A review of recent research on the antecedents of CEO wrongdoing and suggested actions for organisations – by Karen Schnatterly and Ashley Gangloff.

A review of recent research on the antecedents of CEO wrongdoing and suggested actions for organisations – by Karen Schnatterly and Ashley Gangloff.

Sometimes CEOs misbehave. This misbehaviour has terrible consequences for the CEO, the organisation and society, yet still – they do it. Recent estimates suggest that fraud, a specific type of wrongdoing, results in a loss of 5 per cent of sales for a typical company every year and a global loss of about $3.7 trillion. With such clear consequences, why do CEOs misbehave?

Wrongdoing is defined as a behaviour judged as going from right to wrong; a fine line separates the two. Wrongdoing includes misappropriation (e.g., theft, embezzlement, inappropriate use of company resources), market manipulation, fraud, and other illegal activities as well as earnings management and lying.

Management scholars have been interested in understanding why CEOs misbehave for decades and have worked hard to dissect the antecedents of such behaviours in ways that could help us predict its occurrence. With so much evidence of significant predictors of CEO wrongdoing, there have been few attempts to synthesise it in its entirety. So, we decided to catalogue and draw conclusions from this body of literature to have a better view of what we know about why CEOs engage in wrongdoing and why it’s so persistent.

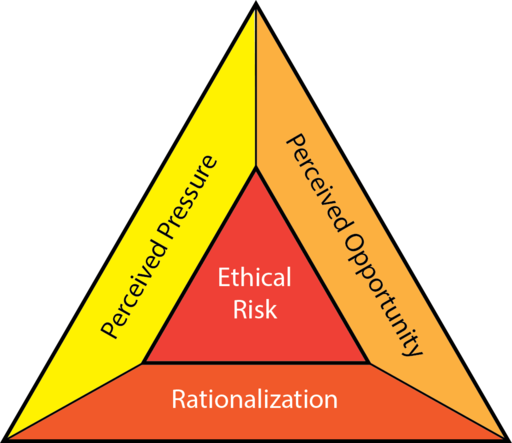

We used the Fraud Triangle, a model often used by auditors to assess the likelihood of misconduct, to structure our review of the literature. The Fraud Triangle explains that three key characteristics are influential in facilitating misconduct: pressure, opportunity, and rationalisation.

Fraud Triangle illustration by David Bailey, under a CC BY-SA 4.0 licence

Fraud Triangle illustration by David Bailey, under a CC BY-SA 4.0 licence

Pressure is the necessity to commit wrongdoing (‘have to’). Opportunity is the ability to commit wrongdoing with the expectation that it will not be detected or punished (‘can’). Finally, rationalisation is the ability to explain an act of wrongdoing as morally justifiable (‘it’s okay’). Pressure and opportunity are different than rationalisations, which are “mental strategies” that individuals use to justify their wrongdoing. In organising all recent management literature about wrongdoing within the Fraud Triangle, we highlight what we know about what precedes CEO wrongdoing and where our understanding falls short.

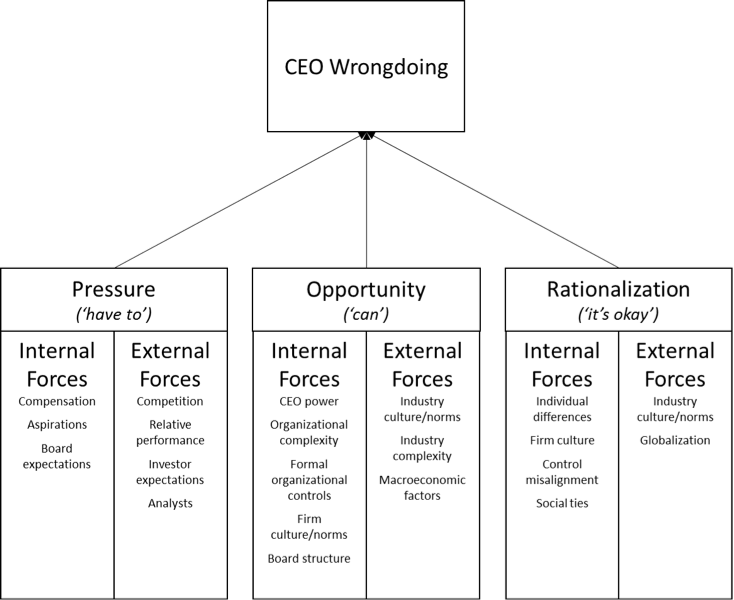

In figure 1, we summarise the common antecedents of CEO wrongdoing from the Fraud Triangle using management publications since 2005. Both internal (e.g., organisational culture or compensation structure) and external factors (e.g., industry rivalry and macroeconomic factors) contribute to the pressure the CEO faces, the opportunity he or she is afforded, and his or her ability to rationalise away misconduct. For instance, scholars have found that male CEOs are more likely to engage in wrongdoing than female CEOs and that firms that are more diversified provide CEOs with greater opportunity to engage in wrongdoing. These are separate findings, but when considering all empirical results across the last thirteen years, we can begin to paint a big picture of CEO wrongdoing and why it occurs so that we can create or refine organisational processes such as recruitment and selection, compensation, decision-making policies and organisational structures to mitigate it.

