Often unnoticed by business leaders in Europe, Chinese technology companies are on the move. Hardly a week goes by without news that Alibaba has acquired a company in Southeast Asia, Tencent has invested in an Israeli startup or that Baidu is entering a new industry. Western onlookers may think that this is unlikely to have a direct impact on their businesses. And if they are concerned or interested, often the deals are more complex and opaque than first imagined. Chinese companies are generally reticent about communicating their strategies. They also often make investments through companies inside their ecosystem, through subsidiaries or companies in which they own a stake (sometimes undisclosed).

But, there are three important reasons why the rise of digital China cannot be ignored: the scale and speed of Chinese tech investments in Europe; the unique Chinese approach to organization; and the innovation imperative for Chinese companies leveraging a comparative advantage in technology rather than cost.

Scale and speed of Chinese tech investments in Europe

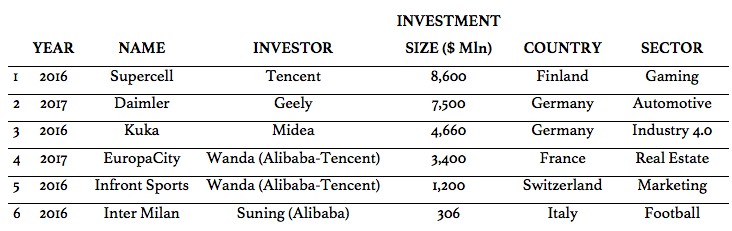

China’s Baidu, Alibaba and Tencent – known by the acronym BAT — are the leading Chinese internet companies. With a combined market capitalization of close to $1 000 billion, billions of users and business activities in over 20 sectors, BAT cannot be ignored. In the last five years alone, BAT have made direct investments and acquisitions of 11 companies in Western Europe — including WayRay (Switzerland), Nestpick (Germany), Indoor Atlas (Finland), Lilium Aviation (UK), and Supercell (Finland). Table 1 summarizes the six largest investments by Chinese tech giants in Europe.

The investments are large and wide-ranging:

- WeChat, the Chinese multi-purpose app by Tencent, has over one billion active users worldwide. Its WeChat Pay was recently launched in Europe (Italy, France, UK, Germany). Tencent has also invested (along with Allianz) $160 million in N26, a European startup based in Berlin that aims to revolutionize the traditional banking industry. WeChat Pay’s expansion follows that of Alipay, a payment platform by Alibaba, which is already linked with BNP Paribas, Barclays, UniCredit and six payment services, enabling 930,000 merchants to join its payment network.

- Consider the Chinese conglomerate Dalian Wanda Group. At the beginning of 2018 Wanda sold a combined 13 percent of its film business Wanda Film for $1.24 billion to Alibaba and a state-owned investment group, and 14 percent of its real estate business, Dalian Wanda Commercial Properties Co., for $5.4 billion to Tencent Holdings. Wanda, along with the French retail group Auchan (already partnering with Alibaba in the Chinese retail market), is planning to invest $3.4 billion to build a shopping and leisure complex near Paris. Wanda has also acquired the Swiss marketing company Infront Sports for $1.2 billion. Infront is a partner of FIFA, the German and Italian Football Federations, and Italy’s Lega Serie A.

- At the end of 2016 Tencent and Alibaba invested $360 million in Bona Film Group a leading film distributor in China,Korea, Southeast Asia, the United States and Europe with an integrated business model encompassing film distribution, production, exhibition and talent representation. Furthermore, Wanda (backed by Alibaba and Tencent) will work with Alibaba in film production, film investment, film advertisement and other businesses. Wanda Group is the owner of Odeon & UCI Cinemas Group, the largest cinema chain in Europe with about 250 cinemas and a market share of 20 per cent. In this way, all the value chain from the production to distribution until movie projection is under the control of three Chinese players.

- The carmaker Geely acquired the Swedish car company Volvo in 2010 and Taxi London in 2013. In 2017 it took control of the British company Lotus and, at the beginning of 2018, became the first stakeholder of Daimler, acquiring about 10 per cent of the company for $7.5 billion. Moreover, in 2017 Geely invested £300 million in a new factory in England to produce up to 5,000 electric vehicles by 2019 aiming at replacing “traditional” taxis with emission-free engines.

- The leading German robotics firm Kuka was acquired by the Chinese appliance producer Midea. Kuka is the pioneer of Industry 4.0, playing a fundamental role in the strategy of Germany and Europe. This acquisition raised business and security concerns from politicians who suggested that Chinese investments might become a strategic threat to the country’s industrial leadership.

Table 1. The six largest investments by Chinese technology companies in Europe (2016-present)

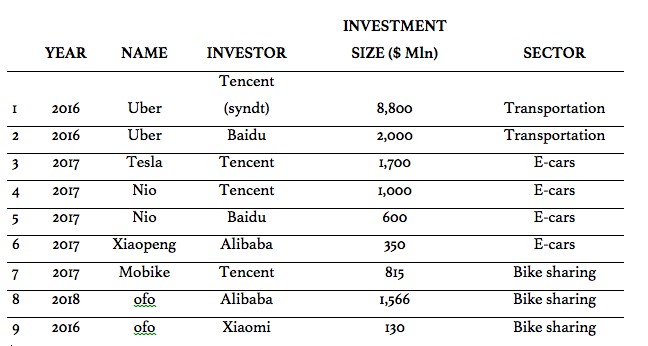

Amid this frenzy of purchases, one particular battlefield is especially noteworthy: mobility. Geely, in addition to a stream of investments in the automotive sector, is involved in car sharing with the only pure electric provider, Share’ngo. The company, is already active in Italy, the Netherlands, France and (soon) Spain.

