Europe’s political leaders are deeply divided over how to manage the economic consequences of the Covid-19 outbreak. Dimitris Katsikas writes that without a sizeable common funding mechanism, the danger is that European economies will be on very different fiscal and macroeconomic trajectories once the health crisis is over. However, the correction of these imbalances would come at a high economic and political cost, and further divisions between states could ultimately put the future of the Eurozone at risk.

Europe’s political leaders are deeply divided over how to manage the economic consequences of the Covid-19 outbreak. Dimitris Katsikas writes that without a sizeable common funding mechanism, the danger is that European economies will be on very different fiscal and macroeconomic trajectories once the health crisis is over. However, the correction of these imbalances would come at a high economic and political cost, and further divisions between states could ultimately put the future of the Eurozone at risk.

The coronavirus pandemic is an unprecedented health crisis with tragic humanitarian consequences. At the same time, it is a major economic trial, particularly for Europe, which stands at the heart of the global pandemic. The required fiscal intervention constitutes a challenge, whose scale is magnified for the Economic and Monetary Union (EMU), which has experienced a deep economic crisis in recent years. The EMU came out of the crisis burdened with economic problems, political divisions and no common fiscal and/or debt instruments to help her navigate through a future economic shock. Alas, the shock came earlier than anticipated and exceeds by far any adverse scenario previously considered.

Some member states, mostly in the south, are burdened with high levels of public debt, which makes it harder to employ the fiscal resources necessary to combat the pandemic and most worryingly raises the prospect of another debt crisis the day after. To avoid this, the EMU needs common fiscal and debt instruments, which however entail risk mutualisation and a certain degree of fiscal transfers. For Germany and its allies such a prospect is unthinkable, and they resist it fiercely.

As a result, old divisions over the handling of the debt crisis have reappeared; European leaders try to find common ground, but they stand a long away apart. The Eurogroup’s deal on 9 April, provides temporary relief, but does not offer the definitive solution required. The stakes are high; if the Eurozone fails to deal effectively with a major economic crisis for the second time in a decade, the consequences could be dramatic.

Unresolved disputes and incomplete reforms

After the outbreak of the global financial crisis, and in the midst of the debt crisis that followed, the EMU embarked on an ambitious reform effort. Germany and other fiscally like-minded member states were able to dictate terms; their priority was to limit ‘moral hazard’, i.e. the risk that debtor countries could use the loans they received (or the ability to borrow through a common debt instrument – a Eurobond), to avoid implementing politically costly, but economically necessary, reforms. This could potentially result in permanent fiscal transfers to those countries, leading to a ‘transfer union’ at the expense of the creditor member states.

Accordingly, the main fiscal reforms have comprised mechanisms of enhanced national fiscal discipline and surveillance. The coordination of an EMU-wide fiscal stance continues to be an unrealised objective and the stabilisation function has remained at the national level. Moreover, proposals for the creation of a European safe asset did not progress. In other words, the EMU, continues to lack substantial common fiscal and/or debt instruments.

Despite the increasingly shared acknowledgment that the ‘reformed’ fiscal governance remains incomplete and in need of further reform, progress has not been forthcoming. The main obstacle is the political economy struggle that continues to pit fiscal conservatives preaching against the risk of moral hazard against supporters of fiscal solidarity. The economic recovery seen in recent years has not changed the terms of this struggle as the Eurozone crisis casts a dense and long shadow. Its legacy includes non-performing loans, high levels of public debt, and output and investment gaps. Dealing with the adverse legacy of the crisis requires further adjustment, which comes at substantial economic and political cost. The distribution of this cost is a highly political issue and has divided the union between proponents of risk reducing and risk sharing options.

Finding a way to overcome this divide has acquired new urgency in view of the coronavirus pandemic, as countries need to employ fiscal resources at an unprecedented scale. Italy and Spain, the two countries at the heart of the pandemic in the EU, have a public debt of 136 and 97 per cent of GDP respectively. Greece whose public debt stands at 175 per cent of GDP and Portugal with a public debt of 120 per cent of GDP are also vulnerable. The scale of the challenge was quickly perceived by the markets and the yields of these governments’ bonds increased rapidly (Figure 1).

