As governments across the world enforce lockdowns to suppress the spread of Covid-19, and with global markets set for their worst quarter since the 2008 financial crisis, what will be the impact on Bangladesh’s economy? Here Sajid Amit (University of Liberal Arts Bangladesh) provides an overview of how small businesses, startups, the financial sectors, consumer demand, remittances and the ready-made garment sector will fare in the coming months.

Globalization has brought great benefits to Bangladesh’s apparel industry as international fashion companies farm out production to cost-effective centres for manufacturing, and by carefully orchestrating a supply chain that spans multiple countries, are still able to deliver products at stores, in time. Covid-19, however, has exposed the vulnerability of these cross-country supply chains, with negative consequences for Bangladesh.

The potential negative impact on Bangladesh’s economy due to Covid-19 however depends on the duration of the crisis. There is a limited possibility, following lockdowns around the world, that infections may return in subsequent wave(s), even if in limited quantities, which may continue to have economic impacts. There are experts however who argue that a potential global recession will fade out by Q4 2020. The International Monetary Fund (IMF) thinks that the recession will be worse, but more short-lived than the global financial crisis of 2008. The duration matters greatly for Bangladesh, because its economic fate is closely tied to the fate of countries that enable the two R’s that drive it: ready-made garments (RMG) and remittance.

The 2 R’s: RMG & Remittances

Ready-made Garments (RMG) companies that buy from Bangladesh are literally closing doors all over European and American cities. Stores have closed for H&M, GAP, Zara, Marks & Spencer, Primark, which are all major buyers. Shopping has come to a standstill as people avoid discretionary spending. There is also a measure of panic regarding raw materials sourced from China. As of 23 March, 264 Bangladeshi garment factories have faced cancellations. H&M, one of the largest buyers of Bangladeshi garments, has had to “temporarily pause new orders as well as evaluate potential changes on recently placed orders.”

At the time of writing, BGMEA President Ms. Rubana Huq suggested the total impact of order postponement/cancellations will amount to US$1.5 billion, which is roughly 50% of our average export income in a month. Insiders interviewed suggest that if the virus continues to impact global supply chains, buyer demand, and of course, health and safety of workers, by Q4 2020, loss in export revenues could reach US$ 4.0 billion.

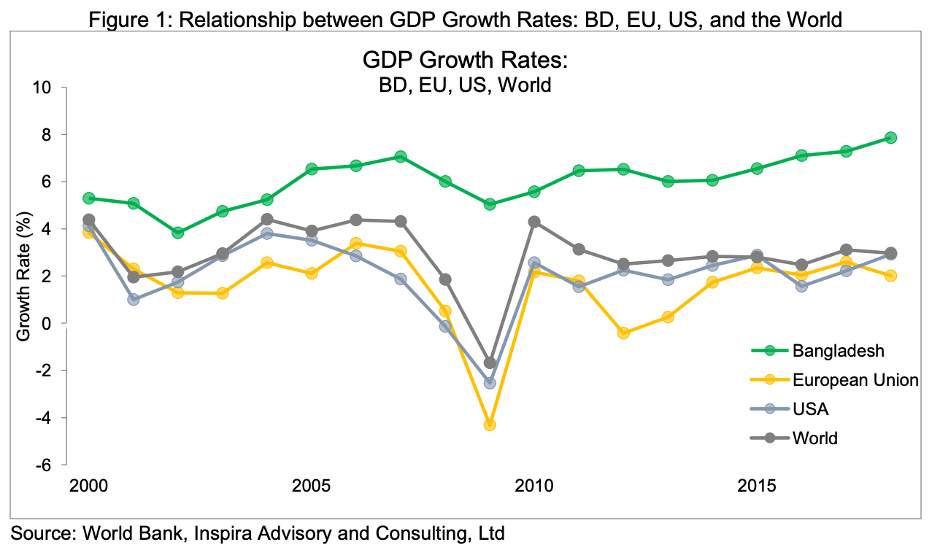

This is not surprising because slowdown in US and EU economies have had ripple effects in the Bangladesh economy (Figure 1). This correlation is most evident for the global financial crisis in 2008, when Bangladeshi GDP growth curve mirrors those of US and EU, albeit the drop off was less severe than for the developed economies.

However, international credit rating agency Moody’s expects that the RMG sector in Bangladesh will recover by the end of the year, as demand recovers and supply chain shocks are overcome.

Meanwhile, the other pillar of the Bangladesh economy – remittances sent by migrant workers – will also take an inevitable hit. Bangladesh has around 10 million workers overseas, with a majority in the Middle East and the US, UK, and Malaysia. Travel restrictions as well as an economic slowdown and curfews in host countries in Saudi Arabia, UAE, Qatar, Kuwait, Malaysia, US and EU countries mean that workers are losing out on wages. The Japan News tells us a story of Jahirul Islam, 30-years-old, who will lose out on 2 months’ pay, after being instructed by his employer, the Abu Dhabi Sports Academy, to go home. While he decided to stay put for fear not being able to re-enter, there are news reports that an untold number of migrant workers have returned. There are also disconcerting stories of migrant workers being shepherded into “labour camps” in Qatar.

