Aggressive government policies to prevent a collapse of credit may be more important for the election than the rate of unemployment, write Alexis Antoniades and Charles Calomiris.

Aggressive government policies to prevent a collapse of credit may be more important for the election than the rate of unemployment, write Alexis Antoniades and Charles Calomiris.

America is in the middle of an election year. Analysts regularly speculate on how the state of the economy will affect voters. When they do so, they usually refer to unemployment or changes in income (see Fair 1978, 1996, 1998, 2002; Lewis-Beck and Stegmaier 2000). But there is evidence that, under some circumstances, changes in the supply of credit can matter even more in determining electoral outcomes. Indeed, our research suggests that the aggressive government policies that have been implemented to prevent a collapse of credit may be more important for the election than the rate of unemployment.

There are good reasons to suspect voting and credit subsidies are related: government policies subsidising homeownership have been a hallmark of American politics for nearly a century and have also figured prominently in various electoral campaigns across the world. For example, presidents George H.W. Bush, Bill Clinton, and George W. Bush all were vocal and active supporters of expanding mortgage credit subsidies. George H.W. Bush signed the GSE Act of 1992 establishing mortgage purchase mandates for low-income and urban housing for Fannie Mae and Freddie Mac. President Clinton substantially expanded those mandates and weakened FHA lending standards. President George W. Bush further expanded the GSE mandates as part of his “blueprint for the American dream.” Barack Obama has also supported expanded mortgage credit. He not only enacted a mortgage relief program, but also appointed former congressman Mel Watt in 2014 to oversee the renewed expansion of GSE credit (see Calomiris and Haber 2014).

The United States is not the only country in which housing subsidisation through cheap mortgages has figured prominently in electoral politics. Margaret Thatcher’s popularity owed in no small part to her championing of the privatisation of council flats. In the U.K. today, the credit risk subsidies from the “help-to-buy” program were the major exception from the government’s austerity policies, and prime minister Cameron has made increased housing opportunities a hallmark of his current electoral campaign. In Brazil’s 2014 election, President Dilma Roussef squeaked to a narrow electoral victory, which some observers attributed to her “Minha Casa Minha Vida” home-buying program.

Despite this suggestive evidence of a relation between electoral campaigns and credit subsidies, and despite the proven relation between the state of the macro-economy and election outcomes, prior to our study of recent presidential elections, there was virtually no microeconomic evidence of the relation between changes in credit supply and voting behaviour.

In our research, we find that voters do, in fact, punish incumbent presidential candidates for contractions in the supply of mortgage credit. We connect votes for president at the county level to county-level conditions in the mortgage market, controlling for other economic and social variables, including unemployment. Using the Home Mortgage Disclosure Act (HMDA) data on banks’ provision of mortgage credit, we identify supply shifts in mortgage credit at the county level and examine how these mortgage supply shifts affected voting in several Presidential elections. We focus first on mortgage collapse from 2004 to 2008, and connect it to the election results of 2008. 2004-2008 saw an unprecedented swing from the most generous underwriting standards for mortgages in U.S. history in 2004-2006 to a severe contraction of mortgage credit supply during the subprime crisis of 2007-2009. It also saw a dramatic swing in electoral results, with the Republican Presidential candidate winning many key swing states in 2004, but losing those same states in 2008. Were the two changes connected?

