Ever since the financial and sovereign debt crisis, the political and economic implications of Germany’s unbalanced economy have lured the attention of academics, policy institutions, the public and politicians across Europe and beyond. Frequent are the pleas made to the German political establishment to rebalance its export-oriented economic model, increase fiscal expenditures and thus rein in the world’s largest current account surplus.

But what is Germany being criticised for? In essence, the controversy revolves around macroeconomic policy making and what the German growth model implies for the rest of the world. There are four constitutive elements in this debate. Two pertain to the sphere of macroeconomic policy proper, i.e. wage and fiscal policy. One has to do with an empirical manifestation of macroeconomic policy in the German balance of trade, i.e. persistent current account surpluses. The last criticism is centered on the growth model itself and considers the implications of the German export Weltmeister for the European Economic and Monetary Union (EMU) (as well as global imbalances).

Germany’s ‘unbalanced’ economy and the EMU

German policy makers, the argument goes, should rein in the country’s trade surplus and allow for symmetric adjustments in the EMU. Germany is accused of engineering economic growth at home by free-riding on other European countries’ aggregate demand. Some even go as far as to argue that Germany is “artificially” and “purposefully” repressing domestic household consumption, government spending and private investments to sustain a mercantilist model. Germany allegedly refuses to correct trade imbalances and – given fixed exchange rates – grows at the expense of other EMU participants, which have to go through painful internal devaluations and fiscal austerity. What is thus being asked of Germany is to reduce its trade and budget surpluses to provide a more symmetric adjustment mechanism to the single currency via the expansion of its domestic demand for EMU exports.

In the eyes of the critics, Germany’s increased imports are supposed to work as a functional equivalence for the lack of a supranational adjustment mechanism in the monetary union. In other words, Germany should act as a “fixer of last resort” in the Eurozone and, to fulfill this role, domestic macroeconomic policy should follow suit. Since participating in the EMU entails a loss of sovereignty over exchange rate and monetary policies, both criticism and policy advice focus on wage and fiscal policy.

Let’s start with the criticism. People concerned with wage policy argue that Germany has undergone a substantial internal devaluation of its real unit labour costs: real wages have fallen behind productivity rates in both the private and public sector, thus yielding a cost and price competitiveness premium to the German export sector. Those who point at fiscal policy stress the German budget surplus, bemoaning the lack of government spending. Deflationary wage policies are said to deter household consumption at home and imports from abroad. An austere fiscal policy contains the government’s final consumption and contributes to keeping imports artificially low. At any rate, the combination of a restrictive wage and fiscal stance represses total domestic demand (public and private), leads to relatively low inflation, real exchange rates competitiveness and trade surpluses – which prevent the possibility of other EMU participants adjusting via an export-led recovery.

Now the policy advice: what should Germany do? Policy remedies follow consistently from the critiques. Real unit labour costs in Germany should rise faster than its competitors’. Additionally, the German government should spend more money. The effects of this policy mix would set in motion two complementary mechanisms for adjustment. On the one hand, the inflation deriving from higher real unit labour costs and an expansionary fiscal stance will decrease real exchange rate competitiveness and help rebalance the current account – allowing other EMU countries to “breathe”. On the other, increased households and government consumption will increase domestic demand and imports from abroad.

Germany is already rebalancing its economy

In general terms, the criticism on such a high current account surplus is certainly valid. Yet, what the critiques have is common is that they do not ask what Germany has done so far to address these issues. Scapegoating is generally easier than qualified reasoning so let us consider wage and fiscal policy in post-crisis Germany.

