The German economy has generally been perceived as the strongest in the Eurozone, particularly since the start of the financial crisis. Terence Tse argues that while the country has impressive headline economic figures, the situation is not quite as healthy as it appears. He notes that levels of internal investment are relatively low in comparison to other European countries, and that demographic trends are likely to impede future development. He concludes that rather than relying on Germany to pull Europe out of its crisis, helping ‘periphery’ countries to stand on their own feet may be a more productive solution.

The German economy has generally been perceived as the strongest in the Eurozone, particularly since the start of the financial crisis. Terence Tse argues that while the country has impressive headline economic figures, the situation is not quite as healthy as it appears. He notes that levels of internal investment are relatively low in comparison to other European countries, and that demographic trends are likely to impede future development. He concludes that rather than relying on Germany to pull Europe out of its crisis, helping ‘periphery’ countries to stand on their own feet may be a more productive solution.

With so-called ‘peripheral’ Eurozone countries – Portugal, Italy, Greece and Spain – currently struggling to pull themselves out of the economic calamities, many people look to the ‘core’ countries, especially Germany, not only as the leader of the EU but also as the saviour of the Eurozone crisis. It’s not hard to see where they are coming from as Germany has the highest GDP in the EU with $3.4 trillion, about half a trillion more than France, the next largest economy. The country also has the best GDP growth among the largest European economies, including France and the UK. It has seen its GDP grow by over 8 per cent since 2009, with 1.2 million new jobs created. Indeed, in 2012, it had a budget surplus of 0.2 per cent of GDP.

Credit: Jack Kennard (CC-BY-SA-3.0)

Germany has also performed well on reducing unemployment. With the second lowest unemployment rate at 5.4 per cent, the country stands out as a notable exception in the EU. By contrast, the rates in France, Italy and Spain, the next 3 largest economies in the Eurozone, are much higher at 11 per cent, 11 per cent and 27 per cent, respectively. But what’s more telling is youth unemployment. The jobless rate for those aged 16 to 24 stands at 8 per cent, compared to 20 per cent in the UK, 22 per cent in France and a whopping 50 per cent in Spain and 60 per cent in Greece.

In addition, Germany has a trade surplus which hit its second highest level in more than 60 years in 2012. In 2013 it ran another surplus: at around 7 per cent of GDP, it is comfortably the largest in the Eurozone. Given that the Deutsche Bundesbank is the biggest among all the national banks to contribute to the ECB, it has the loudest voice in how the bank should run the monetary policy of the Eurozone.

What few of us realise about Germany

All these observations point to the economic – and hence political – strength of Germany. Yet these headline figures may give the wrong perception as they divert our attention away from the weaknesses of the country. Indeed, trouble seems to be bubbling below the surface. In November, the European Commission launched a formal review of Germany’s current account surplus, with the implicit suggestion that Germany’s exports have come at the expense of other Eurozone countries. Many Germans responded to what they saw as an absurd claim by saying that people outside the EU want to buy made-in-Germany products – they can’t help it that their products are of exceptional quality and standard. Yet, it is all too easy to forget that the weakness in the euro – the result of the on-going Eurozone crisis – has made its exports cheap and therefore competitive.

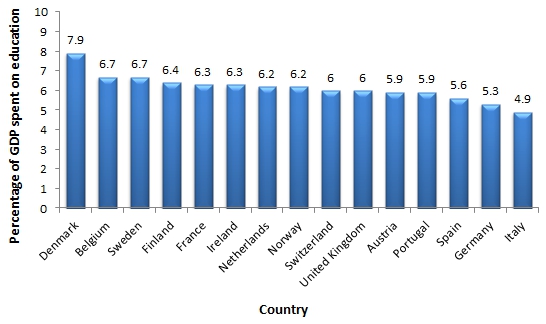

Indeed, Germany’s strong export figures actually highlight its weakness rather than its strength: the country is far from investing enough. The country’s current investment represents only 17 per cent of its GDP; even countries in more difficult economic environments, such as France and Italy, are investing more in their own countries. Public spending is a paltry 1.5 per cent of GDP. The result is chronic under-investment in energy supply, transport infrastructure and education. As shown in Chart 1 below, in the case of education, with spending at about 5.3 per cent of GDP, investment is lower than both the average of 15 European countries and the OECD average of 6.2 per cent. The investment gap is particularly big in early childhood where prospective returns on education are especially high.

Chart 1: Education spending as a percentage of GDP in selected European countries

Note: Chart is based on 2009 figures available here.

The high quality of German products is undoubtedly mostly due to the continuous investments by the private sector. However the current level remains inadequate: growth in productivity has been in decline since 1999. Regulations have discouraged private investment, especially in the services sector. While the Germans save a lot of the money they earn, they are unwilling to invest it in local firms. Instead, they prefer to make overseas investments. Yet, one estimate suggests that between 2006 and 2012, these investors could have lost as much as €600 billion, roughly 22 per cent of GDP. The result is that local firms are shut out of the capital needed for investment;

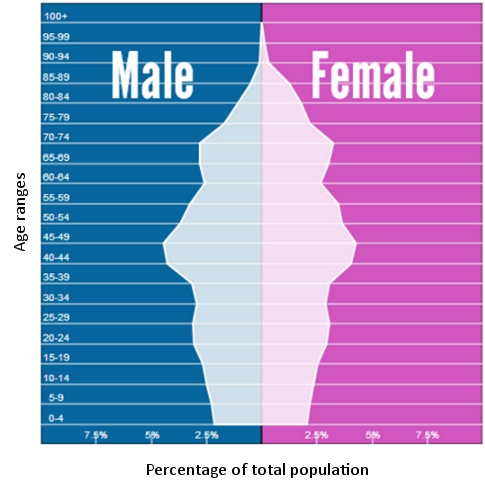

Germany’s current budget surplus is not only the result of low public spending, but also the collection of high levels of taxes. Looking at the demographic pyramid in Chart 2 below, it is possible to see that, compared to other G7 countries, with the exception of Japan, the percentage of the German population in their 40s and 50s is particularly high. The good news here is that there are a lot of people currently paying taxes, contributing to the state coffers; the bad news is that without a massive boost in investment, especially in education, it will be increasingly difficult for the country to support the forthcoming old age government pension burden. Summarising these issues in one sentence, the country is living on the fruits of its past labour; it must do more if it wants to ensure its economic future.

