The UK and EU have reached a Brexit deal. But what will the withdrawal agreement mean for the UK economy? To address this question we have analysed how the withdrawal deal and a no-deal scenario would affect income per capita in the UK, relative to the baseline of staying in the EU, through changes in trade costs.

Scenario 1: The current withdrawal agreement

We assume future relations are based on the customs backstop written into the withdrawal agreement. The UK remains in a permanent customs union with the EU, but, with the exception of Northern Ireland, does not remain in the single market for either goods or services. Leaving the single market would give Great Britain (though not Northern Ireland) the opportunity to diverge from EU regulations. However, any divergence would mean that traders have to design their products to satisfy different regulations in different markets. This would create new trade barriers between Great Britain and the EU and between Great Britain and Northern Ireland.

Scenario number 2: The WTO case

In this case, the UK and the EU revert to trading on World Trade Organisation (WTO) terms. The UK would leave both the single market and the customs union, leading to the imposition of far larger trade barriers between the UK and the EU. The EU’s most-favoured nation (MFN) tariffs would apply to UK- EU trade and non-tariff barriers between the UK and the EU would rise due to new trade costs caused by customs checks at the border, rules of origin, and product certification and testing requirements, among others. Regulatory divergence would also be greater than in the ‘deal’ scenario.

What we are looking for

In each case, we analyse the effect of changes in UK-EU trade barriers on aggregate real income per capita ten years after the new trading arrangements are introduced — in practice, given the transition period, this means approximately 2030. A ten-year window allows the economy time to adjust and means our results should be viewed as estimating the long-run impact of the deal and WTO options. We do not attempt to model the short-run effects of either. We note that the short-run costs of a no-deal Brexit are likely to be severe and could exceed the long-run costs.

Our analysis does not attempt to forecast how much the UK economy will grow over the next ten years. The UK’s economic growth depends on many factors other than relations with the EU. Instead, we address a narrower question that can be answered with a greater degree of confidence. Namely, compared to remaining in the EU, what would be the change in the UK’s income per capita, assuming the future relationship were based on either the deal or no deal (WTO) option? This implies our results should be interpreted as estimating how UK levels of income per capita will change relative to a counterfactual world where the UK continues its existing economic arrangements with the EU.

Modelling the deal

To model the economic impact of the ‘deal’ and WTO scenarios, we use the Centre for Economic Performance (CEP) trade model, which is a Computable General Equilibrium (CGE) model. The CEP trade model was used prior to the referendum to study how a ‘Norway-style’ Brexit or a ‘WTO-style’ Brexit would affect the UK. We use the same calibration of the model employed in previous CEP work (see also). The model divides the world into 31 sectors and 35 regions, including the UK and the major EU economies. It features trade in intermediate inputs, as well as final goods, and takes account of how changes in trade barriers affect income levels through their impact on the UK’s trade with both the EU and the rest of the world.

To implement the model, we have made a series of assumptions about how trade costs between the UK and the EU change under the deal and WTO scenarios. We divide changes in trade costs into three parts: (i) tariffs on goods trade; (ii) non-tariff barriers to trade arising from customs checks, product standards and regulations, and other costs of cross-border trade; and (iii) after Brexit the UK may not participate in future steps the EU takes towards reducing non-tariff barriers through deeper integration.

We model the WTO scenario using the same assumptions made in previous CEP work: first, that UK-EU goods trade would be subject to the EU’s MFN tariffs; second, that all UK-EU trade would face an increase in non- tariff barriers three-quarters as large as the estimated reducible non-tariff barriers between the EU and the US, which implies an increase in non-tariff barriers of 8.3 per cent; and third, intra-EU trade costs fall 40 per cent faster than trade costs in the rest of the world over the ten-year forecast horizon, but UK-EU trade costs do not. Assuming the fall in trade costs applies to three-quarters of reducible non-tariff barriers, this implies a 12.7 per cent reduction in intra-EU non-tariff barriers that the UK does not benefit from. (See Dhingra et al. (2017) for details on how these changes in trade costs are calculated.)