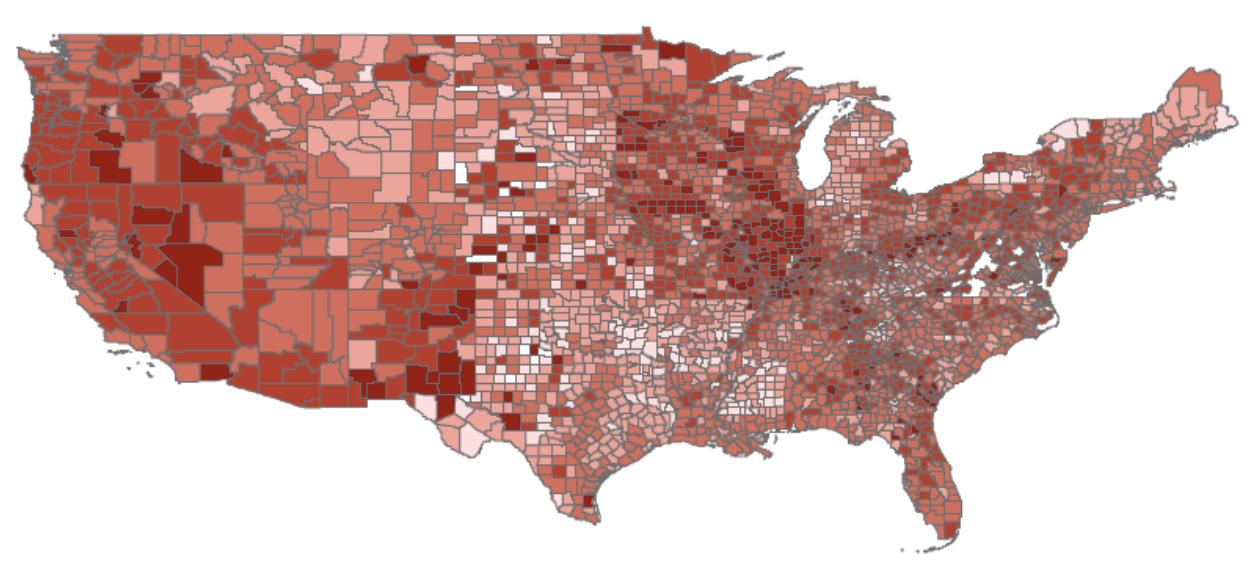

Figure 1 – Geographic representation of county-level growth in mortgage credit supply, 2004-2008

Notes: changes in mortgage credit supply at the county level between 2004-to-2008 are shown on the map of the US. Each county is represented by a cell. The magnitude of the change is colour-coded from white (no change) to dark red (large negative change). Because credit expansion occurred in only 4% of the US counties, it is not observable on the map.

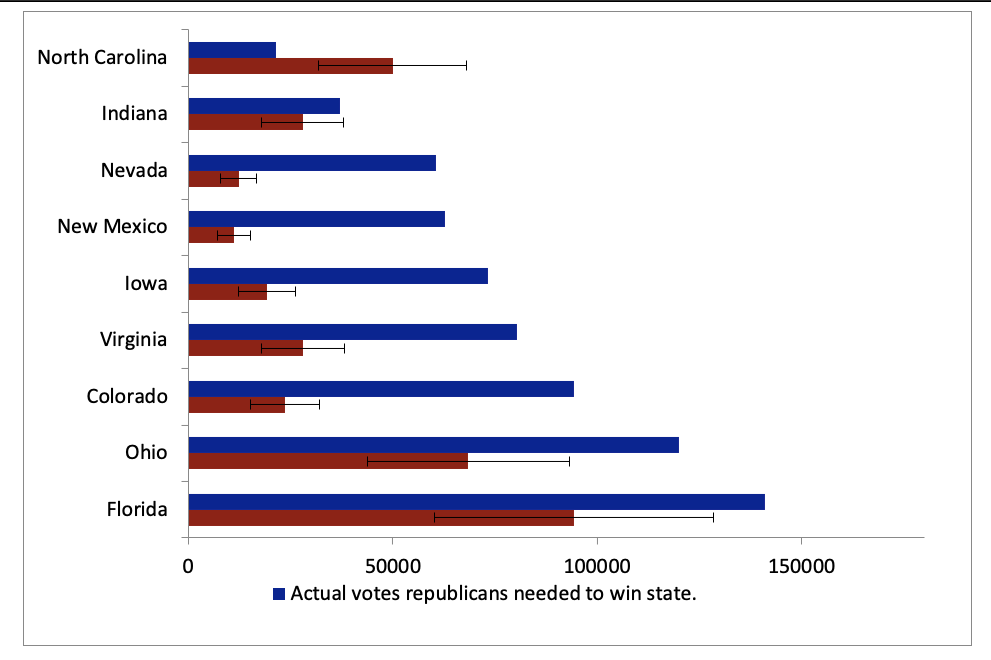

After controlling for other relevant factors, voters responded to the contraction in credit by shifting their support away from the Republican candidate in the 2008 presidential election (John McCain). The shift toward the Democratic candidate (Barack Obama) was particularly pronounced in swing states (those that have the least predictable support for either party). The magnitude of the voting impact of mortgage credit supply shifts was large. But for the mortgage credit supply contraction, some important swing states – most obviously, North Carolina – would have cast their electoral votes for McCain. In other swing states, the absence of mortgage credit supply contraction by itself would not have reversed the electoral result, but nevertheless, would have substantially narrowed the gap between votes received by McCain and Obama in 2008. Overall, if mortgage credit supply had not shifted adversely from 2004 to 2008, McCain would have received half the votes needed to capture all nine of the swing states that Bush had won in 2004 but that McCain lost in 2008, which would have reversed the outcome of the election. In that sense, the contraction in mortgage credit supply from 2004 to 2008 was five times as important as the increase in the unemployment rate; if unemployment had not increased from 2004 to 2008, that improvement in local labour markets would only have given McCain 9% of the votes he needed in those crucial swing states.