Chart 2: Age distribution of German population (2010)

Source: Population Pyramid

The fact that Germany is not as strong as we believe means that the country may not be able to lift Europe out of its economic woes. If this really is the case, we are pinning our hopes on the wrong leader. It therefore makes a lot more sense for us to come up with new ways to solve the Eurozone crisis: one that does not require Germany to take the lead. Instead, we can perhaps think of directly helping the peripheral countries stand on their own feet. But this shift in our thinking can happen only if we start to realise that, ‘ja’, Germany is doing well for the moment, but, ‘nein’, it will be doing less – perhaps much less – so in the future.

A version of this article originally appeared at the Huffington Post

Please read our comments policy before commenting.

Note: This article gives the views of the author, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/1e1hNtQ

_________________________________

Terence Tse – ESCP Europe Business School and i7 Institute for Innovation and Competitiveness

Terence Tse is Associate Professor in Finance at the London campus of ESCP Europe Business School. He is also the Head of Competitiveness Studies of i7 Institute for Innovation and Competitiveness, an academic think-tank. He can be reached at tt@terencetse.com, and @terencecmtse on twitter.

excellent analysis….

Germany is producing surpluses….which is a disaster for a technology driven economy and a tombstone for the rest of the world. There are a couple of lessons they could be taught from recent Japanese Economic history. And there are a couple of lessons that can be taught from Anglosaxon economics.

The Germans should be worried more than Greeks for the Eurobonds. They should be motivating the rest of the Europe to save Germany in the medium to long term. The renewable energy sector has brought investments and the grid to its knees, the public infrastructure (roads, highways, telecommunications) are -relatively- in their worst ever condition.

In the long term Europe will be saving Germany once again….the 5th of 6th time in less than 100 years…

I am sorry to say but is a poor article. The points have been already mentioned a couple of times before. There is nothing substantially new in this analysis. De facto, it just scratch the surface and the over-aging population is applicable to all Western industrial economies.

If you would look at the UK, for example, you should be able to recognise even more downsides. Moreover, the education nor the British infrastructure can be considered a superior to the German counterparts in general.

What you say about the saving of Germany through Europe is nonsense. Well, I understand it but the continent should consider that is has flushed itself down the drain. Substantially, Europe has not contributed much, concretely said, not anything, to the world’s population, growth…….Just put this Greek-national glasses aside.If you are willing you can see that we all in Europe have been in the SAME boat and this boat is en route into troubled waters.

So if admire the Anglo-Saxon economies as superior, well, OMG.

It is always an illusion that not properly functioning countries/people can be carried forward by the leader. Especially the kind of leader that you refer to basically one that pays the bill even more when there are so many that need that kind of leadership.

Europe has simply too many passengers on one side and it all doesnot create the mindset to get your own house in order on another.

The latter is the main problem imo in the South, they let EMs with a much lower costbase catch up and are in no way fit to compete with them (while even now EMs are moving forward much faster as the ‘Club Med’.

The help you refer to will be mostly financial and all that that seem to do uptil now is deferring the necessary restructuring.

It is mainly a mental thing (as countries their mindset/attitude, necessary for competing in the future, simply sucks). They have to solve that themselves or much more likely will not do it not or too late and fail (if the past say 5 year is any indication) and with as you indicate nobody to pick up the pieces.

Another part I am missing is the fact the merkel is basically reversing the Schroder reforms.

Before these Germany was seen as the ‘sick man’. Reversing these will therefor bring up the hypothesis that it will become ‘sick’ again, unless there is another clear indication.

It is not a 1:1 reversal, but basically it does the same thing increase the welfarestate (and the cost thereof which is real problem).

Effectively the climate in which it is happening look even worse now than it did in Schroder’s time.

-Aging as you indicate is a bigger problem now.

-‘New normal’ growth is lower than structural growth those days anyway.

-Schroder didnot have half Europe to guarantee for.

-The kind of industry (SME, family style stuff) Germany has is now in line for a real outsourcing boom.

With very little pointing in the other direction.

In a nutshell it seems a reversal that Germany even looking only at itself can very likely ill afford. Not even to mention when transferpayments South are would be required.

-The kind of industry (SME, family style stuff) Germany has is now in line for a real outsourcing boom.

Realy? they are already kings of the supply chain. And the EU with the industry robots program for the whole EU is inspired from Germany because there Mid size companies do all this already since a long time. And still not much countries have nearly as much apprenticeship programs as Germany.

Much more important is that Hartz4 reforms were almost useless.

Did just increase the inequality to an pervert Level -> so huge surplusses.

Dreadful domestic market etc.

The real Story is that, Germanys ULC grow significant slower already since 1995 and not since 2004(Hartz reforms) as many people think.

http://www.wirtschaftswurm.net/uploads/2014/02/relative-Lohnstückkosten-1994-2012.png