Financial crises play a key role in changing existing policies concerning financial markets and institutions. Orkun Saka, Nauro Campos, Paul De Grauwe, Yuemei Ji and Angelo Martelli provide new evidence for the negative impact of financial crises on the process of financial liberalisation. They also show that such interventions are only temporary and that the liberalisation process restarts quickly after a financial crisis. These results support the view that governments use short-term policy reversals as a tool to ease crisis pressures.

Large economic and political turbulences occur in the aftermath of financial crises. What starts as a panic in a single financial market or institution usually propagates rapidly to other agents of the economy and might necessitate an urgent and decisive reaction from policymakers. However, it is difficult to predict, a priori, whether the reaction of policymakers to the crisis would be in the direction of further liberalisation.

On the one hand, as financial institutions and markets become dysfunctional in the midst of a crisis, governments may feel the urge to intervene, for instance by bailing out the failed banks or increasing the efforts to better regulate the misbehaving institutions. This could be politically unavoidable especially when the cause of the crisis is commonly perceived to be the result of “unregulated capitalism” and public sentiment turns against the financial industry as well as the bankers at its helm.

On the other hand, such periods of instability may act as a catalyst for pushing forward the liberalisation agendas that might have been stuck due to private interests or lack of political enthusiasm. In that case, financial crises could open a window of opportunities to make sharp changes in the policy space. This view is in line with the more general crises-beget-reforms hypothesis.

In a recent paper, we study how financial reforms evolve in the aftermath of financial crises by carefully merging the classic dataset on financial liberalisations by Abiad et al. with the more recent but narrow dataset by Denk and Gomes and the recently updated IMF dataset on financial crises. This provides us with one of the most comprehensive set of observations that has been employed on the crises-reforms nexus covering 94 countries over the period between 1973 and 2015. The dataset includes 7 major areas of financial reform including 5 indices directly related to the domestic banking sector (credit controls, interest rate controls, entry barriers, privatisation, and supervision), one index on restrictions in international capital movements and one on asset markets (security market regulation).

Using a quasi-difference-in-differences approach, we first find that the immediate impact of financial crises is to lead to de-liberalisation. This result generally holds for any individual reform area and crisis type (banking, currency or sovereign debt crises, in order of increasing effect size). It seems that, at least in the specific context of “financial” crises and “financial” reforms, periods of turmoil do not spur liberalisation efforts; on the contrary, they end up reversing some of the previously liberal policies. This contrasts with the predictions of the earlier literature on the political economy of reforms.

Instead, our results align with the view that governments may consider crises as market failures and respond by increasing their interventions in the hope of an urgent correction in the markets. Therefore, it is likely that governments may be using reform reversals as a form of self-help. This could be especially true for bank bailouts (privatisation reversals) as there has been an increasing demand since the 1970s for protection of the middle-class wealth during financial crises. As argued by Chwieroth and Walter, this may even result in the punishment of incumbent politicians if they fail to provide such protection. If this view is true, government interventions should be temporary and hence disappear in the medium-term as the crisis wanes.