Figure 2 – Swing states electoral counterfactual, 2008

Notes: Lost votes attributed to changes in the supply of credit are shown above for swing states. Swing states are those where the Democrats won the popular vote in 2008, but not in 2004. In total, had the mortgage credit supply not changed between the 2004 and 2008 elections, the Republicans would have received 51% of the votes needed to win all swing states (82% if we add a standard deviation,). In contrast, had the unemployment rate not changed, they would have received only 9% of the votes.

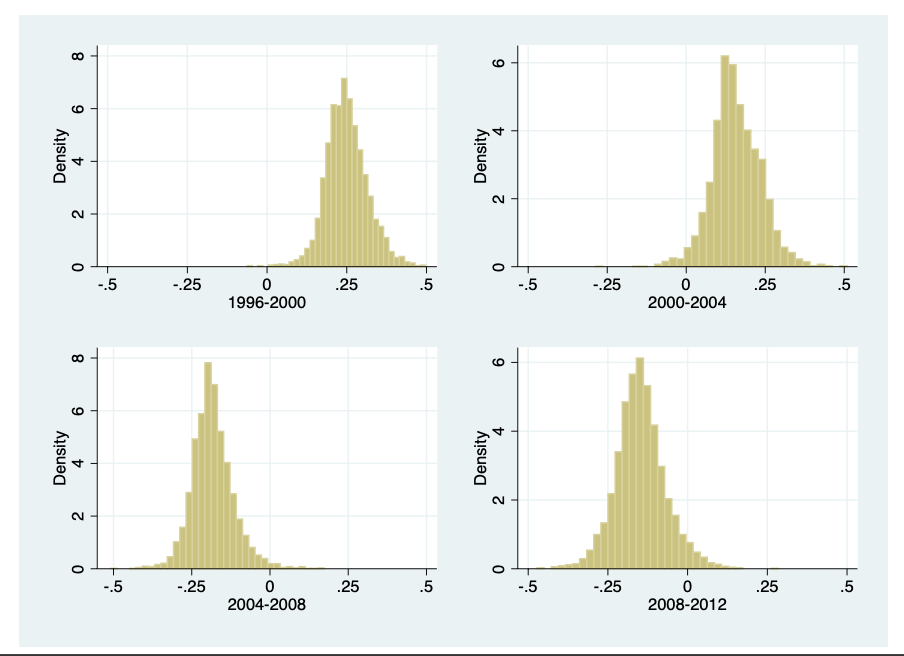

Extending our analysis to other presidential elections from 1996 to 2012, we find that contractions in credit supply from 2008 to 2012 penalised the incumbent party and benefited the candidacy of Mitt Romney. In the mortgage credit boom phase (in 2000 and 2004), however, there is no evidence that counties with relatively high credit expansion voted in favour of either the incumbent party candidate for president. Voters punish incumbent parties for mortgage credit crunches but do not reward presidential candidates of the incumbent party for mortgage credit booms. Furthermore, the asymmetric way voters react to mortgage credit changes does not vary according to the political party of the incumbent.

Figure 3 – County-level growth in mortgage credit supply between presidential elections, 1996 to 2012

Notes: Changes in mortgage credit supply by county between two election years are shown above. Four elections are covered.

Our findings have important implications for research on the politics of mortgage credit. Most importantly, our findings do not lend support to the view that presidential candidates gained direct votes from supporting the relaxation of underwriting standards for mortgage lending from 1996 to 2004. Whatever political rewards attended that support must have come from other sources (e.g., campaign contributions from special interests).

- This blog post is based on the paper Mortgage market credit conditions and U.S. Presidential elections in the European Journal of Political Economy and appeared originally at LSE Business Review.

- Featured image by Wynand van Poortvliet on Unsplash

Please read our comments policy before commenting

Note: The post gives the views of its authors, not the position USAPP– American Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: https://bit.ly/3jyOzNL

About the authors

Alexis Antoniades – Georgetown University in Qatar

Alexis Antoniades is an associate professor and director of international economics at Georgetown University in Qatar. He is an expert on understanding global markets and on the economies of the Gulf countries. Antoniades previously worked as an assistant economist at the Federal Reserve Bank of New York, was awarded a $1,050,000 research grant (2009-2012) by the Qatar National Research Fund to undertake the first micro-study on the economies of the Gulf countries, and a $867,000 research grant to use social media and analyse sentiment in the Arab World (2014-2017) in collaboration with colleagues from Qatar University.

Charles W. Calomiris – Columbia Business School

Charles W. Calomiris is Henry Kaufman professor of financial institutions at Columbia Business School, director of the Program for Financial Studies Initiative on finance and growth in emerging markets, and a professor at Columbia’s School of International and Public Affairs. His research spans the areas of banking, corporate finance, financial history and monetary economics. He is a distinguished visiting fellow at the Hoover Institution, a fellow at the Manhattan Institute, a member of the Shadow Open Market Committee and the Financial Economists Roundtable, and a research associate of the National Bureau of Economic Research.