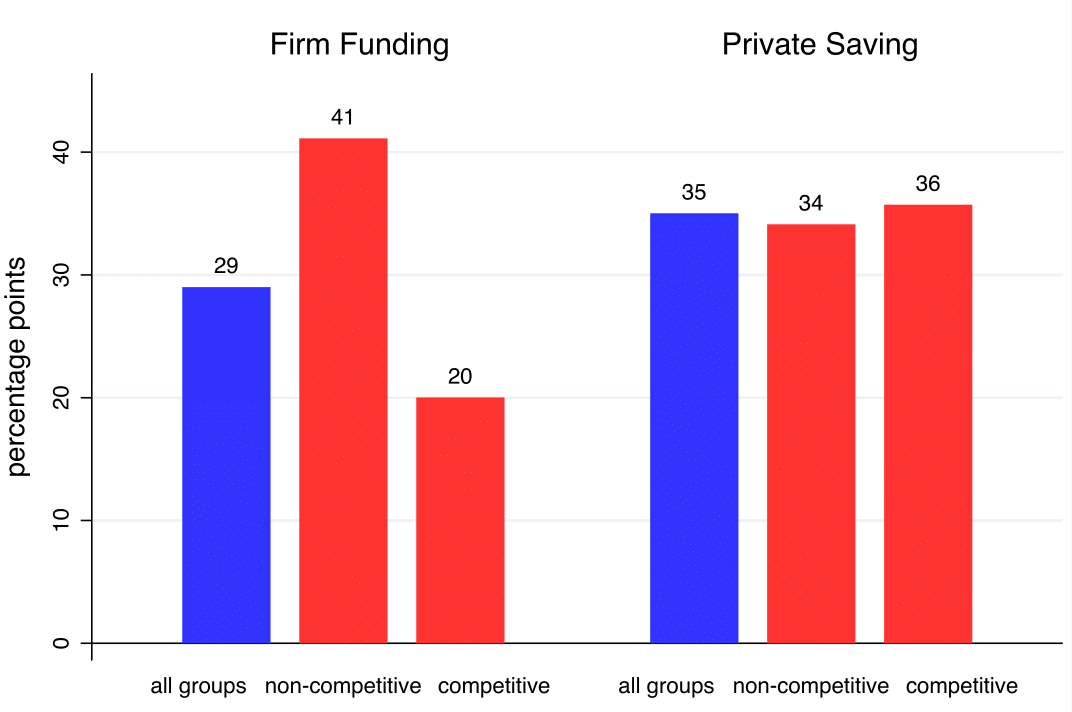

What made the meetings successful? To complement the suggestive evidence on possible channels discussed earlier, we implemented additional interventions that more directly isolate concrete channels. In one such intervention we distributed information about financial opportunities to a subset of managers. We were interested in the extent to which managers shared this information with their peers, that is, the rate of diffusion.

Figure 2. Information diffusion rate

The first set of bars in Figure 2 plots the diffusion rate concerning a firm funding opportunity; a cash-grant from the government. The first bar shows that managers were 29 per cent more likely to apply for this funding if some of their peers were informed, confirming that learning from peers was indeed an active force in the meetings.

The second and third bar separately measure diffusion for “non-competitive” and “competitive” groups, defined by the share of firms in the group that were competitors of each other. Diffusion was lower in competitive groups, suggesting that product market rivalry can hinder learning.

The second set of bars plot the analogous diffusion rates of a second financial opportunity, which was a personal savings account. Because this opportunity did not affect rival firm performance, competition was not expected to affect the rate of information diffusion. The evidence shown in Figure 2 confirms this, with equally strong diffusion effects in competitive and non-competitive groups. These findings not only establish that learning was an active channel, but also uncover a new mechanism: that competition can limit the transmission of rival information.

We used another additional intervention to document the mechanism of improved firm-to-firm matching. In this intervention we organized one-time meetings between managers from different groups. We found that more new partnerships were created in the regular meetings than in these cross-group meetings. This result confirms that regular meetings reduced the cost of firm-to-firm matches, and hence led to improved partnering.

Performance gains and policy impact

We also used our estimates to conduct a cost-benefit calculation, and found that the average profit gains from the meetings exceeded the associated time cost of the managers by a factor of two. While this calculation relies on some assumptions, the extent to which the benefits outweigh the costs strongly suggests that the meetings were overall beneficial. Further research is needed to fully evaluate the contexts to which they generalize, but our results suggest that business associations can be an effective tool for private sector development.

♣♣♣

Notes:

- This blog post is based on the authors’ paper Interfirm Relationships and Business Performance, The Quarterly Journal of Economics, August 2018

- The post gives the views of its author(s), not the position of the institutions they represent, the LSE Business Review or the London School of Economics.

- Featured image credit: Photo by Free-Photos, under a CC0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Jing Cai is an assistant professor in the department of agricultural and resource economics at the University of Maryland. She was an assistant professor of economics at the University of Michigan before joining Maryland. She received her PhD from the University of California at Berkeley in 2012. She is a research fellow at the National Bureau of Economic Research (NBER), an affiliate of the Bureau for Research and Economic Analysis of Development (BREAD), and an affiliated professor of the Abdul Latif Jameel Poverty Action Lab (J-PAL). Her research areas are development economics, Chinese economy, and household finance. Her current research examines growth of micro-enterprises and SMEs, diffusion and impacts of financial innovations in developing countries, and impacts of tax incentives on firm behaviour.

Jing Cai is an assistant professor in the department of agricultural and resource economics at the University of Maryland. She was an assistant professor of economics at the University of Michigan before joining Maryland. She received her PhD from the University of California at Berkeley in 2012. She is a research fellow at the National Bureau of Economic Research (NBER), an affiliate of the Bureau for Research and Economic Analysis of Development (BREAD), and an affiliated professor of the Abdul Latif Jameel Poverty Action Lab (J-PAL). Her research areas are development economics, Chinese economy, and household finance. Her current research examines growth of micro-enterprises and SMEs, diffusion and impacts of financial innovations in developing countries, and impacts of tax incentives on firm behaviour.

Adam Szeidl is a professor of economics at the Central European University (CEU). He is an applied microeconomist who has done research on the economics of networks, international trade, behavioural economics and consumption. He is an editor of the Review of Economic Studies and won several awards, including the Alfred P. Sloan Research Fellowship in 2010. Prior to joining CEU, Adam was assistant and then associate professor at UC-Berkeley.

Adam Szeidl is a professor of economics at the Central European University (CEU). He is an applied microeconomist who has done research on the economics of networks, international trade, behavioural economics and consumption. He is an editor of the Review of Economic Studies and won several awards, including the Alfred P. Sloan Research Fellowship in 2010. Prior to joining CEU, Adam was assistant and then associate professor at UC-Berkeley.