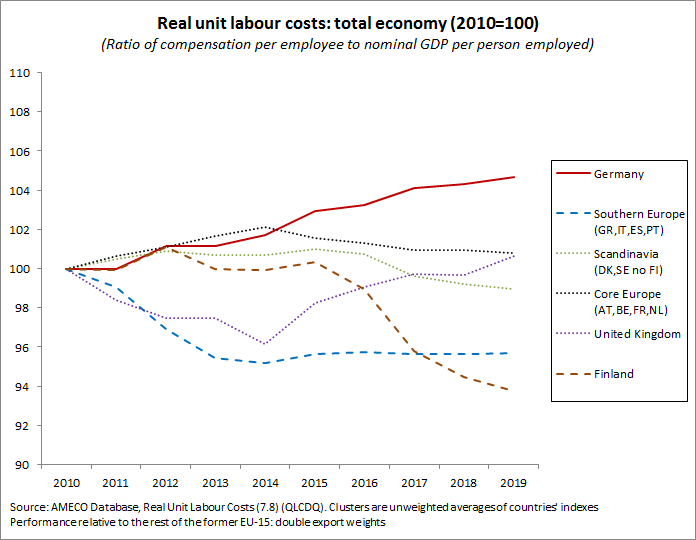

Real unit labour costs have increased, slowly but steadily. In relative terms, Germany has undergone an internal appreciation vis-à-vis its trading partners of approximately 5%, as compared to 2010. Surely, criticising Germany for its own sake may lead to one always asking “how much is enough”. But then one should elaborate on the entity of a higher revaluation and – most importantly – on the feasibility of such an option given the German wage setting systems. Tarifautonomie allows for no government interference in private sector wage negotiations. Regarding public sector wage setting, after the reforms of the mid-2000s it is now the finance ministers of the Länder who are in charge of negotiating wage increases for the public employees they are in charge with, i.e. the majority.

Given that the Länder lack the possibility to manipulate their marginal tax revenues, it would be pointless to expect substantial wage increases in the TV-L contract without a fiscal federalism reform that attributes more money to subnational governments. Even more fundamental is that it is unclear why one should expect the finance minister of a German State to respond to Eurozone imperatives, while being accountable to their local constituency. The only instrument the German government could use to intervene in wage setting is to legislate for an increase of the minimum wage above inflation. This has already been agreedand the government is about to ratify an above-inflation increase of 4%.

Even admitting that it would be structurally possible to raise German price inflation far above the EMU average via wage push inflation, this is likely to create more damage than relief. Given Germany’s size in the EMU, it will rather put enormous political pressures on the soon-to-be new governor of the ECB to tighten monetary policy. The effect for the EMU would be devastating.

Figure 1: Real unit labour costs: total economy (2010=100)

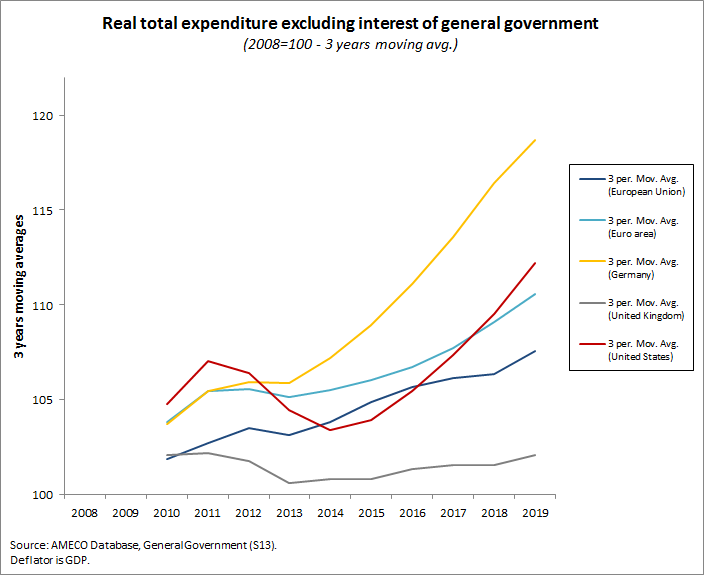

What about the German finance ministers, are they really so stingy? In terms of real government expenditures (net of interest payments), Germany has since the crisis spent considerably more than most other OECD countries, almost twice as much as the increase in spending in the United States – often praised for its post-crisis Keynesian stance.

The truth is that focusing on the budget surplus is misleading since, in a buoyant economy, it is relatively faster growth of revenues that drives the calculation up. Surely enough, again one can ask how much is enough. But, after all, didn’t Keynes say at some point that hoarding money in good times is functional to governments’ countercyclical spending in hard ones?

Figure 2: Real total expenditure excluding interest of general government (2008=100, 3 years moving average)

What about Germany’s current account surplus vis-à-vis its European partners in the single market? Ever since the crisis, German exports of goods to the EU have decreased substantially relative to its imports. The intra-EU export/imports ratio has been going down significantly. In fact, the core countries of the EMU, together with the Visegrád Group, show a higher exports/imports ratio than Germany. Also, countries of Southern Europe have arguably found a market for their export-led adjustment. Their ratio has increased considerably even though they continue to import more than they export.