Figure 1: European sovereign bond yields (10-year bonds, selected countries)

Source: Investing.com

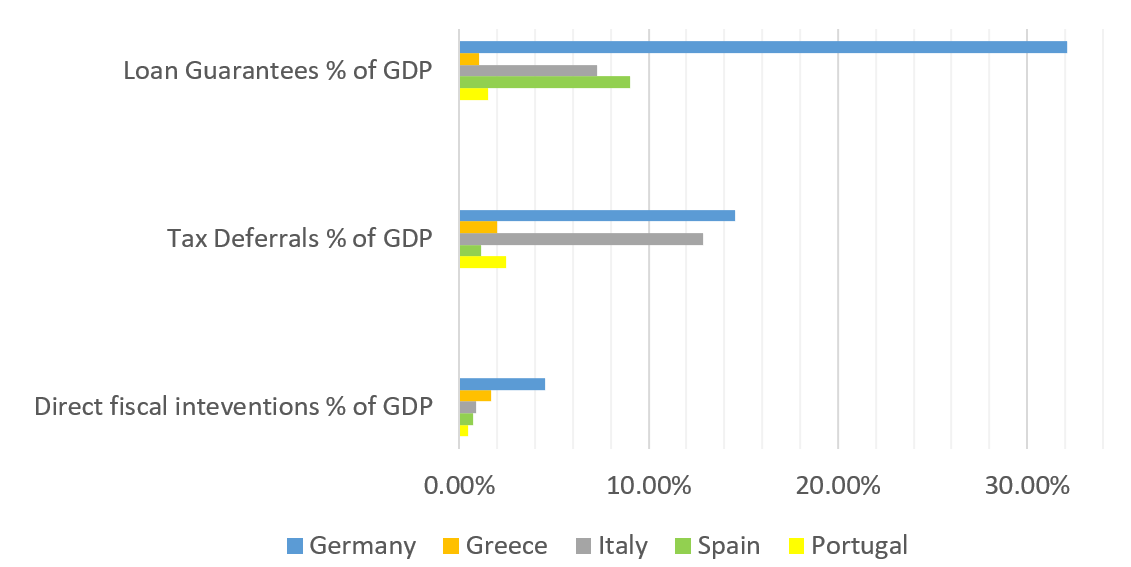

In such circumstances, the fiscal space of these countries is constrained. It is interesting to note that their initial responses to the crisis were very limited in terms of direct fiscal transfers – paying out public funds – and relied more on tax deferrals – delaying tax revenues – and mostly on the provision of guarantees for loans to the private sector, which do not necessitate any immediate pay-outs (Figure 2). Although all countries, including Germany, employ deferrals and guarantees more than direct fiscal transfers, the magnitude of direct fiscal intervention for the countries under stress is particularly small; Italy, Spain and Portugal have committed resources of less than 1% of their GDP. The contrast with Germany’s 4.5% is striking.

Figure 2: Economic responses to the coronavirus crisis (up to 3 April, selected countries)

Source: ELIAMEP compilation based on IMF, OECD and Bruegel data

The EMU’s path dependent initial reaction

What was the EMU’s initial reaction to this unprecedent situation? It followed the same decentralised, ‘individual responsibility’ rationale that dominated both the handling of the debt crisis and the reform effort that followed; the idea is to allow states to deal with the crisis as they see fit, within the limits of their fiscal and macroeconomic circumstances, without committing to substantial common resources or assuming common responsibilities.

The measures announced by the European Commission and the EIB are well below €100 billion, less than 0.5 per cent of the EU’s GDP. This compares poorly to the United States’ $1.2 trillion fiscal intervention, bringing back memories of a delayed response (at that time on the monetary front) to the global financial crisis.

Unavoidably, the response has been bolder when it comes to ensuring national fiscal flexibility; the activation of the general escape clause was an unprecedent but necessary move, as national governments have undertaken major fiscal interventions, which according to Mário Centeno, are on average 3 per cent of GDP, and liquidity supporting measures (e.g. states guarantees for loans to businesses and tax deferrals) that reach 18 per cent of GDP.

