There are three main longer term factors that determine how our economy performs. These are:

- Population trends (demography);

- Technical know-how (innovations);

- How we manage ourselves (governance and education).

There is debate whether innovation is currently slowing or accelerating, and governance questions are always with us. But this blog is primarily about demography, and its influence on monetary policy, largely taken from a joint paper with Manoj Pradhan, presented at BIS Conference, June 2016.

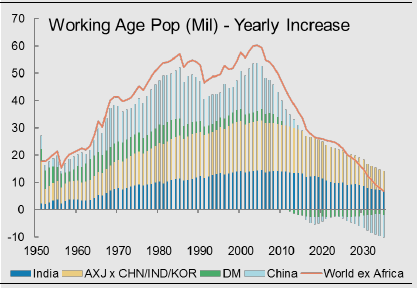

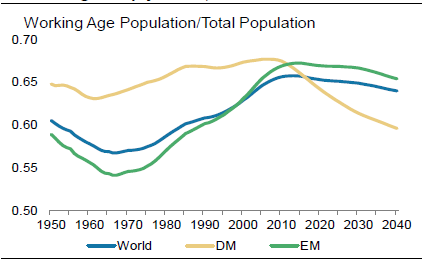

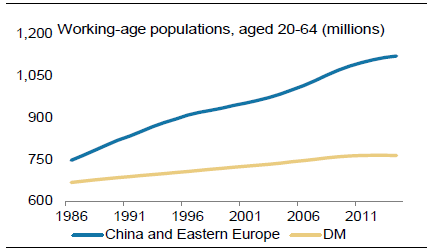

After WWII, there was a baby boom, followed by a declining birth rate, with a subsequent rise in life expectancy, thereby causing a sharp increase in working population, and a falling ratio of dependants (children below 20, aged above 65) to workers, [Charts 1 and 2]. This was compounded by the inclusion of China and Eastern Europe, after the USSR collapsed, into the global, trading system, [Chart 3).

So, between 1980s and 2000s, the world, both developed (DM) and emerging market (EM) economies, absorbed the largest ever positive worldwide supply shock. Such demographic forces played a major role in the following trends:

- Off-shoring, with a shift of manufacturing production to N. Asia, especially to China;

- Stagnation or even decline in real wages of median workers, as labour became much more plentiful;

- A collapse in membership and power of private sector Trade Unions;

- An increase in inequality within countries, but a decrease in inequality between countries;

- Deflationary pressures, apart from commodity prices;

- Decreases in nominal and real interest rates.

But now these demographic trends, which have favoured the top one per cent, but not the lower 90 per cent, in income distribution, are reversing. The growth of the working population will fall, relative to the growing numbers of old. The ratio of dependants to workers will rise virtually everywhere.

This could indicate a reversal of previous trends, thus,

- A reversion to national production, (less free trade);

- Rising real wages, and greater labour power;

- Less inequality within countries;

- More inflation; not only will unit labour costs rise, but taxation will have to rise sharply to pay for the old’s medical services and pensions;

- Higher nominal, and perhaps, real interest rates.

Mitigants to such reverse trends include:

- The age of retirement is rising and the relative generosity of support for the old may fall. Perhaps, but politically difficult.

- Robots may take over, so wages for the less educated may remain submerged. But the relative fall in working population is so great that we will need much more robotics.

- India and Africa could play the role of China and Asia as the source of ever more cheap labour, either by migration out or by inflows of capital and management. Doubtful; migration is too socially disruptive, and infrastructure and governance required for India/Africa to play the role of China/Asia is not yet in place.

Perhaps the strongest rejoinder to this thesis came in response to our view that demographics would lead to a future rise in nominal and real interest rates. Part of this came from a denial that worsening dependency ratio would lead to the wish to save falling faster than the desire to invest. But the strongest argument against our view of a turn-around in interest rates was that macro-economic policy had led us into a debt trap.

Low interest rates had been the preferred response to insufficient demand and deflation over these decades, and this encouraged a massive expansion of debt. Such increases in debt ratios have not yet had a seriously adverse effect on world growth, since they were offset by falling interest rates, leaving debt service ratios stable, or declining. But this cannot continue, having reached the zero lower bound (ZLB).

Meanwhile, real growth must fall, on account of slower growth of the working population. Moreover, expansionary monetary policy is losing power. So nominal interest rates will tend to rise, but only glacially, relative to slowing growth rates of nominal incomes, but that will still cause the burden of the debt overhang to worsen.

As the US recovers from the global financial crisis and tries to renormalize interest rates, the adverse effect of that on the rest of the world feeds back to the US economy, and thereby slows down that rise. But at some point (who knows when?), labour market tightening in recovering countries, driven by demographic change, will put upwards pressure on wages, unit labour costs and inflation. The Phillips curve is sleeping, not dead. What then? A mixture of defaults in the weaker countries/sectors, and inflation in the stronger countries/sectors?

♣♣♣

Notes:

- This post is based on the author’s paper Demography versus Debt, co-authored with Manoj Pradhan, presented at BIS Conference, June, 2016.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: moerschy, Pixabay, CC0

- Before commenting, please read our Comment Policy

Charles Goodhart, CBE, FBA is Emeritus Professor of Banking and Finance with the Financial Markets Group at LSE, having previously, 1987-2005, been its Deputy Director. Until his retirement in 2002, he had been the Norman Sosnow Professor of Banking and Finance at LSE since 1985. Before then, he had worked at the Bank of England for seventeen years as a monetary adviser, becoming a Chief Adviser in 1980. In 1997 he was appointed one of the outside independent members of the Bank of England’s new Monetary Policy Committee until May 2000. Earlier he had taught at Cambridge and LSE. Besides numerous articles, he has written a number of books. His latest titles include The Basel Committee on Banking Supervision: A History of the Early Years, 1974-1997, (2011), and The Regulatory Response to the Financial Crisis, (2009).

Charles Goodhart, CBE, FBA is Emeritus Professor of Banking and Finance with the Financial Markets Group at LSE, having previously, 1987-2005, been its Deputy Director. Until his retirement in 2002, he had been the Norman Sosnow Professor of Banking and Finance at LSE since 1985. Before then, he had worked at the Bank of England for seventeen years as a monetary adviser, becoming a Chief Adviser in 1980. In 1997 he was appointed one of the outside independent members of the Bank of England’s new Monetary Policy Committee until May 2000. Earlier he had taught at Cambridge and LSE. Besides numerous articles, he has written a number of books. His latest titles include The Basel Committee on Banking Supervision: A History of the Early Years, 1974-1997, (2011), and The Regulatory Response to the Financial Crisis, (2009).

Will matter more in US, as most workers will be poor since maj of students in public schools already poor.