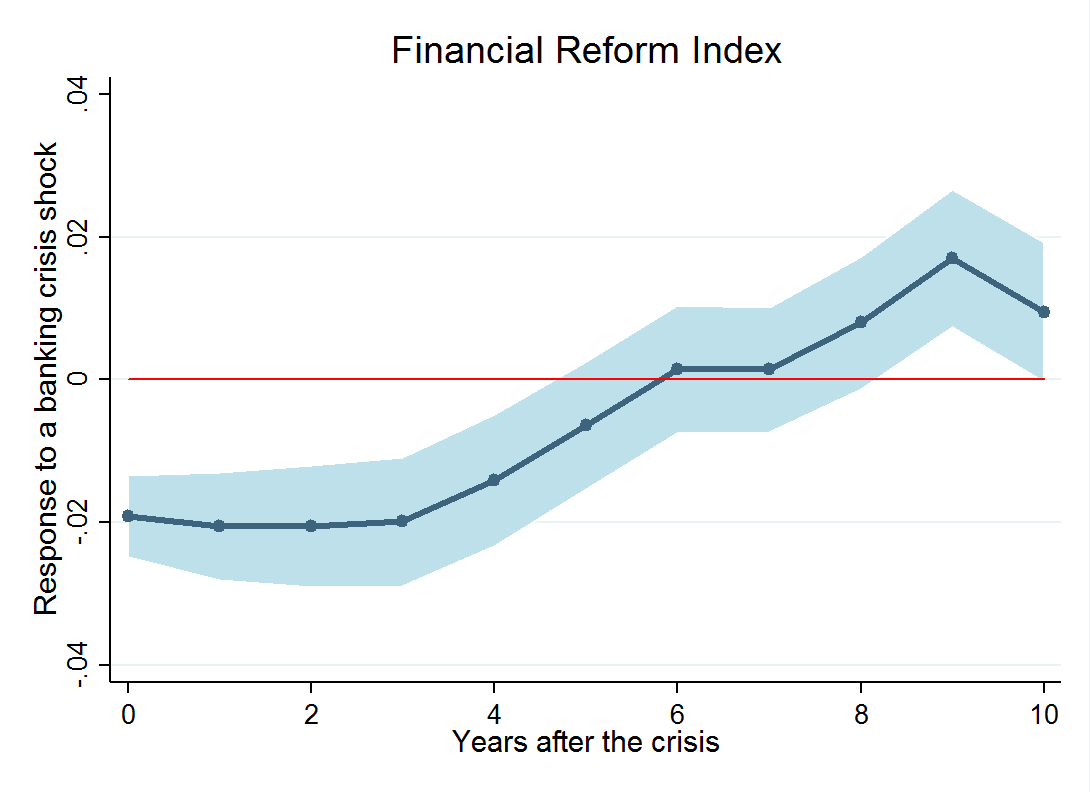

An alternative argument to explain our findings on the reversals of reforms could be that politics breaks down and governments become fractionalised following financial crises with more veto players coming into play and affecting the government’s reform programme. In that case, one would expect reversals to be persistent over time and crises to have a longer-term negative effect on the liberalisation process. In order to investigate this hypothesis, we utilise local projections à la Jordà and plot the impulse-response function of a continuous measure of banking crises on the average level of financial liberalisation.

Figure 1: The effects of a banking crisis on average level of financial liberalisation

Note: The figure shows the estimated impulse-responses via the local projections (LPs) method (see the Equation 2 in our paper) using the average financial reform as the endogenous variable and banking crises as the exogenous shock with four lags included as controls on the right-hand-side for each variable. The shaded area represents the 90% confidence intervals. Source: Saka et al. (2019)

Figure 1 illustrates the time horizon of the relationship between financial crises and reversals showing us clearly that the effects are concentrated on the very short-term. After the contemporaneous decrease in the liberalisation levels, there is no additional divergence between crisis and non-crisis countries in the following years. Indeed after 3 years – which is approximately the average duration of a banking crisis in our sample – countries that had a crisis start catching up with the ones that did not. Overall in a period of 5-6 years there is almost no effect of the banking crisis on average liberalisation levels. Some countries may even end up being more liberalised than their counterparts a decade after experiencing a banking crisis.

These results are more in line with the argument that governments react to crises by using short-term policy reversals in order to intervene and correct market failures. Such urgent policy reactions might be in high demand especially with the middle-class voters and thus explain our finding that the negative effect is almost entirely driven by the contemporaneous relationship in Figure 1. As soon as the crisis pressures ease, countries go back to their liberalisation paths and catch up with others.

These findings also have important implications for the general literature on the crisis-reform nexus. As documented before, many studies on the political economy determinants of reforms produce contradicting and inconsistent results that make it hard to reach a consensus. Our findings imply that, not only the contemporaneous relationship but also the persistence of the effects might matter in this discussion and could reconcile some of the contrasting results in the literature that look at the effects of crises on reforms at varying horizons.

Finally, our results support the case-study evidence reported in Dagher arguing that financial regulation is inherently pro-cyclical – being more lenient during booms and stricter during recessions – and crises may act as turning points. Whether such regulatory cycles occur due to changing sentiments in the public and how they interact with the lobbying power of the financial sector and electoral incentives of the incumbent politicians constitute fruitful avenues for future research.

Please read our comments policy before commenting.

Note: This article gives the views of the authors, not the position of EUROPP – European Politics and Policy or the London School of Economics. Featured image credit: Marco Nürnberger (CC BY 2.0)

_________________________________

Orkun Saka – University of Sussex / LSE

Orkun Saka – University of Sussex / LSE

Orkun Saka is an Assistant Professor of Finance at the University of Sussex and a Research Associate at the Systemic Risk Centre and the European Institute of the London School of Economics and Political Science (LSE). His main research interests are in financial intermediation, international finance and political economy. He tweets @orknsk.

Nauro Campos – Brunel University London

Nauro Campos – Brunel University London

Nauro Campos is Professor of Economics and Finance at Brunel University London, a post he has held since 2005. He is also a Research Fellow at IZA-Bonn and a Research Professor at ETH-Zürich. His main fields of interest are political economy and European integration.

Paul De Grauwe – LSE

Paul De Grauwe – LSE

Paul De Grauwe is a Professor and the John Paulson Chair in European Political Economy at the London School of Economics and Political Science (LSE). His research interests are international monetary relations, monetary integration, theory and empirical analysis of the foreign-exchange markets, and open-economy macroeconomics.

Yuemei Ji – University College London

Yuemei Ji – University College London

Yuemei Ji is a Lecturer in Economics at University College London (UCL). Her interests cover three aspects. 1. International macroeconomics in general and the European monetary union during post-crisis period in particular. 2. Behavioural macroeconomics. 3. The Chinese economy, especial its financial development and the government and private debt problems.

Angelo Martelli – LSE

Angelo Martelli – LSE

Angelo Martelli is soon to be an Assistant Professor in European and International Political Economy at the London School of Economics and Political Science (LSE). His research interests span labour economics and European political economy.

1 Comments