The European Central Bank continues its activism, bearing once again the main burden of response. Initially, it added €120 billion to its existing Asset Purchasing Programme (APP) to support the prices of assets (including sovereign bonds). At the same time, it launched a new emergency refinancing operation to provide liquidity to the banking sector and expanded the volume of an already scheduled refinancing operation, adding €1 trillion of available funds at extremely low (negative) rates, up to -0.75 per cent.

The ECB’s major move came on 18 March with the announcement of a €750 billion Pandemic Emergency Purchase Programme (PEPP) with increased flexibility in terms of asset class, maturity and country limits. The PEPP has had a strong positive effect on the yields of southern member states; a further decline was recorded on 25 March, when it became known that for the PEPP, country limits on purchases will be relaxed (Figure 1).

The EMU’s fiscal conundrum

The projections for economic growth are particularly gloomy; according to the OECD, the direct impact of the lockdown measures employed range for most Eurozone member states from 20 to 30 per cent of GDP for the period of implementation. For a lockdown of three months this translates into a 4-6 per cent loss of GDP on an annual basis. Taking into consideration the prospect of a U-shaped recovery, which is increasingly probable, at least for some economies, it becomes clear that the size of funding required is truly unprecedented.

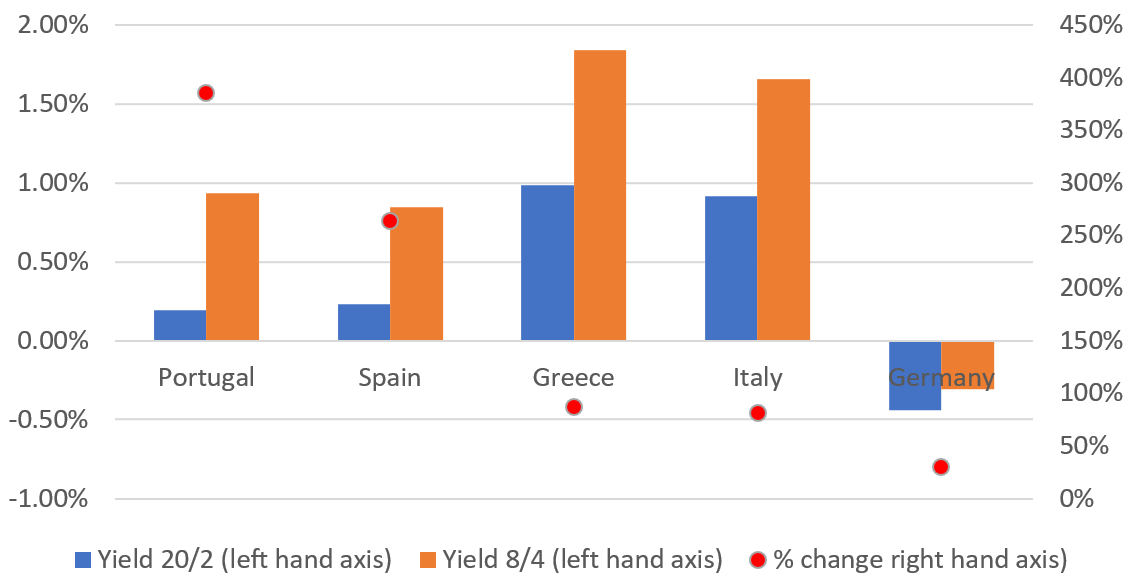

Figure 3: Change in yields of sovereign bonds (10-year bonds, selected countries)

Source: Investing.com

The conundrum is how to access such funds without triggering another debt crisis. Pilling up massive new loads of national debt through a recession is likely to lead to serious sustainability problems in the medium-term for sovereigns that are already heavily indebted, particularly when yields continue to be elevated, despite the ECB’s intervention (Figure 3).

The PEPP does not offer a remedy in this respect; states continue to issue debt on their own terms, which increases debt by one euro for every euro raised. Borrowing from the European Stability Mechanism (ESM) also raises debt, and the same is true for other proposals which operate through loans to member states.

