Taxes also affect the location decisions of people and firms, regardless of other benefits locations may offer, write Ufuk Akcigit, John Grigsby, Tom Nicholas and Stefanie Stantcheva.

Taxes also affect the location decisions of people and firms, regardless of other benefits locations may offer, write Ufuk Akcigit, John Grigsby, Tom Nicholas and Stefanie Stantcheva.

Whether taxes affect innovation, and if so how, is a question of central importance to policy makers across the globe. Recent research has shown that tax policy can have a strong impact on the behaviour of corporations, where superstar inventors decide to locate, and economic activity more generally. While higher taxes can help to redistribute income and lower inequality, they may also reduce incentives for inventors to develop innovations that will ultimately benefit society.

Although the study of the relationship between taxation and innovation is critical to inform policy decisions, lack of data has been a principal obstacle to the analysis of these important effects. In our paper, we conduct a major data collection effort, compiling new data on individual and corporate tax rates in the United States across the twentieth century. We link our rich tax data to comprehensive data on millions of patents by inventors and the R&D activities of corporations. Although our focus is on America, the questions we ask are general, being applicable to other countries and tax jurisdictions as well.

New data on taxes and innovation

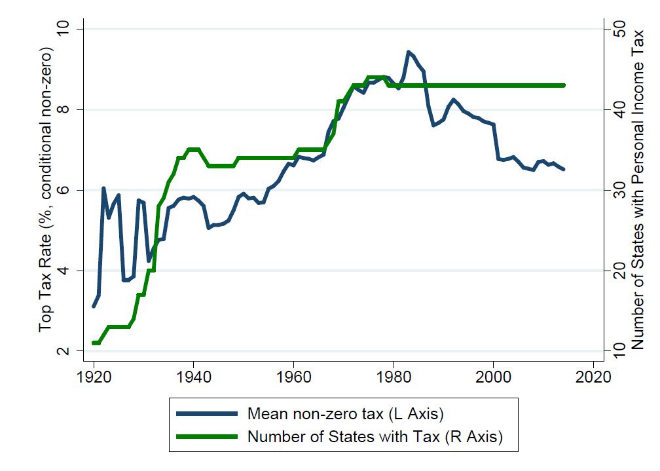

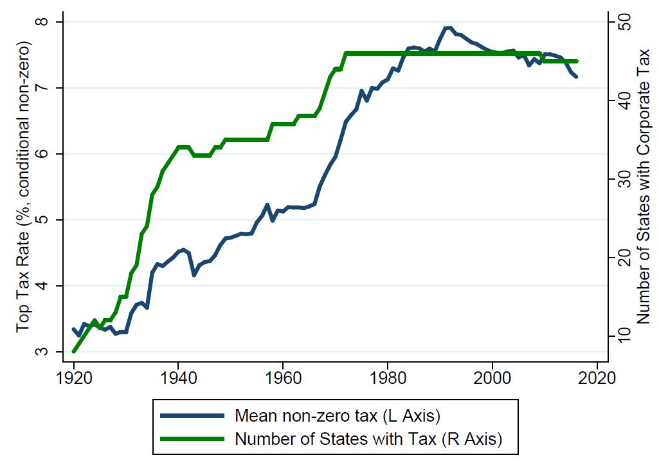

Figure 1 shows the evolution of personal and corporate taxation over time from our newly collected data. We observe major periods of change such as the “Soak the Rich” tax era of the 1930s and the push towards lower taxes during the Reagan administration in the 1980s. The number of states with taxes increased over the twentieth century. Our analysis exploits variation over time, across states and exposures faced by individuals and corporations to examine the impact of taxes on the quantity, quality, and location of inventive activity.

