How people perceive the quality of the law can affect companies in many ways. Gerhard Schnyder, Anna Grosman, Kun Fu, Mathias Siems, and Ruth V. Aguilera explore the underdeveloped role of legal perceptions in initial public offerings (IPOs), when companies list their shares in a stock exchange. They find that what drives IPO valuation is how shareholder protection laws are perceived, rather than the actual quality of the legal protection.

It is often said that perception matters more than the actual underlying rule. Say you try to discipline a child, and you write a set of rules on the kitchen board, about their screen time, homework, house chores etc, but it stops there – you do not consistently monitor how the child abides by the rules, or discipline the child in case of misbehaviour. Over time, the child’s perception of these rules will be different from what the rules actually are. Thus, what matters in the end, if you want your child to follow the rules, is the perception of these rules. For the parent, the implication is that what matters is the signal that the rules send and how the child perceives that signal.

In an economic context, this analogy from a parent’s everyday life highlights the importance of focusing on the perception of law and how it matters for companies relative to the actual law. In a recent article on legal perception and finance, we argue that the perception of the quality of law should be considered alongside the quality of law and firm-level corporate governance practices. We focus on Initial Public Offerings (IPOs) across a large number of countries, and find strong support for the claim that the perception of the quality of law is more important than its actual quality to explain the post-IPO firm value. This effect remains no matter whether the law’s quality is correctly perceived or misperceived.

One of the novelties of our study is the focus on “legal signalling” which we model theoretically and test empirically. This view focuses on the impact that law has on the legitimacy (as opposed to the efficiency) of economic activities. Laws can have an impact on economic activity through increased efficiency and decreased transaction costs (the standard view). Yet, the law can also have an impact on behaviours by influencing people’s perception of a given legal system or the companies operating in it. We call this aspect “legal perception”. The legal signalling view suggests that laws are not just transaction-cost reducing devices, but also legitimacy-creating devices that signal adherence to certain expected norms and behaviours to market participants.

Based on the actual and perceived quality of minority shareholder perception in various countries, Table 1 shows that adding perception to the actual quality of law is important, because by far not all countries’ legal rules are correctly perceived. Indeed, there is approximately the same number of countries in each category (correctly perceived low-quality law, correctly perceived high-quality law, misperceived low-quality law, and misperceived high-quality law. In the case of Australia, for example, minority shareholders are objectively not particularly well protected according to international standards. Indeed, Australia’s shareholder protection laws score below average in our sample. Yet, the perception of the quality of its shareholder law is above average indicating a mismatch between perception and actual law..

Table 1. Perception of law in 54 home countries

| Correctly perceived low-quality law | Correctly perceived high-quality law | Misperceived low-quality law | Misperceived high-quality law |

| Argentina* | Belgium | Australia | Bulgaria* |

| Bangladesh* | Canada | Finland | Chile* |

| Brazil* | Denmark | France | India* |

| China* | Hong Kong | Germany | Pakistan* |

| Cyprus | Ireland-Rep | Luxembourg | South Korea |

| Egypt* | Israel | Netherlands | Spain |

| Greece | Japan | Oman* | Thailand* |

| Indonesia* | Malaysia* | Saudi Arabia* | Turkey* |

| Italy | Malta | Sri Lanka* | |

| Jordan* | New Zealand | Switzerland | |

| Kenya* | Norway | ||

| Kuwait* | Singapore | ||

| Mexico* | South Africa* | ||

| Nigeria* | Sweden | ||

| Philippines* | Taiwan | ||

| Poland* | United Kingdom | ||

| Russian Fed* | United States | ||

| Tunisia* | |||

| Vietnam* | |||

| 35.2% | 31.5% | 18.5% | 14.8% |

| (19 of the 54 home countries) | (17 of the 54 home countries) | (10 of the 54 home countries) | (8 of the 54 home countries) |

Notes: * denotes emerging economies. Source: Legal Perception and Finance: The Case of IPO Firm Value, British Journal of Management

