The 2008 market crisis was notable in the UK relative to previous recessions for three things: the enormity of the output shock; the muted unemployment response; and the very slow rate of recovery. The initial drop in GDP of 5 per cent was steeper than in previous recessions and the UK economy has performed particularly poorly in the years since.

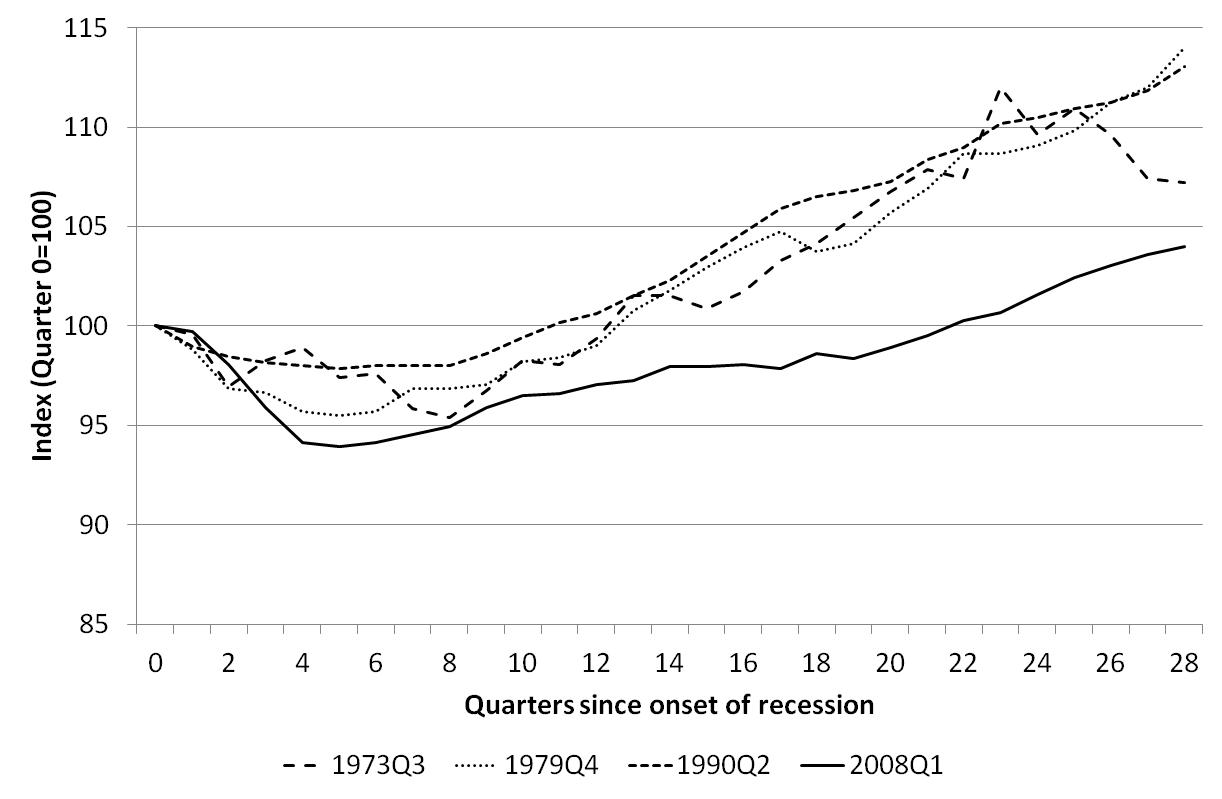

In 2014, output per hour remained 0.4 percentage points below the level seen in the pre-recession year of 2007 (Figure 1).

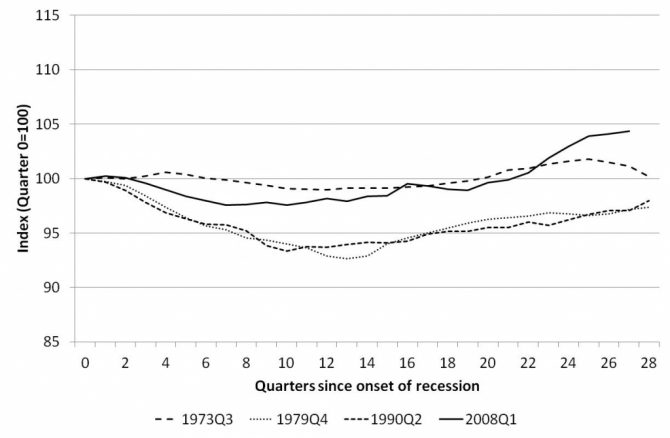

Yet at the same time, although employment levels fell, they didn’t fall by anything like what we might have expected from previous recessions and the fall was considerably smaller than the decline in GDP (Figure 2).