In the ‘deal’ scenario, there would be no tariffs on UK-EU trade and no customs-related border procedures. However, goods trade would still be subject to new regulatory requirements and checks due to the UK’s departure from the single market. We assume UK-EU goods trade would be subject to a quarter of the reducible non-tariff barriers between the EU and the US, implying a 2.8% increase in non-tariff barriers. This is the same increase in non-tariff barriers previously used by the CEP to model a so Brexit scenario where the UK stayed in the single market, but not a customs union. Therefore, our assumption is that leaving either the customs union or the single market leads to similar increases in non-tariff barriers. Indirect support for this hypothesis comes from the government’s own Brexit analysis, which (also using a CGE model) found that the impact of non-tariff barriers (excluding regulatory divergence) on UK GDP was similar in size for customs non-tariff barriers and for other non-tariff barriers.

The customs agreement would not apply to services trade, but the level playing field measures in the Withdrawal Agreement suggest non-tariff barriers to services trade would still be somewhat lower than in the WTO scenario. We assume services trade would be subject to two-thirds the estimated reducible non- tariff barriers between the EU and the US, implying a 7.3 per cent increase. Finally, we again assume the UK does not benefit from future falls in intra-EU trade costs. However, we take the view that regulatory divergence is likely to be more limited in the ‘deal’ scenario than the WTO scenario. Consequently, for goods we assume the fall in intra-EU trade costs only applies to a quarter of reducible non-tariff barriers, while for services it applies to two-thirds.

The modelling results show that relative to staying in the EU, UK income per capita declines by 1.7 per cent in the ‘deal’ scenario, but by 3.3 per cent in the WTO case. This leads to the following observations:

-

- both the deal on offer and the WTO scenario would reduce UK living standards compared to staying in the EU;

- the trade-related costs of Brexit are roughly twice as large for the WTO case than if long-term relations were based on the arrangements specified in the Withdrawal Agreement; and

- the estimated costs are comparable to those found in earlier CEP work and in the broader literature on Brexit and trade, although no previous study has analysed the ‘deal’ scenario. The results for the ‘deal’ scenario are close to the CEP estimates for a Norway-style Brexit, where the UK stays in the single market but not the customs union.

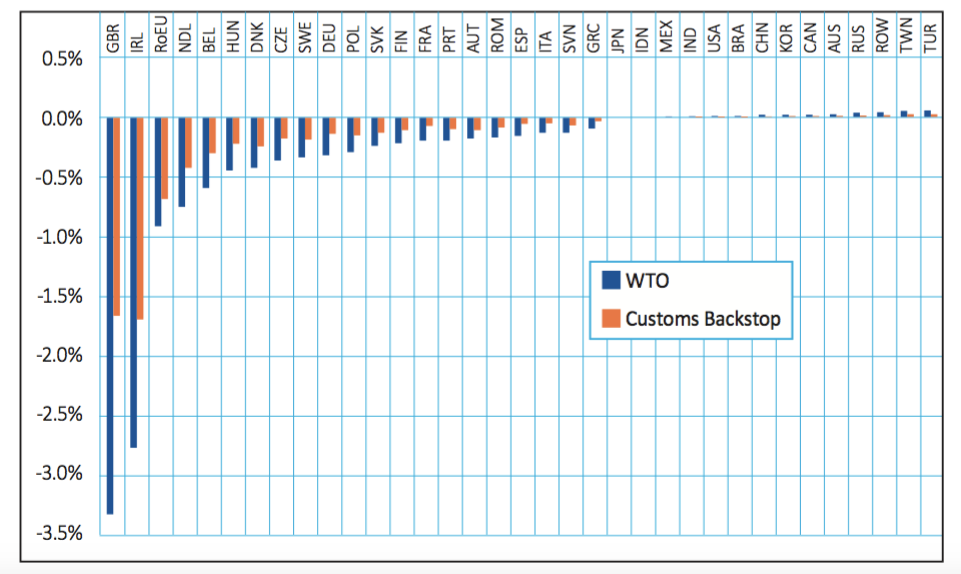

We have also calculated how the two scenarios would affect income per capita in other countries. The results are shown in the figure below. Income per capita falls under both scenarios in all EU countries and the costs are approximately twice as large in the WTO case. The reduction in Ireland’s income per capita is comparable in size to the UK effect, but for most EU countries the losses are around ten times smaller than for the UK, which highlights why Brexit matters more to the UK than the EU. Ireland is the worst-affected EU country because of its high share of trade with the UK. Non-EU countries experience very small income gains due to trade diversion effects.

