Portugal held elections on 4 October, with the governing centre-right coalition winning the election, but losing its absolute majority in parliament. Luís Aguiar-Conraria assesses what the result of the election could mean for the country’s economy, which was one of the worst hit during the Eurozone crisis. He argues that while the potential for another election to be held in the short-term could pose a problem, there is nevertheless reason for cautious optimism about Portugal’s economic future in the short to medium term.

Portugal held elections on 4 October, with the governing centre-right coalition winning the election, but losing its absolute majority in parliament. Luís Aguiar-Conraria assesses what the result of the election could mean for the country’s economy, which was one of the worst hit during the Eurozone crisis. He argues that while the potential for another election to be held in the short-term could pose a problem, there is nevertheless reason for cautious optimism about Portugal’s economic future in the short to medium term.

While Portugal’s election on 4 October produced few surprises politically, given the polling proved exceptionally accurate; compared to the previous election, there have been two main changes to the Portuguese electoral map. First, the incumbent centre-right coalition, led by Pedro Passos Coelho, no longer holds a majority in parliament. Second, the support for parties that signed the Memorandum of Understanding with the Troika decreased from around 80 per cent to 70 per cent of the electorate.

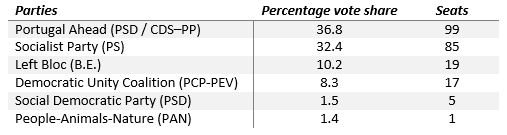

Table: Provisional results of the 2015 Portuguese election

Note: The Parliament has 230 seats, but 4 of these seats will only be assigned after the final results from voters outside Portugal are counted. Only parties that have a seat are shown. Portugal Ahead is a coalition of the Social Democratic Party (PSD) and CDS – People’s Party (CDS-PP). The Social Democratic Party (PSD) shown in the table refers to the electoral list in Madeira and the Azores. The Democratic Unity Coalition is a coalition between the Portuguese Communist Party (PCP) and the Ecologist Party “The Greens” (PEV). For information on the other parties see: Socialist Party (PS); Left Bloc (B.E.); People-Animals-Nature (PAN).

On the one hand, these developments are good news for the Portuguese economy. There is still widespread support for the parties that prefer Portugal stays in the euro and that agreed with the fiscal discipline imposed by the European treaties (according to which the public debt to GDP ratio should decrease from 130 to 60 per cent by 2035).

The defeated centre-left Socialist Party had a government economic programme which could easily be signed by the centre-right governing coalition, as it included some (liberal) reforms in the labour market, some restrictions on social subsidies and some (small) steps moving the social security system towards a fully funded system. It is true that it also included some fiscal stimulus, but these measures were relatively minor.

On the other hand, the fact that the government coalition lost its majority in the parliament suggests a bumpy road ahead. In Portugal, the culture of political compromise is not well developed. Typically, the parties in opposition force new elections after a couple of years. Only once in recent memory did a minority government reach the end of its mandate. Therefore, in Portugal, (almost) everyone is anticipating new elections in either 2016 or 2017.

The possibility of new elections in the short term may refrain the government from taking unpopular measures. This is particularly risky as in the last year, possibly with the objective of winning yesterday’s elections, austerity measures have been relaxed. As a result, the deficit in the first semester of this year is about 4.7 per cent, when it is supposed to be 2.7 per cent at the end of the year. Moreover, the government has already committed to a relevant tax return in 2016. Incredibly, we are still talking about the feasibility of having a deficit below 3 per cent, instead of discussing the final 0 per cent target.

Another problem is social security. Usually, when one discusses social security, the concern is with the long-term picture. In Portugal, this is no longer the case. Because of unemployment and mass emigration, social security contributions are exhausted. During the campaign, all the parties denied the possibility of pension cuts. This is probably the most important challenge ahead. Will the government and the Socialist Party reach a serious commitment to deeply reform the social security system? So far, neither of them have shown in public that they understand how deeply important this issue is.

From a broader economic perspective, in the non-governmental arena, there are mixed signs. On the one hand, saving rates have reached record lows (after a significant rise in the beginning of the crisis). Thanks to that, imports are increasing, endangering Portugal’s external accounts equilibrium. This has so far not been a severe problem because of the low international oil prices (Portugal is a net oil importer).

On the other hand, the exporting sector is alive and well. In just a few years the exports to GDP ratio increased from less than 30 per cent to more than 40 per cent. And it continues to grow. Almost every quarter, there is good news on that regard. Moreover, there is strong evidence that technological exports are increasing, suggesting that the Portuguese economy is finally adjusting to the paradigm a living with a strong currency.

The potential for short and medium term growth is largely thanks to the current high unemployment levels and to high-skilled mass emigration. High levels of unemployment guarantee that it is possible to increase production without inflationary pressures. The fact that there are highly skilled Portuguese living abroad provides the potential for easy international recruitment for firms wishing to invest in Portugal.

All in all, one can be cautiously optimistic about the future of the Portuguese economy. And, although the election results did not help a lot, they did not cause severe damage either.

Please read our comments policy before commenting.

Note: This article gives the views of the author, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/1LiYI7i

_________________________________

Luís Aguiar-Conraria – University of Minho

Luís Aguiar-Conraria is Associate Professor of Economics at the University of Minho in Portugal.