The sensitivity of corporate bond returns to changes in the value of equity is a fundamental input for portfolio asset allocation. Since imperfect correlation of asset returns is a key assumption in portfolio theory, stock-bond return co-movement is important to determine the diversification benefits of bonds, and to hedge common exposures across the two asset markets. Because bonds exhibit on average lower expected returns, a higher stock-bond return co-movement implies a greater allocation to equities.

The finance literature has extensively studied the phenomenon of stock-bond return correlation at the aggregate level, providing evidence on how macroeconomic factors impact the return association across portfolios of stocks and bonds. Prior studies find that stocks and bonds exhibit a positive return co-movement with substantial time-series variation. However, evidence on stock-bond co-movement at the firm level (i.e., return correlation between stocks and bonds issued by the same firm) is surprisingly scant.

Similar to aggregate co-movement, understanding firm-specific stock-bond return correlation and its cross-sectional determinants is important for asset allocation. This is because wealth transfers from debt holders to shareholders are likely correlated across firms (especially during periods of economic downturn) and hence very difficult to diversify.

In a recently published paper, I examine how an important attribute of financial reporting quality, accounting conservatism, affects stock-bond return co-movement at the firm level. Companies’ financial statements are usually regarded as “conservative” if managers require a higher degree of verification to recognise possible future gains vis-à-vis possible future losses. This reporting convention typically leads companies to prudently understate, rather than overstate, their net assets. Prior research has shown that conservative financial statements can contain management’s opportunistic behaviour by mitigating moral hazard problems. Similarly, I argue that conservative financial reports provide bondholders with a credible and contractible signal that improves monitoring thus preventing wealth transfers.

