The UK first dismissed the European Community, but later spent 12 years desperate to join it, writes Adrian Williamson. He argues that holding Brexiteers to account can be done by looking at economic history.

The UK first dismissed the European Community, but later spent 12 years desperate to join it, writes Adrian Williamson. He argues that holding Brexiteers to account can be done by looking at economic history.

The House of Commons has voted overwhelmingly to trigger Article 50, on the explicit basis that this process will be irrevocable and that, at the end of the negotiations, Parliament will have a choice between a hard Brexit (leaving the Single Market and the EEA) and an ultra-hard Brexit (WTO terms, if available).

It follows that arguments about whether the UK should remain in the EU, or should stay in all but name (the so called Norwegian option) are now otiose. What role can economic historians play as the terms of exit unfold? I think that there is an important role for scholars in seeking to analyse the promises of the Brexiteers and how feasible these appear in the light of previous experience.

Thus far, the economic debate over Brexit has been conducted on a very general basis. Remainers have argued that leaving the EU spells disaster, whereas Leavers have dismissed such concerns and promised a golden economic future. But what exactly will this future consist of? Doing the best one can, the Brexit proposition must surely be that the rate of economic growth per capita will be significantly higher in the future than it would have been if the UK had retained its EU membership. Since, at the same time, there was to be a massive and permanent reduction in EU and non-EU immigration (from c.330,000 p.a. net immigration to ‘tens of thousands’), it is per capita improvements that will have to be achieved.

Featured image credit: Cameron v Farage, by DAVID HOLT, under a CC-BY-2.0 licence.

The path to this goal will, it is said, be clear once the UK leaves. In particular:

- the UK will be able to make its own trade deals and become a great global trading nation;

- the UK can develop a less restrictive regulatory framework than that imposed by the EU;

- industries such as manufacturing, fisheries and agriculture will revive once the country is no longer ‘tethered to the corpse’ of the EU;

- the post-referendum devaluation will provide a boost for exporters.

In relation to each of these claims, there is plenty of helpful evidence from economic history. After all, the UK was the first nation to embrace a global trading role. As Keynes pointed out in a famous passage, in 1914:

The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep; he could at the same moment and by the same means adventure his wealth in the natural resources and new enterprises of any quarter of the world, and share, without exertion or even trouble, in their prospective fruits and advantages…

Yet, despite this background, and despite the economically advantageous legacies of Empire, the UK spent the period between 1961 and 1973 making increasingly desperate attempts to join a (then much smaller) Common Market. British policymakers were initially dismissive of the European Community. Exports to the Six were thought less important than trade with the Commonwealth. Britain’s initial response was to establish EFTA as a rival free trade area. However, it soon became apparent that this arrangement was lopsided: Britain was part of a free trade area with a population of 89m (including its own 51m), but stood outside the EEC’s tariff walls and population of 170m. Will the 2020s be different from the 1960s? In any event, ‘free trade’ is an elusive concept. As John Biffen, a Tory Trade Minister in the Thatcher government (and no friend of the EU), acknowledged, free trade has never existed ‘outside a textbook’.

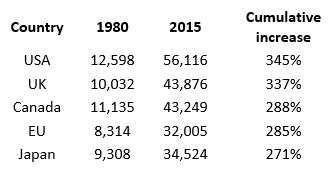

As regards decoupling from EU regulations, the UK was, of course, completely free to devise its own regulatory framework prior to accession to the EU in 1973. Nonetheless, in this period, much of the current labour market structure, such as protection against unfair dismissal and redundancy, was enacted. EU regulations, such as the Social Chapter, have complemented, not undermined, this domestic framework. In any event, does the evidence suggest that a mature economy, such as the UK, will be able to establish a more rapid rate of growth with a looser regulatory framework? The obvious comparisons in this respect are the developed North American and Japanese economies. The data suggests that the UK has performed extremely well within the EU framework.

Table 1. GDP per capita (current US$)

Source: World Bank

Of course, much higher rates of growth have recently been achieved in developing economies such as China and India. But it cannot seriously be argued that an economy like the UK, which underwent an industrial revolution in the eighteenth century, can achieve rates of progress comparable to economies that are industrialising now. The whole course of economic history shows that mature economies have much slower rates of growth and that the increases achieved by the USA and the UK over the last few decades are close to optimum performance.

The maturity of the UK economy is also germane to arguments suggesting that it will be possible to revive industries that have suffered long term decline, such as manufacturing, agriculture and fisheries. After all, one consequence of the UK’s early start in manufacturing is that primary industries declined first and most rapidly here. Economic historians have been pointing out since the 1950s that in advanced economies the working population inevitably drifts from agriculture to manufacturing and then from manufacturing to services. In 1973, the American sociologist Daniel Bell greeted the arrival of the post-industrial society. He pointed out that the American economy was the first in the world in which more than 60 per cent of the population were engaged in services, and that this trend was deepening in the USA and elsewhere. Brexit is scarcely likely to reverse these very long-term developments.

The British economy has also had considerable past experience of enforced devaluation (for example in 1931, 1949 and 1967). Research following the 1967 devaluation suggested that a falling pound gave only a temporary fillip to the trade balance, whilst delivering a permanent increase in inflation. Over the same period the West German economy performed extremely strongly, despite a constantly appreciating currency.

Finally, one may question whether the UK can achieve an economic miracle whilst, at the same time, pursuing a very restrictive approach to immigration. Successful economies tend to be extremely open to outsiders, who are both a cause and a consequence of growth. After all, in the pre-1914 golden age to which Keynes referred, there were no controls at all, and the British businessman ‘could secure forthwith, if he wished it, cheap and comfortable means of transit to any country or climate without passport or other formality…and could then proceed abroad to foreign quarters…and would consider himself greatly aggrieved and much surprised at the least interference’. Our putative partners in trade deals are not likely to be offering such access and, if they do, they will want substantial concessions in return.

Of course, past performance is no guarantee of future prosperity. Historic failure does not preclude future success. And sections of British public opinion have, it appears, ‘had enough of experts’. Even so, economic historians can hold up to scrutiny some of the more extravagant claims of the Brexiteers.

This blog post was originally published in The Long Run (the blog of the Economic History Society) and LSE Bussiness Review. Featured image credit: Cameron v Farage, by DAVID HOLT, under a CC-BY-2.0 licence.

The post gives the views of its author, not the position of LSE Brexit or the London School of Economics.

Adrian Williamson has been a practising barrister in Keating Chambers since 1989, specialising in construction disputes. He was called to the Bar in 1983 and was appointed QC in 2002. He completed a PhD in Economic History in 2014 at Cambridge, supervised by Professor Martin Daunton, and was elected a Fellow of the Royal Historical Society in 2015. He has since published extensively on, amongst other things, Thatcherism and Labour history.