Figure 1 – The evolution of personal and corporate taxes

a. Personal taxes

b. Corporate taxes

Taxes can potentially influence innovation through a variety of mechanisms. Principally inventors invest in costly research and development activities, and they receive payoffs in the event of a successful invention. Taxes, as a levy on net profits, will therefore influence returns and potentially the supply of inventors. Within corporations, invention may depend on how much of the reward is shared with the inventor versus being captured by the firm. Consequently, both personal and corporate taxes could influence the rate of innovation.

Taxes negatively affect innovation

The main finding from our empirical analysis is that higher taxes tend to suppress innovation, and the magnitude is economically large. We establish this finding at the macro (state) level and at the micro (inventor) level. We use for identification pre-existing state tax rates and deductibility rules to exogenously predict changes in the total tax burden facing a firm or inventor using changes in the federal tax rate only. Our estimates can therefore be interpreted as causal.

At the macro-level we establish that a one percentage point increase in either the median or top tax rate is associated with an approximately 4 per cent decline in patents, citations, and inventors, and a close to 5 per cent decline in the number of superstar inventors in the state. A one percentage point higher top corporate tax rate leads to around 6-6.3 per cent fewer patents, 5.5-6 per cent fewer citations, 4.6-5 per cent fewer inventors, and 8.5-9.3 per cent fewer superstar inventors.

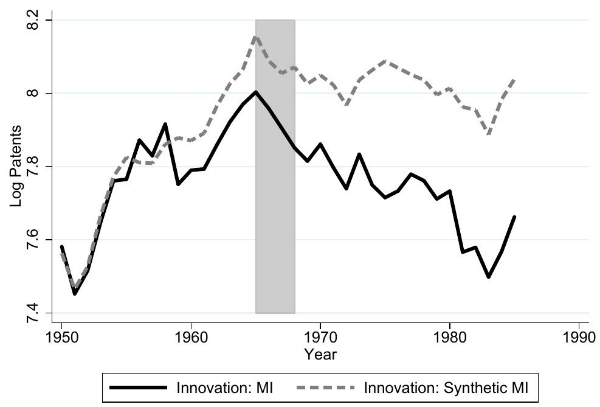

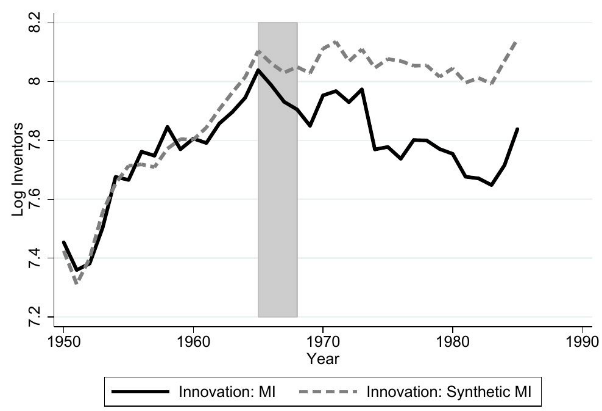

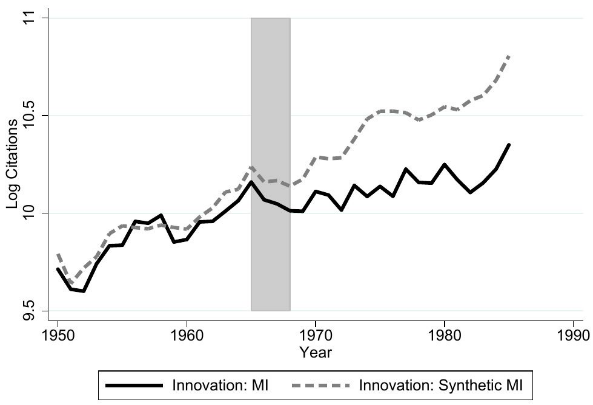

Case studies of major tax changes further illustrate the powerful suppressing effect of taxation. Figure 2, for example, shows a sharp drop in the level of innovation in Michigan relative to its peer states following the 1967 introduction of personal income tax, at a rate of 2.6 per cent and the 1968 introduction of corporate income tax, at a rate of 5.6 per cent. Michigan saw reduced patents, inventors and patent citations. Such effects, we show, cannot be fully explained by states strategically setting their tax rates to “business steal” inventors from other states.