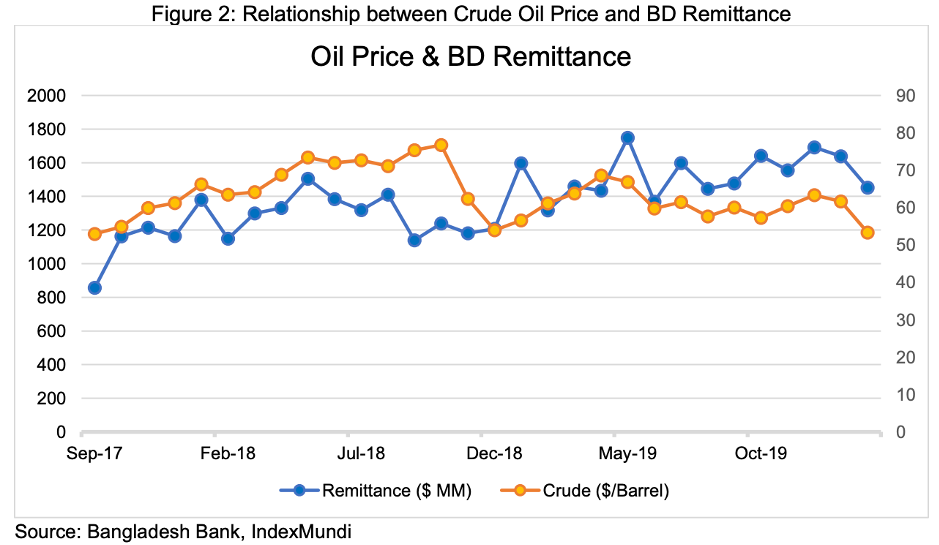

Furthermore, oil prices have fallen precipitously, which is expected to aggravate demand for migrant workers. Oil prices are often an effective leading indicator of inward remittances (Figure 2). History shows that falling oil prices have a lagged effect on remittances into Bangladesh. At present, prices are falling because of reduced demand from sectors such as aviation and transportation sectors, as well as the Russia-Saudi Arabia price war.

Overall, the drop in export revenues, RMG worker layoffs, and reduced flow of remittances will impact demand in the urban and rural consumer economy of Bangladesh.

Impact on Consumer Demand

According to the latest reports, scores of RMG factories are shutting down and workers are going back to the villages. This creates pressure on the rural economy at a time when urban-rural economic linkages have also been severely disrupted. To speak of the urban economy, malls have been closed from 25 March, as per directive of the Bangladesh Shop Owners Association. Only kitchen markets, grocers’ shops, shops selling daily essential commodities and pharmacies have been allowed to stay open. In Bangladesh, footfalls will be minimal in April, which is usually a time stores do brisk business, because of Pohela Boishakh.

In one interview, a retailer with a relatively high capital investment argued she would focus more on her online sales. Our research suggests that several large retailers will look to strengthen their online operations, if effects of Covid-19 last until May, which is the month of Eid, which is when retailers do most of their business. At the time of writing, Bangladesh supermarkets have had more resilient business, albeit for food items and groceries.

Of course, one of the hardest-hit sectors is aviation. In interviews conducted with one of the largest travel agencies in Bangladesh, there was considerable concern about paying staff salaries at a time when customers were seeking cancellations, refunds, and holidays were clearly out of the question. Globally, travel agencies have digitised significant components of their value chain, especially booking and payments. Certain Bangladeshi travel startups have invested in this space, and as a result, may fare better than the competition in the wake of the crisis.

However, travel agencies constitute a fragmented sector in Bangladesh, and owing to Covid-19, many small ones are expected to close shop. Airlines and hotels have also been badly hit. As of 1 March, Mr. Abdus Salam Aref, former Secretary-General of the Association of Travel Agents of Bangladesh, reported that outbound passengers had fallen by 70-80% and inbound, 35-40%. By the end of March, inbound passengers are expected to fall by 70-80%.

Overall, the current economic situation may seriously undermine the livelihood of the underprivileged cohort of the population. The Center for Policy Dialogue (CPD) has predicted that the effect of Covid-19 will be worst for people who are dependent on daily wages and low-income groups. Lack of access to basic healthcare, knowledge of hygiene and a social safety net have always been a challenge for this cohort and the pandemic is likely to increase these challenges, exponentially.