The only way out would be to raise common debt, which is then monetised by the ECB by rolling it over or even cancelling it. Alas, this solution would be against EU law, and a non-starter for supporters of monetary orthodoxy. The alternative would be a no-debt solution, i.e. direct fiscal transfers, e.g. from the EU budget. Fiscal transfers of a big enough size to make a difference, however, is exactly what northern countries are trying to avoid.

A second-best approach would be to raise common debt with a very long maturity; this would reduce servicing costs for indebted countries and transfer repayment far into the future. Proposals along this line suggest either a common fiscal mechanism, or a common debt instrument. Ideally, their set-up would differentiate between the receiving and payment keys; in other words, repayment would be based on a pre-determined criterion like the size of the economy or the ESM’s capital key, but funds would be distributed according to the severity of the health and consequent economic crisis (see here for more details). Such a solution would increase available funding for countries that need it most, without increasing their debt burden at the same rate. This would result in a limited amount of fiscal transfers that would be affordable for the contributors; provided that such a scheme is designed as a one-off emergency solution, fears of a transfer union should not come into play.

Having said that, progress in this direction seems unlikely given the mutualisation of risk such proposals entail. On 26 March, Germany and its allies rejected the request of nine European leaders representing, among others, the vulnerable countries of the south, for a ‘common debt instrument’. The decision was followed by a spat between the Portuguese prime minister and the Dutch finance minister. The divide became more visible than ever before. The drama climaxed as the Eurogroup, assigned by the European Council to come up with new proposals, failed to do so at its meeting on 7 April.

A new deal is on the table, but is it enough?

A compromise was finally reached at the Eurogroup on 9 April. It is based on a multi-pronged response including SURE, the European Commission’s Temporary Support to mitigate Unemployment Risks in an Emergency programme, which will fund labour market measures to the tune of €100 billion through debt issued by the EU based on state guarantees; a European Investment Bank (EIB) scheme for private sector loans, also based on state guarantees; and new credit lines from the ESM.

Agreement has been faster compared to the EMU’s reaction during the debt crisis, and the amounts agreed are substantial. Having said that, it is unlikely that the package will be enough. The ESM funds will be used only for ‘direct and indirect healthcare, cure and prevention related costs due to COVID 19’. However, healthcare is only a small part of the pandemic’s economic cost.

It is uncertain how the much higher cost of supporting the economy during lockdown will be covered; the fuzzy language employed has allowed the Dutch finance minister to state that support for the economy – even for measures directly related to the pandemic – would come under conditionality, at the same time that the Italian finance minister was asserting that ‘conditionality was off the table’.

Moreover, the critical and divisive issue of how to fund European economies’ recovery was left for the future; once again post-meeting statements from the Dutch and Italian ministers show that divisions over mutualisation of debt remain unresolved; a repeat of ‘kicking the can down the road’ seems increasingly likely when it comes to the really important decisions.

In order to heal from the impact of the virus, the Eurozone needs to heal its own divisions. Without a sizeable common funding mechanism, the danger is that once the health crisis is over, European economies will be on very different fiscal and macroeconomic trajectories. The correction of these imbalances would require adjustment policies which however come at high economic and political cost; what is more, given the experience of the debt crisis, they are unlikely to be acceptable to the countries of the south. A new clash over austerity policies would delay the economic recovery, weaken further the EU’s already damaged credibility and ultimately risk the Eurozone’s break-up.

Please read our comments policy before commenting.

Note: This article gives the views of the author, not the position of EUROPP – European Politics and Policy or the London School of Economics. Featured image credit: European Union

_________________________________

Dimitris Katsikas – National and Kapodistrian University of Athens

Dimitris Katsikas is Assistant Professor of International and European Political Economy at the National and Kapodistrian University of Athens. Between 2013-2020 he was Head of the Crisis Observatory at the Hellenic Foundation for European and Foreign Policy (ELIAMEP); he now heads its new Greek and European Economy Observatory. His most recent books include Public Discourses and Attitudes in Greece during the Crisis: Framing the Role of the European Union, Germany and National Governments and Economic Crisis and Structural Reforms in Southern Europe: Policy Lessons, with P. Manasse.