Figure 2 – Case study of tax reform: Michigan 1967-68

a. Patents

b. Inventors

c. Citations

At the micro-level we assign inventors to tax brackets according to their productivity: it is an empirical fact that more productive inventors earn more. Again we find negative effects. A one percentage point higher tax rate decreases the likelihood that an inventor will produce a patent in the next three years by 0.63 percentage points, even controlling for inventor quality and all other state-level policy changes. The likelihood of having high-quality patents with more than ten citations decreases by 0.6 percentage points for every percentage point increase in the personal tax rate.

We also show that corporate inventors are particularly sensitive to both personal and corporate tax rates relative to non-corporate inventors. This suggests profit-sharing rules in technologically dynamic firms can influence incentives for innovation.

Finally, we establish that the location decisions of individuals and firms are affected by taxation independently of the benefits particular locations may offer. Inventors may wish to reside in places like Silicon Valley, for example, where innovation tends to cluster. But although agglomeration benefits represent an important driver of technological development, taxes still play a key role. At the corporate level, we find the higher the top corporate tax rate the less likely a firm is to locate its R&D laboratory there.

Implications for tax policy

Our analysis highlights that personal and corporate taxes matter for innovation beyond targeted tax policies such as R&D tax credits, which represent the traditional focus of policy makers. Evidence from the United States during the twentieth century suggests that higher taxes can exert a strong negative effect on innovation. While governments around the world use tax policy in an effort to redistribute income and invest in the provision of public goods, society at large benefits from innovation-led growth, which higher taxes can potentially undermine. More evidence across countries along the lines of our study would be a valuable step towards understanding the dynamics of these complex tradeoffs and their distributional implications.

- This blog post appeared previously at LSE Business Review and is based on the authors’ paper “Taxation and Innovation in the Twentieth Century” , NBER Working Paper No. 24982, presented at an event of LSE’s Centre for Economic Performance (CEP), June 2019.

- Featured image by holdentrils, under a Pixabay licence

- Please read our comments policy before commenting

Note: This article gives the views of the author, and not the position of USAPP– American Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/2JrUYsG

About the authors

Ufuk Akcigit – University of Chicago

Ufuk Akcigit is an associate professor in economics, director of graduate placement, and FY19 director of admissions at the University of Chicago. He is also affiliated with the National Bureau of Economic Research, Research, the Centre for Economic Policy Research and Koc University, Istanbul. He has a PhD in economics from MIT.

John Grigbsy– University of Chicago

John Grigbsy is a fifth year PhD student in economics at the University of Chicago, specialising in labour and macroeconomics, with particular emphasis on wage adjustments, and the labour supply of inventors. He received a B.A. with honours in economics, as well as a major in mathematics and minor in Russian from Washington & Lee University. Before attending the University of Chicago, he spent two years as a senior research analyst at the Federal Reserve Bank of New York.

Tom Nicholas – Harvard Business School

Tom Nicholas is William J. Abernathy professor of business administration at Harvard Business School. He has a PhD from Oxford University. Prior to joining HBS, he taught at MIT’s Sloan School of Management and at LSE. His current research focuses on linking historical US patent records to federal censuses to examine the life cycle of inventors and their contribution to US economic growth over the long run. He has also written a book (VC: An American History), which examines the historical roots of the development of the venture capital industry in the United States.

Stefanie Stantcheva – Harvard University

Stefanie Stantcheva is a professor of economics at Harvard University. She studies the taxation of firms and individuals, focusing on three main issues: the long-run effects of taxes on innovation, education & training, and wealth; the determinants of our social preferences, attitudes, and perceptions, which ultimately drive support for redistribution; and the effects of taxes in imperfect markets with informational frictions and rents.