Figure 3: Intra-EU exports divided by intra-EU imports (2002-16)

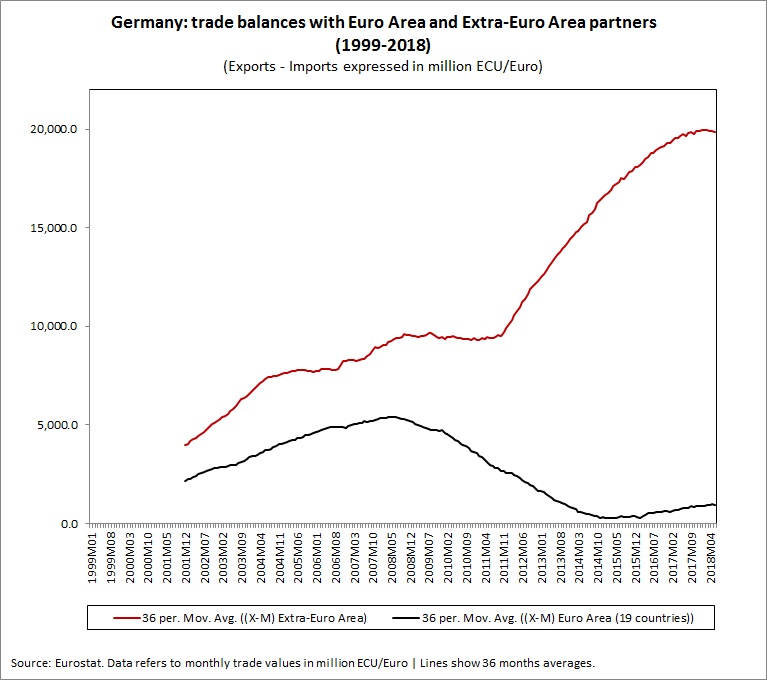

So, where does the German current account surplus come from? Surely neither from the EU single market, nor the Euro Area. Ever since summer 2008, Germany’s trade surplus with EMU partners has disappeared and the current account surplus has been driven solely by extra-EMU trade. In this sense, Germany quietly “exited” the euro in 2008 to then assail international markets in 2011. This makes Donald Trump and his colleagues very angry. Global imbalances are indeed a serious issue in advanced capitalism and others have addressed the topic elsewhere.

Figure 4: German trade balances with the Euro Area and Extra-Euro Area partners (1999-2018)

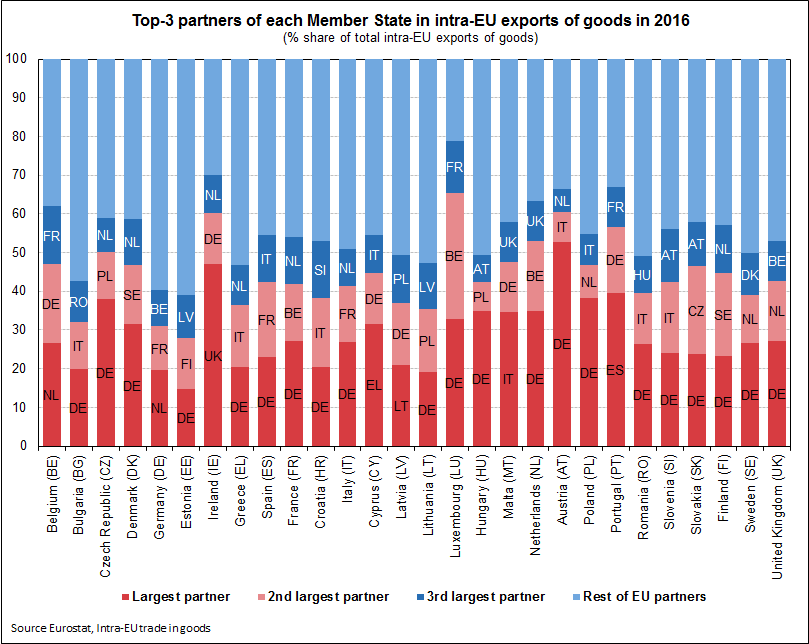

As far as the single market is concerned, Germany is virtually the largest importer for all its members. Germany already provides a very wide market for EMU exports. Will asking Germany to slow down its export engine benefit the EMU? I think it is hard to tell. Possibly, it is instead likely to reduce German imports from its EU trade partners. Overall, it seems that accusing Germany for not providing a sufficiently large import market for European goods is, simply, wrong.