Figure 1 – Antecedents of CEO wrongdoing

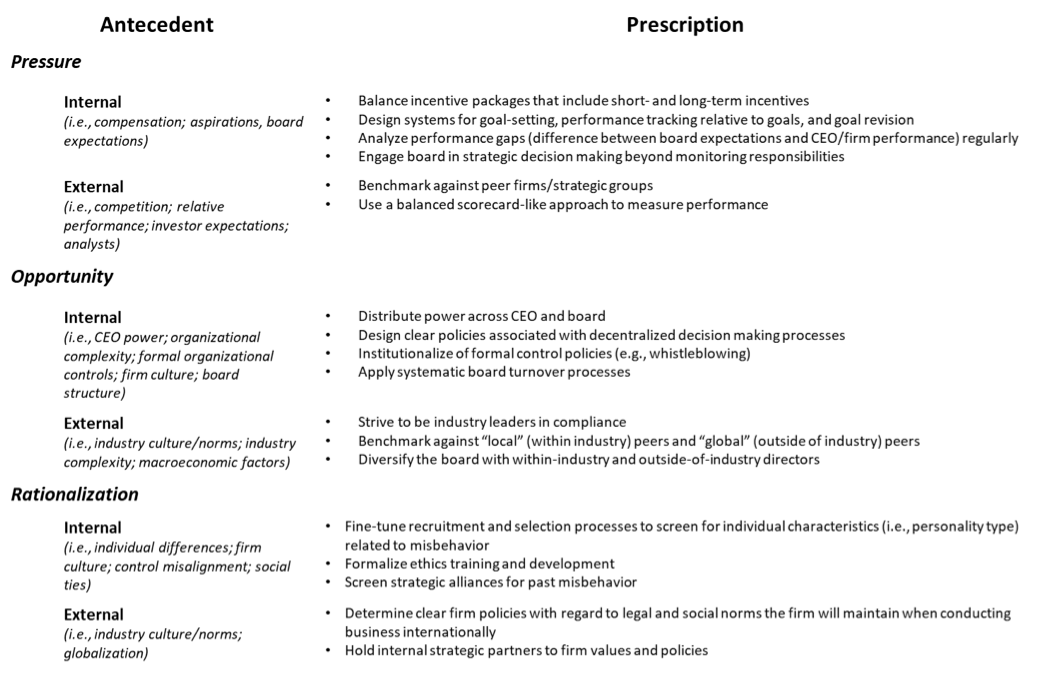

As they say, knowledge is power. So, based on what we know about the antecedents of CEO wrongdoing, we encourage organisations to create or refine practices, policies, and structures. Here we provide examples of organisational prescriptions based on our understanding of CEO wrongdoing. In this table, each antecedent category (e.g., internal pressure; external pressure; internal opportunity, etc.) is listed in the left column and recommendations for addressing each antecedent is provided in the right column.

In our review, we also uncovered gaps in our understanding of CEO wrongdoing. For instance, we know very little about cross-level interactions. Identifying cross-level interactions allows us to understand how variables at different levels (individual, such as the CEO; firm, such as firm performance; and industry, such as industry dynamism) might work in combination to predict CEO wrongdoing.

A second significant gap in our understanding is related to opportunity and, specifically, with regard to external factors that provide an opportunity for misbehaviour. We also have a lot to learn about how external forces might encourage or foster CEO rationalisation. As scholars continue to dig deep into their research, answers to these questions will become clearer and provide practitioners with sound conclusions for building or refining organisational policies, practices, and structures.

Several questions reflect the agenda we recommend for future research — a subset of these questions is listed below. Scholars have yet to address these questions, but we think, if answered, will ultimately help to decrease the frequency of CEO wrongdoing by informing organisational practices.

- What is the effect of CEO status on wrongdoing?

- Does product-market competition create pressure for wrongdoing?

- What kinds of “distractions” can a CEO create that allow the opportunity to misbehave without detection?

- Do external stakeholders’ idealized portrayal of firms/CEOs provide opportunity for CEO wrongdoing?

- What is the relationship between uncertainty associated with organisational events such as an M&A and CEO wrongdoing?

- How do changes in rules or regulations effect CEO wrongdoing?

- How does the political environment influence CEO wrongdoing?

Our assessment of recent management scholarship about the antecedents of CEO wrongdoing provides a springboard for practitioners. Through this work, we aim to inform organisations and their leaders as they create and refine policies, practices, and structures.

- This blog post first appeared at LSE Business Review, and is is based on the authors’ paper CEO Wrongdoing: A Review of Pressure, Opportunity, and Rationalization, Journal of Management, Vol 44, Issue 6, 2018.

- Featured image credit: Photo by Rene Böhmer on Unsplash

Please read our comments policy before commenting

Note: This article gives the views of the author, and not the position of USAPP– American Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/2LsB2ZZ

About the authors

Karen Schnatterly – University of Missouri

Karen Schnatterly is the Emma S. Hibbs Distinguished Professor of Management at the University of Missouri. She was previously on faculty at the University of Minnesota. She is a member of the Academy of Management and the Strategic Management Society. Her teaching and research interests include white-collar crime, boards of directors and institutional owners (corporate governance generally). As a result of her research in white-collar crime, she has been quoted frequently by various news organisations. She has published in top journals has authored several book chapters. She is also an associate editor of the Journal of Management.

Ashley Gangloff – University of Missouri

Ashley Gangloff is an assistant professor at the University of Missouri. She is a member of the Academy of Management. Her teaching and research interest include strategic leadership, ethics, and corporate governance. She has published articles in several peer-reviewed journals.