In the initial public offering (IPO) market, sophisticated issuers with considerable sums at stake acquire underwriting services from a large number of capable and highly competitive investment banks. Neoclassical economics implies that such a market will (well, really, must) reach an efficient equilibrium. Yet, in practice, the IPO market has a number of highly unusual features that has led to a consensus in the (extensive) IPO literature that this market simply cannot be efficient. Instead, the IPO literature has generally sought to understand the market by applying insights from behavioural finance. The IPO market therefore provides an excellent case study to probe the meaning of market efficiency and to evaluate the relative merits of the efficient markets and behavioural finance approaches to financial market analysis.

Our research shows that the IPO market is efficient and that the behavioral finance approach has led researchers astray. But, before getting into the efficient markets/behavioral finance debate, let us briefly describe how the IPO process works and why the market is so puzzling.

The IPO market

An issuer making the initial public offering (IPO) of its shares will generally do so by paying an investment bank a fee to manage (or underwrite) the IPO. The bank then: i) chooses the initial investors; ii) sets the initial or offer price of the shares; and iii) places the shares with an underwriting method such that investors do buy the shares at the offer price. The bank’s per-share fee (the gross spread) is set at a percentage of the offer price. Once the initial allocation of shares is complete, trading begins on an exchange and this trading establishes the shares’ market price (by convention, the closing price on the offer date). An IPO’s initial return is then the return from its offer price to its market price.

The average initial return (AvIR) on our 1999/2016 sample of US IPOs is 33 per cent, and AvIRs vary tremendously across both IPO types and time. To illustrate, the AvIR on tech IPOs during the dotcom boom of 1999/2000 is 77 per cent, while the AvIR on non-tech IPOs during the 2001/2016 post-boom period is only 12 per cent. These AvIRs indicate that IPOs are on average underpriced (that is, offer prices are on average less than market prices). Underpricing leaves a great deal of money on the table for investors that — one might think — could more sensibly go to issuers in the form of higher offer prices and to banks in the form of the higher fees on those higher offer prices.

It is the fact that IPO pricing does appear to leave so much money on the table that has led the IPO literature to reject market efficiency and to instead seek to explain underpricing with various behavioural factors. Yet, before one can conclude that IPO pricing is inefficient, one must first figure out how IPO pricing should work in an efficient market.

IPO pricing in an efficient market

In an efficient IPO market, an issuer and its bank both want the issuer’s offer prices to be as high as possible given that the bank can successfully place the shares with investors. So, banks: i) use the optimal underwriting method to ensure that they can successfully place the shares; and ii) set IPO offer prices as high as possible given that underwriting method and issuer fundamentals.

Successfully placing IPO shares with investors is a non-trivial task because IPO shares are of highly uncertain value and investors can at least potentially acquire an informational advantage over the bank. In this case, an investor invited to participate in an IPO can either lemon-dodge — that is, expend resources and figure out if an IPO’s offer price is above its market value and avoid participating if so — or just buy the shares. Since lemon-dodging is always profitable as it enables an investor to avoid an IPO’s downside risk, investors left to their own devices will lemon-dodge. But, if investors lemon-dodge, a bank cannot guarantee that their IPOs will succeed. So, a bank must devise an underwriting method such that investors forego the option to lemon-dodge and instead just purchase the shares.

We think that this underwriting method is block-booking. A block-booking bank enters into a repeat game with a stable coalition of investors in which the bank: i) underprices its IPOs on average (that is, the bank leaves money on the table for investors); ii) preferentially allocates IPO shares to coalition investors; and iii) ejects any investor who does lemon-dodge from the coalition. Block-booking therefore creates a profit-stream that coalition investors enjoy if they refrain from lemon-dodging. So, a bank prevents lemon-dodging by setting offer prices at the maximum level such that an investor finds remaining in the coalition and purchasing on-average underpriced IPO shares in the future more profitable than lemon-dodging once.

To figure out how a block-booking bank sets offer prices, suppose that expected future coalition profits are fixed. As a bank raises an IPO’s offer price from zero, the benefits an investor obtains from remaining in the bank’s coalition remain constant but the benefits of lemon-dodging increase (because an IPO’s downside risk increases as its offer price increases). So, a bank increases an IPO’s offer price to the point where the downside risk on that IPO, given that offer price and its share value distribution, just equals the (fixed) coalition profit. This condition must hold for any IPO the bank underwrites, implying that banks set offer prices to equalise downside risk across their IPOs.

We test our theory by seeing if this downside risk equalization pricing rule correctly predicts the magnitude of the cross-sectional and time-series variation in IPO AvIRs. To do so, we sort our sample into four test portfolios on the basis of a boom/post-boom time-series dimension and a tech/non-tech cross-sectional dimension. If banks block-book, then the downside risk of the return distribution for a given test portfolio equals the equilibrium level of downside risk (which we set equal to the observed downside risk of the initial return distribution for the IPOs in the other time period). So, we proportionally adjust test IPO offer prices until this condition is satisfied. The test IPO AvIR in an efficient market then equals the AvIR calculated with these adjusted offer prices.