Figure 5: Top-three partners of each member state in intra-EU exports of goods (2016)

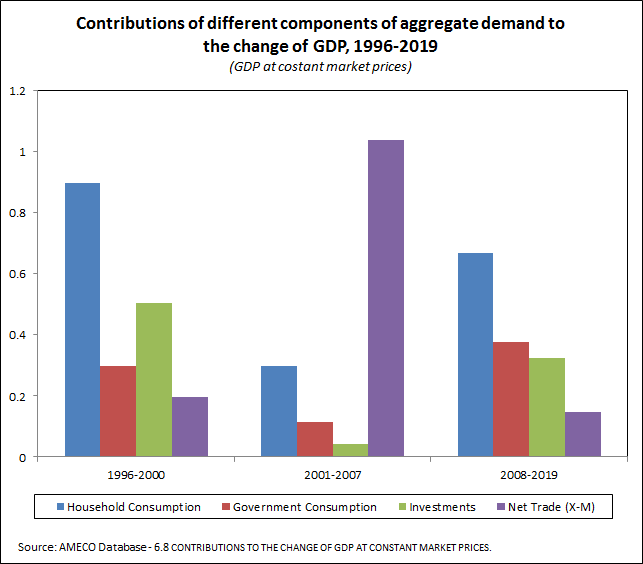

Is economic growth in Germany driven by exports, i.e. net trade (exports minus imports)? Or, in other words, does Germany “steal” growth from abroad? When decomposing GDP growth in the aftermath of the crisis, we ascertain that export-led growth seems to be an historical parenthesis rather than a structural feature of the German economy. GDP growth was strongly driven by exports during 2001-2007. In the aftermath of the crisis, given real wage growth and increased government expenditures, GDP growth has been driven by household consumption, public and private investment. Yes, the export share in total GDP remains high in relative terms, but data shows that exports have not contributed so much to the post-crisis German engine.

Figure 6: Contributions of different components of aggregate demand to change of GDP (1996-2019)

Does this mean that Germany is safe and sound? No. Rather, an incomplete EMU remains fragile and requires upkeep. If German politicians want others to stop blaming Germany for everything that occurs in the EMU, they should venture into a serious EMU reform plan that envisages blühende Landschaften for Europe as a whole and not for Germany alone. Whether they like it or not, they belong to a common project now.

To avoid any misunderstanding: I am not arguing that the German current account and fiscal surpluses are good and desirable. The aim here is to show empirically that, contrary to what is usually claimed, Germany has made important steps towards a “quiet” rebalancing. This is good news and should be kept in mind if we aspire to having constructive politics in the EU.

But it would be a mistake to insist that Keynesianism in Germany will fix the Eurozone’s problems: Germany should not and cannot be the fixer of last resort for the single currency. Supranational adjustment mechanisms are needed for the stabilisation of the Eurozone in hard times. There seems to be one priority around which accusers and defendants can and should come together: to avoid macroeconomic adjustments based solely on the compression of wages and public investment.

Two institutional changes could serve the purpose. Broadly speaking, a pan-European unemployment benefit scheme based on national PPPs would work as an automatic stabiliser to support household consumption when countries most in need are forced to switch them off in their budgets. Secondly, one could imagine an ECB that supports a European Growth Bond by the European Investment Bank in the context of a proper European Investment Plan. Unfortunately, the importance of both these reforms for the stabilisation of the EMU has been eclipsed by the attempts to create a Capital Markets Union to engineer a financial fix to the structural flaws of the EMU.

♣♣♣

Notes:

- This blog post originally appeared on EUROPP – European Policies and Politics

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: OSCE Parliamentary Assembly (CC BY-SA 2.0)

- When you leave a comment, you’re agreeing to our Comment Policy.

Donato Di Carlo is a Doctoral Researcher at the Max Planck Institute for the Study of Societies, Cologne. He works in comparative political economy and European integration with a focus on models of capitalism and wage setting systems.

Donato Di Carlo is a Doctoral Researcher at the Max Planck Institute for the Study of Societies, Cologne. He works in comparative political economy and European integration with a focus on models of capitalism and wage setting systems.