Furthermore, employment recovered more quickly, exceeding its pre-recession level in 2012 Q3 (a full year before the recovery in output).

Poor GDP growth and sustained employment levels combined to push down output per worker. The fall in output per hour was not as substantial in the period immediately after the recession, since a growth in part-time working meant that hours per worker fell more steeply than employment; but there has been no overall progress on either measure since 2007.

Why has economic growth taken so long to recover? And why has the labour market responded so differently this time compared with earlier recessions?

The UK’s ‘productivity puzzle’ is, in effect, two puzzles. First, why has economic growth taken so long to recover? And second, why has the labour market responded so differently this time compared with earlier recessions? In neoclassical economics, firms respond to demand shocks by laying off workers, thus maintaining labour productivity. Yet this didn’t happen – at least, not to the same extent as in previous recessions. Another related puzzle is why economic growth has taken so long to return post-recession, and what can be done about it?

Salient Fact Number One: as Rebecca Riley and others have pointed out, output per worker declined in most sectors and in most firms. In contrast to Germany where it was confined to the export sector, the UK recession was felt by the vast majority of firms and workers, although of course some were hit more heavily than others.

Salient Fact Number Two: any cleansing effect due to the recession killing the least productive firms was very muted indeed: the long tail of poorly productive firms remained in place. These firms have dragged down overall productivity.

Salient Fact Number Three: the unprecedented fall in output was accompanied by a large decline in real wages not seen since the nineteenth century — all the more surprising in light of historically low inflation rates. Although economists have yet to identify the mechanisms that led to this real wage decline, some point to the declining bargaining power of trade unions and employees. Whatever the cause, this real wage decline may have encouraged employers to retain labour at a time when, if their price relative to capital had been higher, workers would have been laid off. Many employers were therefore able to pay those wages and were minded to do so, rather than lay workers off, partly because many came into the recession after a period of good profits – unlike in the early 1990s. Some wished to avoid the heavy costs involved in firing high-skilled labour only to have to re-employ it in the inevitable upturn.

Declining labour costs means that firms may have been tempted to substitute labour for capital, resulting in capital shallowing – a process that would ordinarily result in declining labour productivity. There are difficulties in estimating capital stocks and flows, but this appears not to have happened to any great extent. Instead, what has emerged is Salient Fact Number Four: firms experienced a decline in total factor productivity (TFP) which identifies the efficiency with which all factors of production are deployed to create output.

There is general acceptance of these four salient facts, but little agreement about the underlying causes of the productivity decline. Most explanations have some traction, but not much. What is becoming clear is that the crisis may have persistent effects on the UK’s productivity due to reduced investment in physical and intangible capital, and impaired resource allocation.

In the longer run, the productivity trends are likely to reflect the long tail of poorly performing firms that the UK has been noted for over many years. Some of this is due to structural factors such as ‘poor management’. Perhaps the problem is compounded by policy choices: governments have traditionally been reluctant to interfere with managers’ right-to-manage, even when those managers appear poorly equipped for the job.

Despite this, there are some areas where optimism is merited. London is a global centre, one of only a few truly international ‘hub’ cities benefiting from agglomeration and networking. It offers safe haven for international capital, migrant labour flows and talented entrepreneurs. More broadly, a number of reforms have been undertaken since the 1980s: the expansion of higher education, reforms to welfare systems and labour law, and deregulation of capital flows. It remains to be seen whether the UK can benefit from these good foundations to make up the ground it has lost in recent years.

Note: This is a shorter version of the blog post published in LSE British Politics and Policy — based on Bryson, A. and Forth, J. (2015) ‘The UK’s Productivity Puzzle’, NIESR Discussion Paper No. 448 and CEP Occasional Paper No. 45. The final version will appear in ‘Productivity puzzles across Europe’, P. Askenazy et al. (eds), forthcoming.

Featured Photo Credit: Chris Yarzab CC BY-NC-SA-2.0

Alex Bryson is Visiting Research Fellow, Labour Markets Programme at the Centre for Economic Performance and Head of the Employment Group at the NIESR.

John Forth is Principal Research Fellow at the NIESR.