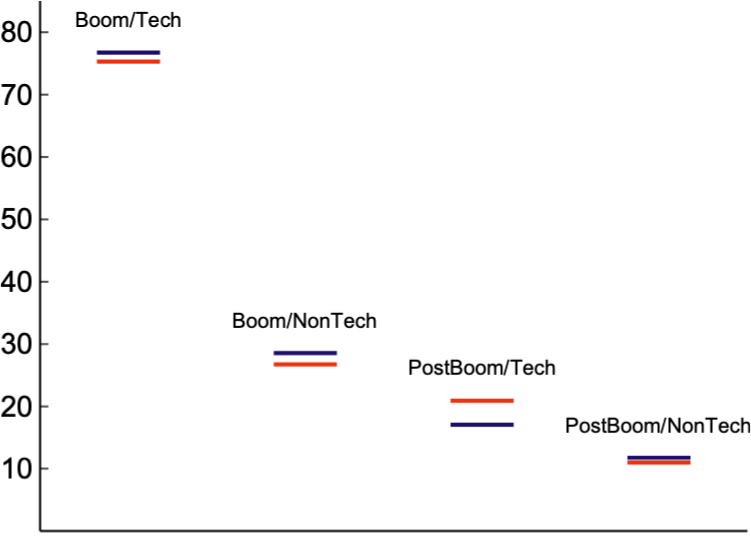

Plotting our results (Figure 1), we find that the magnitude of observed AvIRs closely match the magnitude of AvIRs in an efficient market. To illustrate, the observed AvIR on boom/tech IPOs of 77 per cent is almost exactly equal to their efficient market AvIR of 75 per cent, and the observed AvIR of post-boom/non-tech IPOs of 12 per cent is almost exactly equal their efficient market AvIR of 11 per cent. Intuitively, efficient market AvIRs vary so much because, for a given offer price and expected market value, downside risk on a risky IPO will be much higher than the downside risk on a less risky IPO. Since a bank sets offer prices to equalize downside risk, offer prices on risky IPOs (e.g., tech IPOs during the dotcom boom) will then be much lower relative to expected market value than offer prices on less risky IPOs (e.g., non-tech IPOs in the post-boom period). These much lower offer prices then lead to much higher AvIRs for the risky IPOs.

Figure 1. IPO average initial returns

This figure shows observed AvIRs (Blue) and AvIRs in an efficient market (Orange).

Our theory is the only theory that yields quantitative predictions for AvIRs in an efficient market. Since the magnitude of observed AvIRs closely match these predictions, we conclude that the IPO market is efficient.

Behavioural finance and IPOs

If the IPO market is efficient, just how do behavioral explanations for IPO underpricing have such strong statistical support? We think that two factors combine to bring this situation about.

First, starting with the premise that the market itself cannot possibly be efficient, researchers have tended to use reduced form models to estimate what AvIRs would be in an efficient market. These reduced form models do not capture how AvIRs actually vary in an efficient market and so create large apparent but in fact wholly spurious gaps between observed market outcomes and the “efficient market” null implied by their models. Second, given that there are now hundreds of behavioural factors in the economics literature and little structure on when a given factor applies, it is easy for a behavioural approach to find some factor to “explain” even a wholly spurious gap. These false positives then lead to a misleading picture of how the IPO market functions.

Conclusion

The IPO case illustrates the importance of getting the efficient market null right when analysing how a financial market works. Yet, as Coase argues and as the IPO case illustrates, finding the efficient market equilibrium is not a simple task. It is not an exercise in pure deductive reasoning, and one cannot avoid it by using simple ad hoc nulls instead. Rather, one must look at the market in question (and related markets) for clues about what market participants are trying to accomplish, what frictions/imperfections they face, and what options they have to deal with those frictions. If instead one starts with the premise that market efficiency is “not even a plausible hypothesis”, then one is unlikely to see these clues. And if one does not see the clues, hitting upon something close to the true efficient market null is far more difficult.

It follows that we are much more likely to make progress on understanding both the rational and behavioral aspects of how financial markets actually work if we remain open to the possibility that the market outcomes and process we observe arise from actions taken by rational, optimizing agents in imperfect markets.

♣♣♣

Notes:

- This blog post is based on the authors’ paper The Efficient IPO Market Hypothesis: Theory and Evidence, Journal of Financial and Quantitative Analysis (JFQA), Forthcoming

- The post gives the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by Quinn Dombrowski, under a CC-BY-SA-2.0 licence

- Before commenting, please read our Comment Policy

Kevin R. James is a co-investigator in the LSE’s Systemic Risk Centre. His research focuses upon financial market efficiency and effectiveness, systemic risk, corporate finance, and asset management.

Kevin R. James is a co-investigator in the LSE’s Systemic Risk Centre. His research focuses upon financial market efficiency and effectiveness, systemic risk, corporate finance, and asset management.

Marcela Valenzuela is an assistant professor at the School of Management in Chile’s Pontificia Universidad Católica, a research associate at the Institute for Research in Market Imperfections and Public Policy (MIPP) and a co-investigator at LSE’s Systemic Risk Centre. She received a PhD in finance from LSE, and her research interests lie in the areas of financial crises, financial risk, international finance, and asset pricing.

Marcela Valenzuela is an assistant professor at the School of Management in Chile’s Pontificia Universidad Católica, a research associate at the Institute for Research in Market Imperfections and Public Policy (MIPP) and a co-investigator at LSE’s Systemic Risk Centre. She received a PhD in finance from LSE, and her research interests lie in the areas of financial crises, financial risk, international finance, and asset pricing.

Dear authors,

After reading the article, i’m quite confused how the stated conclusion is the support of an efficient market (in whatever form it may be). Doesn’t the simple observation that such transaction structures must be set up to prevent or solve market failures, directly supports the argument that IPO markets are *not* efficient?

Additionally, i’m still searching for an article that justifies the perspective of IPO’s from an efficient *market* model. As i understand it, there is no market mechanism to set a price before it starts trading, therefore, this seems to be irrelevant for IPOs.

I kindly thank you for any insights on my confusion.

Kind regards,

Victor