Challenges for the Financial Sector

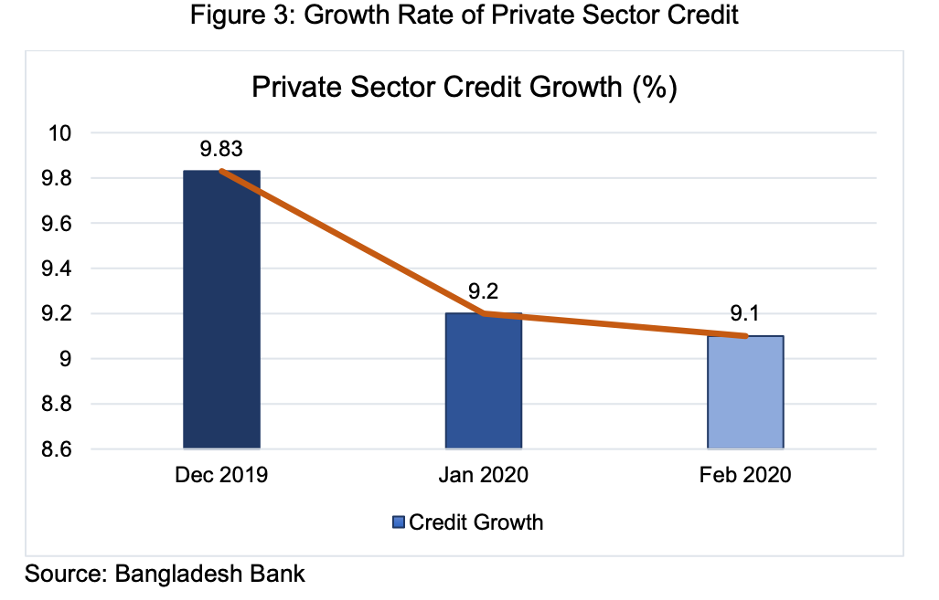

Covid-19 catches the Bangladesh financial sector at an inopportune time. Banks were trying to come to terms with the Ministry of Finance directive of 6% and 9% caps to interest rates on deposits and loans; vulnerable asset quality; moribund capital markets; and a struggling microfinance sector as access to donor funds and bank financing become more competitive. It is worth noting that in the last three months, private sector credit growth was already declining (Figure 3).

A CEO of a leading private commercial bank suggests that banks were taking time to adjust to the 9% directive, as many were reluctant to lend at this rate. As effects of Covid-19 intensify, given that there have been several large-scale order cancellations for RMG clients, many loans may go into default, which is worrisome for the sector.

In the coming months, government sector bank borrowing may decline. This is because large projects such as the Padma Bridge, Padma Rail Link, Karnaphuli Road Tunnel and the Greater Dhaka Sustainable Urban Transport Project involve financial and technical input from China, both of which are expected to be adversely affected. However, a temporary slowdown in government borrowing may assist private sector lending, through a “crowding in” effect. The significance of this remains to be seen. The Bangladesh Bank has also attempted to pump cash into the economy. It has cut both repo rate and cash reserve ratio by 25 and 50 basis points, respectively.

Moreover, the central bank is buying dollars from commercial banks, with the intention of curbing taka’s appreciation against the dollar, has provided guidance on provisions for rescheduled loans, and instructed banks to extend tenure to realise export proceeds, while allowing importers time to make import payments. Once the current risks of infection subside, quantitative easing is expected to encourage banks to seek out investment opportunities. Whenever this happens, some of this liquidity may also find its way into the stock market.

Therefore, while markets are falling, and it is of course, never possible to time a market bottom, there are fundamentally strong equities trading at historically low prices at present.

Impact on Small Businesses and Startups

At times of economic turmoil, small businesses and startups are usually the worst hit. Raising funds is difficult as it is, for small businesses and startups. When it comes to SME’s, in an environment of 6% and 9%, access to finance will become more difficult as banks will be reluctant to make SME loans at 9%, since SME operations are more expensive for banks. It is hoped that the Government will offer SMEs some form of reprieve in the stimulus package that is being designed. For Bangladeshi startups, although the ecosystem is at an early stage, with a handful of startups responsible for a lion share of funds raised, Covid-19 has had adverse consequences.

Fundraising for startups is difficult even in a healthy economy. At the time of the coronavirus, when public equities are being deemed risky and even gold prices have been shaky, startup investing will likely take a considerable hit in the coming months.

The silver lining to this economic scenario is that the Bangladesh government has come out strongly and in a timely manner announcing a multisectoral stimulus package that will shore up RMG businesses, provide direct incentives to workers, buttress the banking system, ensure liquidity in the economy, enable reprieve to exporters and importers, and provide support to other impacted sectors such as tourism, aviation, and hospitality.

In the long run, Covid-19 will have exposed areas for improvement in our health care system, IT infrastructure, workplace cultures, and adaptability of our public and private sector leadership. The virus may also have the unintended consequence of enhancing our social protection and emergency response capacity. It may also push us further along the digital transformation curve. This is a curve we do not wish to flatten, but only steepen.

Given the Bangladesh government’s commitment to ensuring quarantine at a time when official figures of Covid-19 affected persons are low compared to other countries; the potential of a well-considered stimulus package; speedy monetary and fiscal interventions; and not to mention, a large informal economy; there is a possibility that the economy may show signs of reversal by Q4 2020. Of course, much depends on the capacity of RMG and manpower importing countries to recover from economic shocks.

Meanwhile, the resilience and resourcefulness of Bangladeshi people will surely be tested.

An amended version of this article first appeared on University of Liberal Arts Bangladesh.

This article gives the views of the author, and not the position of the South Asia @ LSE blog, nor of the London School of Economics. Photo credit: Graph; Credit: Mediamodifier, Pixabay.

Bro I need the analysis graph which you use in report .

Thank you .

Very informative & precise.