Alibaba and Tencent are also consolidating their presence in the mobility industry through many strategic investments. They already own important stakes in Tesla and Uber, as well as in extremely innovative Chinese players, such as Nio and Xiaopeng, which are targeting the global market.

Another mobility area with increasing Chinese investment is bike-sharing. Alibaba, Tencent and Xiaomi have made heavy investments in this area, most notably in ofo and Mobike which are both now highly active in Europe. The two fast-growing bike sharing companies offer the tech giants access to a large quantity of data — such as email addresses, credit card payments, personal mobility habits etc. – which may prove very useful as it is leveraged in the wider ecosystems of the Chinese tech giants.

Table 2. Largest investments by Chinese technology companies in the mobility sector with impacts in Europe (2016-present)

Unique approach to organizing: The business ecosystems

Chinese technology companies are highly aggressive in comparison with the globally known US technology companies. Amazon, with its willingness to move quickly across industries, is the only company which is comparable. In addition, Western digital players tend to build business in-house instead of buying or investing in external companies and building extensive digital ecosystems. Indeed, business ecosystems – as exemplified by the Chinese tech giants — are new organizational forms where the businesses are interdependent through a variety of equity relationships combining product and service offerings into a customer-centric offering (Greeven and Wei, 2018).

Chinese digital players have what can be described as a deep omnichannel vision. Companies like BAT invest, collaborate, acquire and incubate ventures in sectors that can be digitally connected to their core platforms. Whether it is connecting to the 700 million users in Alibaba’s e-commerce core business or the one billion users of Tencent’s WeChat, via payments, cloud services, social media or any other type of organizational glue, Chinese digital players focus on expansion into new opportunities. They maintain their speed of expansion at a level unheard of for most multinationals or even US tech players.

Figure 1 visualizes Alibaba’s business ecosystem with at the core its e-commerce platforms and a second layer of interdependent services, i.e. the ‘glue’. While Alibaba has been spreading Alipay across Europe and making partnerships with players from completely different industries (including Wanda, Bona Group, Auchan, Suning), it is also scouting locations for a second European Data Center, after establishing its first in Frankfurt, a clear hint of future size expectations.

Ecosystems are not only growing online. For example, Alibaba along with Auchan purchased 72 per cent of Sun Art Retail Group (for $2.8 billion each) a leading Chinese hypermarket operator. It would be no surprise if one day Alibaba was investing in new supermarkets in Europe with or without the support of Auchan, the French supermarket chain.

Figure 1. Alibaba’s business ecosystem

Source: Adapted from Greeven and Wei (2018)

China’s innovation imperative and comparative advantage in technology

Putting the speed, scale and approach of Chinese digital giants in Europe in a broader context, we need to understand that innovation in and from China is not a fad. China has transformed from imitation to innovation in just a generation; an evolution going hand in hand with the development of China’s entrepreneurial private sector.

Of the “50 Smartest Companies 2017”, published by the MIT Technology Review, seven were Chinese — iFlytek, Tencent, Face ++, DJI, Alibaba, Ant Financial and Baidu. Moreover, Face ++, a Chinese startup valued at $2 billion was considered one of the top “10 Breakthrough Technologies 2017” worldwide.

The reality is that Chinese companies have no choice but to innovate and upgrade in global value chains. Their domestic competitive landscape is highly competitive and innovation advantages are necessary. Entry into Europe by many of China’s largest tech companies is a necessity, as they are looking for market experience, leveraging new technology and exposing themselves to international business.

We have not even seen the real beginning of the international journey of Chinese digital giants. More is to come, as it is imperative to China’s business world.

It is also worth noting that while Chinese companies no longer have a cost advantage, they do have a technology advantage. Chinese companies are globally number one in fintech; number two in virtual reality, autonomous driving, wearables, robotics, drones, and 3D printing; and number three in big data and artificial intelligence (McKinsey, 2017). Chinese research in deep learning for artificial intelligence applications has seen the largest growth rate, closing in on the US, while European companies are hardly increasing AI research and development. AI has been supported by recent national government policies in China. Already, there is a Chinese white paper on developing technology standards for AI. Combined with markets, capital and ambitious entrepreneurs, Chinese companies have a strong technology advantage to leverage in Europe.

Connecting to digital China in Europe

For European executives it is vital to understand what is happening and react as fast as possible, either to grasp an opportunity or to be ready to face an emerging threat. First, they should know and analyze in detail the latest solutions, value propositions and business models of the Chinese digital players, identifying the most innovative and disruptive elements. In several cases they can be taken as innovation benchmarks.

As they are very unpredictable, it is crucial to map the different ecosystems to derive insights on whether and how Chinese players will penetrate a particular market space. Designing interconnections among the companies inside ecosystems helps understand the overall business models and next strategic moves. This is critical to define the best strategies to connect, partner or compete against them.

♣♣♣

Notes:

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Baidu, by simone.brunozzi, under a CC-BY-SA-2.0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Mark J. Greeven is a Chinese-speaking Dutch Professor of Innovation based in China for over a decade and author of Business Ecosystems in China (2018, Routledge) and China’s Emerging Innovators (2019, MIT Press).

Mark J. Greeven is a Chinese-speaking Dutch Professor of Innovation based in China for over a decade and author of Business Ecosystems in China (2018, Routledge) and China’s Emerging Innovators (2019, MIT Press).

Paolo Cervini is a Partner with ECSI, a global strategic innovation consultancy. He has 20 years in management consulting for multinational and national companies across Europe and the US on strategy and business transformation. His expertise is in innovation, profitable growth, commercial excellence and organisational change.

Paolo Cervini is a Partner with ECSI, a global strategic innovation consultancy. He has 20 years in management consulting for multinational and national companies across Europe and the US on strategy and business transformation. His expertise is in innovation, profitable growth, commercial excellence and organisational change.

1 Comments