India is one of the biggest consumers of gold on the planet. Nufazil Altaf Ahangar shows that gold has been a better safe-haven asset for investors in the country in times of crisis than stocks and shares. He argues, therefore, that policy-makers should take steps to create a more efficient gold market in India.

Unlike other commodities, gold has the unique advantage of being employed as a store of wealth. Because of its versatility, gold has also been used as jewellery since its discovery. Gold has renounced its position as a currency since the collapse of Bretton Woods system, but it remains a significant commodity for investment. Additionally, it is utilised as a reserve asset and has many industrial uses. Because gold production is limited in comparison to demand, prices have more than doubled over the last 50 years. In fact, gold prices have been rising since the recession of 2009, reaching lifetime highs.

Many economists suggest that gold does well in times of crisis when compared to other asset classes like stocks.

They suggest that gold is considered as an investment asset and an essential part of financial portfolios during times of financial crises or financial shocks. When the world economy was struck by the Dotcom Bubble in 2000 and the financial crisis in 2008, gold investments fared exceptionally well. In the current situation of COVID-19 gold became a safe haven or a hedge for heightened market volatility.

Comparing gold and stocks as safe-haven assets in the Indian context

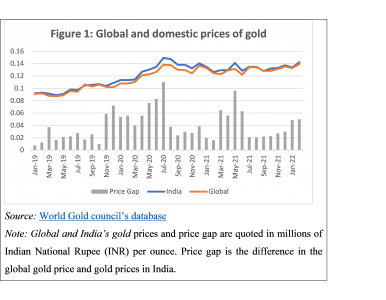

The price and demand of gold is perhaps most apparent in the instance of India among the other emerging markets in Asia. In India, Gold has been a traditional form of savings and an alternative investment in times of crisis. Further, it has limited industrial uses, mostly restricted to medical treatment but is widely used in jewellery production. Since the outbreak of COVID-19 crisis in India during the month of February 2020, the demand for gold appeared to increase. The rising demand of gold in the country in times of crisis continually raised gold price, which were consistently higher than the worldwide market price of gold. From figure 1, one can see that the price gap of gold prices continued to rise from November 2019 to July 2020 (the period of outbreak of wave 1 of COVID-19 in India) and also during March 2021 to June 2021 (the period of outbreak of wave 2 of COVID-19 in India) and a slight increase in price gap during December 2021 to January 2022 (the period of wave 3 in India). The data presented in figure 1 highlights the importance of gold as a safe haven investment in India and by these means Indian gold market is unique in terms of its nature and durable demand for gold.

As the impact of COVID-19 pandemic hit the Indian stock market, a severe fall ensued that resulted in the loss of 5.3 lakh crore INR (approx. GBP 600 billion) worth https://doi.org/10.17015/ejbe.2021.027.02 of investment value and the second largest fall in the history of Indian stock market. Although a slight recovery took place on March 2, 2021 but still markets ended up in the red. Further, March 9, 2021 witnessed a major fall of 500 points in NIFTY in a single intraday session.

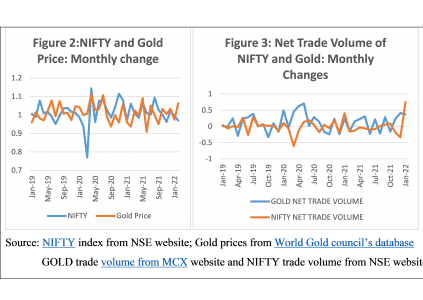

In figure 2, we present the monthly percentage change in NIFTY and gold prices. Perusing figure 2, we can see a sharp fall in NIFTY during the period November 2019 to March 2020 (Period of COVID-19, wave 1 in India) and also considerable fall in the other two waves of COVID-19 (wave 2 during March 2021 to June 2021 and wave 3 during December 2021 to January 2022). However, gold prices have increased significantly during these periods.

The figures of prices do not indicate anything if not supported by net trading volumes (Figure 3). From the data presented in figure 3, we could see the net trading volume of NIFTY index towards the negative side during the period of wave 1 of COVID-19 in India. This indicates heavy selling volumes as opposed to buying volumes. However, for gold buying volumes surpassed selling volumes during these times. A similar case is presented for wave 2 and 3 periods of COVID-19. These figures imply that

in times of stock market crashes due to crisis, gold turns out to be a saving grace for most investors. Like other financial markets, gold has acted as insurance against the damage of crisis in Indian markets when the traditional assets like stocks become unstable.

This means that, in a relative sense, gold can be a stronger safe haven for stocks during temporary market downturns.

Way forward

For an asset to be qualified as a safe-haven asset, its returns should have negative or zero beta when compared to stock market returns during the times of volatility. From the figures presented above we saw that gold has a tendency to produce favourable returns during crisis as it did during Coronavirus pandemic’s lockdown period, indicating that it can be classified as a safe-haven investment. Further, in India, gold is held in large physical quantities, in fact, World Gold Council reports assert that India is world’s single largest market for gold consumption. In India, gold is a more appealing investment than bonds and shares. Gold is also used in the country for many social and religious practices.

Keeping in view such a durable demand for gold in the Indian market,

policy makers need to innovate into gold market by bringing more innovative products like Gold Bullion Securities, and Gold Exchange traded funds.

Although gold ETFs were launched in India in March 2007, they are still in an infancy stage. We need to drive investors to hold gold in ETF form rather than physical forms, in order to create a more efficient gold market in India. Further, the recently introduced derivative market for gold by National Commodity and Derivatives Exchange of India needs to further increase future and option contracts for gold in order to make gold an efficient hedge against risk. For online gold trading, a number of institutions and gold trading enterprises need to be setup that would connect the domestic gold market with global markets. In this vein, a number of local gold trading floors need to be formed with legal frameworks in place to regulate their activities.

The views expressed here are those of the author and not of the ‘South Asia @ LSE’ blog, the LSE South Asia Centre, or the London School of Economics and Political Science.

Banner Image: Photo by Christiann Koepke on Unsplash.