Figure 1. Income per capita effects by country

Source: CEP calculations

Trade and productivity

The CEP trade model does not allow for any dynamic effects of trade on productivity. Trade integration can raise productivity by promoting efficiency through increased competition, by stimulating innovation or by reducing the cost of intermediate goods. For an alternative way to analyse the two scenarios, we turn to the empirical literature on how trade affects income per capita. A central estimate from this literature is that a 1 per cent decline in trade reduces income per capita by around 0.5 per cent. This estimate is designed to capture all channels through which trade affects income, including productivity changes in addition to the mechanisms embedded in the CEP trade model. It may also partially capture the consequences of changes in foreign investment and immigration that are correlated with changes in trade policy.

Combining this estimate with the changes in UK trade calculated by our model gives, in the ‘deal’ scenario, a fall in income per capita of 4.9 per cent. In the WTO scenario, income per capita falls by 8.1% per cent. These costs are around two and a half times as large as the falls in income per capita obtained directly from the trade model, which is consistent with the idea that the model does not incorporate all the channels through which trade affects output and living standards.

Our results are summarised in the table below. We conclude that, although the exact magnitudes are uncertain, both the “deal” and no deal options are likely to lead to substantial declines in UK living standards.

Table 1. Income per capita effects for the UK

Source: CEP calculations. Assumed elasticity of income per capita to trade equals 0.5.

♣♣♣

Notes:

- This blog post is an edited excerpt from The economic consequences of the Brexit deal, a joint report by LSE’s Centre for Economic Performance (CEP) and The UK in a Changing Europe.

- The post gives the views of its authors, not the position of the institutions they represent, LSE Business Review or the London School of Economics.

- Featured image credit: Photo by David P Howard, under a CC-BY-SA-2.0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Thomas Sampson is an assistant professor in the Department of Economics at LSE. He holds a PhD in Economics from Harvard University and an MSc in Econometrics and Mathematical Economics (with distinction) from LSE. He has worked as a consultant to the World Bank, a fellow of the Bank of Papua New Guinea and other organisations. He has published papers in a number of leading academic journals. His research interests are in international trade, growth and development.

Thomas Sampson is an assistant professor in the Department of Economics at LSE. He holds a PhD in Economics from Harvard University and an MSc in Econometrics and Mathematical Economics (with distinction) from LSE. He has worked as a consultant to the World Bank, a fellow of the Bank of Papua New Guinea and other organisations. He has published papers in a number of leading academic journals. His research interests are in international trade, growth and development.

Swati Dhingra is an assistant professor in the department of economics at LSE. Before joining LSE, Swati completed a PhD at the University of Wisconsin-Madison and was a fellow at Princeton University. Her research interests are international economics, globalisation and industrial policy. Her work has been published in top economic journals. She is associate editor of the Journal of International Economics, and was awarded the FIW Young Economist Award and the Chair Jacquemin Award by the European Trade Study Group for her work on firms and globalisation. Swati is a member of the globalisation group at the LSE’s Centre for Economic Performance, and has made regular contributions to work on economic policy.

Swati Dhingra is an assistant professor in the department of economics at LSE. Before joining LSE, Swati completed a PhD at the University of Wisconsin-Madison and was a fellow at Princeton University. Her research interests are international economics, globalisation and industrial policy. Her work has been published in top economic journals. She is associate editor of the Journal of International Economics, and was awarded the FIW Young Economist Award and the Chair Jacquemin Award by the European Trade Study Group for her work on firms and globalisation. Swati is a member of the globalisation group at the LSE’s Centre for Economic Performance, and has made regular contributions to work on economic policy.