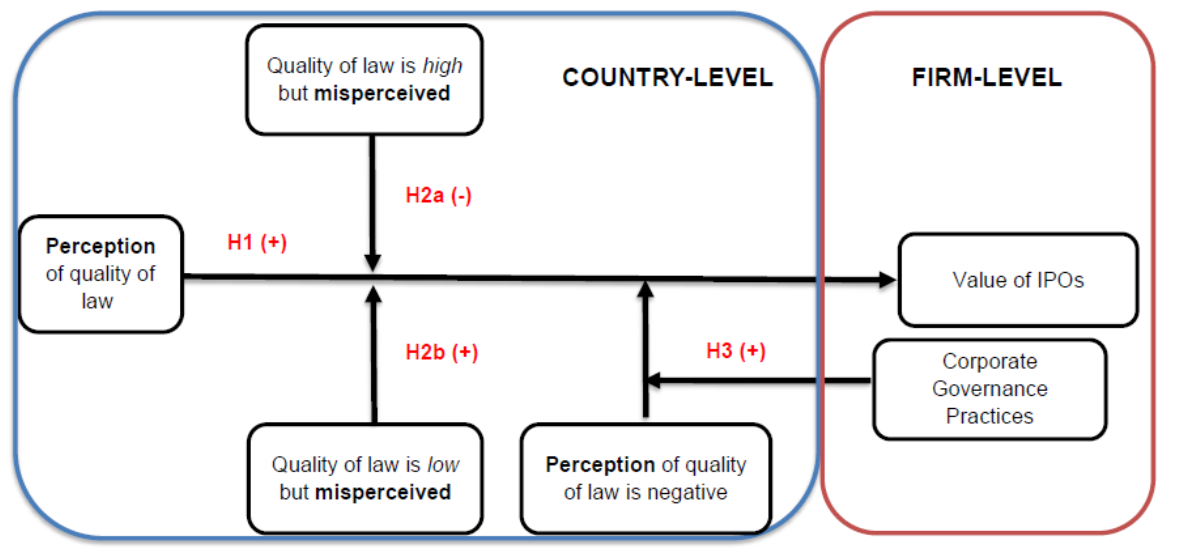

Our research multi-level framework is presented in Figure 1. All of the hypotheses address the underdeveloped role of legal perception in IPOs, be it on its own (H1), or in conjunction with the actual quality of the law (H2a and H2b) and with firm-level corporate governance (H3).

Figure 1. Research model and hypotheses

Source: Legal Perception and Finance: The Case of IPO Firm Value

Our results provide strong support for the basic insight of the legal signalling view that what drives IPO valuation is not so much the actual quality of legal shareholder protection, but rather the perception of its law. In the case of strong actual legal shareholder protection, the effect of legal perception on IPO valuation is stronger if the perception is aligned with positive law than when the quality of law is misperceived.

We also find that in negatively perceived countries (perception below the average), higher levels of firm-level corporate governance affect IPO value. In other words, corporate governance practices can compensate for the negative legal perception. In positively perceived countries, firm-level corporate governance mechanisms do not impact the positive relationship between perception and valuation. One interpretation is that for such countries, the legal framework may be considered sufficient to guarantee a reasonable level of shareholder protection for investors. This hints at the contextual nature of the firm signalling effect, which depends not only on the level of actual legal shareholder protection, but also on its perception. It also supports the idea that firm signalling does not always have an impact on a firm’s reputation. Our study hints at the shortcomings of existing theorisation of the role of law in the economy and suggests that measures of legal quality based on ‘black letter law’ may be insufficient to account for the role the law plays in the economy.

♣♣♣

Notes:

- This blog post is based on Legal Perception and Finance: The Case of IPO Firm Value, British Journal of Management.

- The post expresses the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by Chris Brignola on Unsplash

- When you leave a comment, you’re agreeing to our Comment Policy.

While not having a deep knowledge of the matters this paper paper addresses I as an investor would not only examine the written laws of the countries I am investing in but also their record of applying these laws in the protection of my investments. If the laws are designed to fairly protect the investor and are fairly applied by the courts in the particular country, then my perception will be high. If the laws are poorly written or well written but not applied by the courts then my perception will be low.

Having said this, minority investors may be too preoccupied to study the realities of the written and applied laws in the country they are investing in causing them to rely on their value of perception rather than knowledge. However, I believe majority investors would make it their business to focus on the written laws and the record of these laws being applied by the involved country to protect investors. In this light, uninformed perception is replaced by knowledge or informed perception.

Individual independent perception aside, upon close scrutiny by persons / agencies expert within the realities of written and applied investment law in all countries should be able to clearly sort these complex matters out as a service to potential investors. This would replace weak perception with factual knowledge. Perhaps, all investors should be given a clear unbiased overview of the country they intend to invest in reflecting its record of written and applied law toward the protection of potential investors. After reading and signing off on a short overview document such as this, they can then decide to proceed or not with their investment based on clear knowledge rather than a precarious perception of reality.

I enjoyed reading your paper and my comments spring from my very limited knowledge of the subject matter.

Cheers !

Roy

Dear Roy,

Thanks a lot for engaging with our arguments and for the very thoughtful and interesting comments. Having the practitioner’s view on this is most interesting indeed.

We would agree that the application/enforcement of the law is an important factor here. In our study, we assumed this to be factored into the perception. Indeed, legal perception was taken from a survey that asks business people simply how well a country’s law protects shareholder rights in any given country. Most people certainly will answer this question thinking about the ‘law in action’ i.e. the way it is applied/enforced rather than just what the ‘books’ say. Indeed, that is what your comment suggests: Only when both the content and the enforcement are good, will an investor consider the country’s legal framework to be good.

However, in our study, we find cases where countries whose laws on the book are not good according to international standards of best practice, but the perception is still good. Australia, Finland, France, and Germany for instance fall in this category: perception is better than the content of the laws would warrant (based on international standards of best practice). This may be due to what you suggest: the law may not tick all the boxes, but at least there is certainty about its enforcement. An alternative explanation would be that people overestimate the quality of the law/are not well informed. That could be the case of minority investors, but some studies show a surprising amount of misperception even among experts (some are cited in our study).

Regardless, for our argument the fact that there are countries with weak legal shareholder protection law but still good perception implies that law impacts valuation through perception – and this is what we call the ‘legitimacy effect’.

Thanks again for your thoughtful comments!

Gerhard

Dear Gerhard,

Thank you for your very interesting feedback on my comments.

Cheers !

Roy