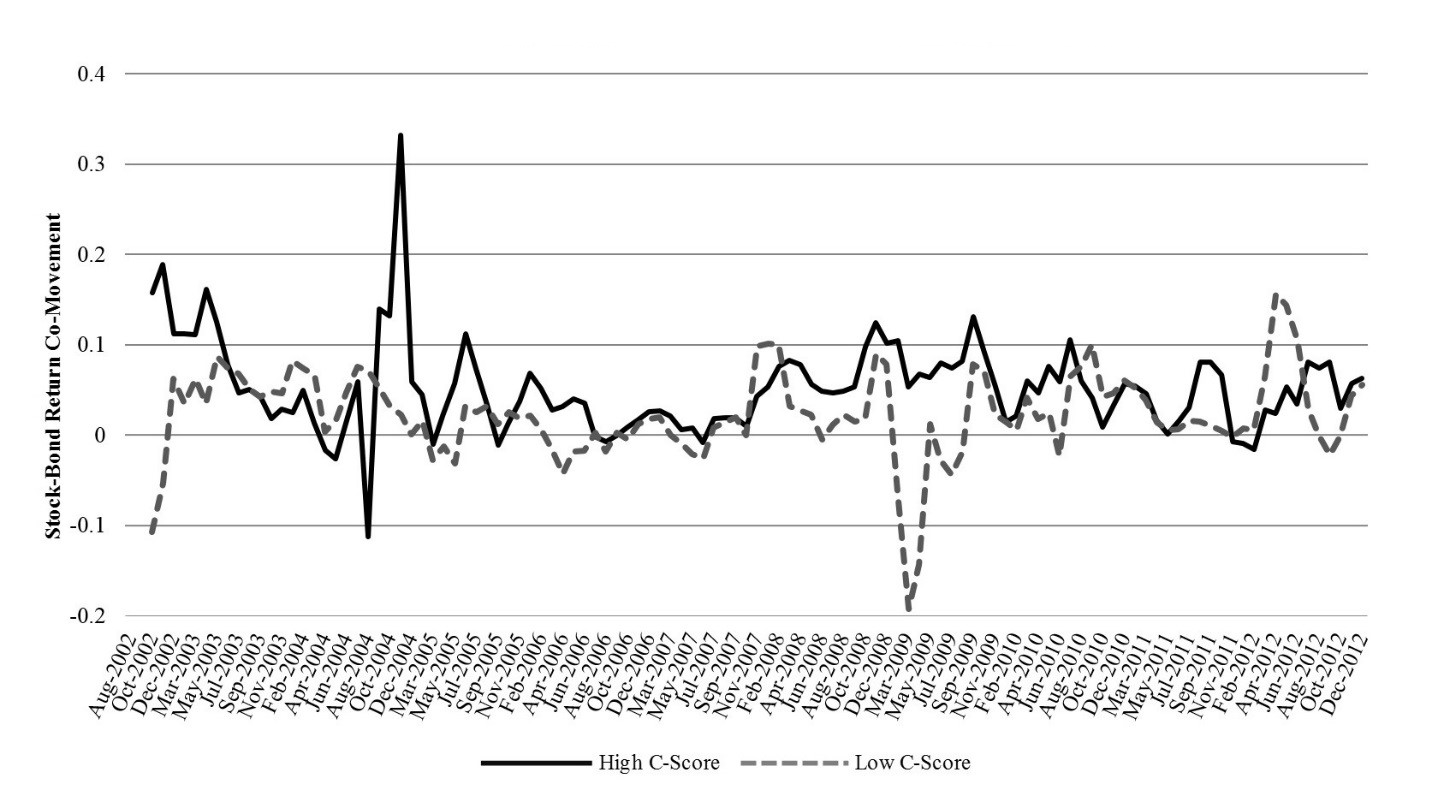

Figure 1. Stock-bond return co-movement time series for high versus low conservatism

According to structural models of default risk, an upward revision in firm expected cash flow should increase both the value of equity (because of increased profitability) and the value of debt (because of lower bankruptcy risk). Hence, stock and bond returns should exhibit a positive correlation on average. However, differences in the payoff structures of shareholders and bondholders may give rise to agency conflicts. Shareholders may expropriate bondholders’ wealth by engaging in risk shifting activities (i.e., by switching from safe to risky investments). These wealth transfers from bondholders to shareholders represent a manifestation of agency problems which reduce (or even reverse) the correlation between stock and bond returns.

My study provides evidence that accounting conservatism increases the extent of stock-bond return co-movement. Firms that choose to report conservatively provide a timely and credible signal to bondholders. This is in line with the conjecture that conservative financial reports improve bondholders’ ability to monitor managerial actions and effectively intervene if needed.

Furthermore, I find that the effect of accounting conservatism on stock-bond return co-movement is more pronounced when default risk is higher and debt maturities are longer. Finally, in line with findings from prior research, I show that conservatism and bond covenants jointly increase stock-bond return co-movement.

My findings are relevant for financial reporting regulators, auditors, and investors. By showing how the quality of financial reports in general, and accounting conservatism in particular, affects firm-specific stock-bond return co-movement, my research offers important insights for portfolio asset allocation. Firm-specific co-movement matters for asset allocation decisions because wealth transfers from debt holders to shareholders are unlikely to be independent across firms and, as a result, are difficult to diversify. Especially in periods of economic downturn, debt-equity conflicts may deteriorate systematically across firms in the economy, and thus many firms may exhibit wealth transfers at the same time. Consequently, understanding how accounting conservatism relates to firm-level co-movement of equity and bond returns is of importance for the optimal allocation of funds across the two asset classes.

♣♣♣

Notes:

- This blog post is based on the author’s paper Stock-Bond Return Co-Movement and Accounting Information, Journal of Business Finance and Accounting, 2017, Volume 44, Issue 7-8, pages 1036-1072.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Photo by StockSnap, under a CC0 licence

- When you leave a comment, you’re agreeing to our Comment Policy.

Stefano Cascino is an assistant professor of accounting at LSE. His primary research interests include disclosure regulation, corporate governance and credit markets. He has been a visiting researcher at the Humboldt University of Berlin (Germany) and at the Queensland University of Technology (Australia). His research has been published in leading accounting journals and has generated the interests of practitioners and standard setters including the International Accounting Standards Board (IASB). His research has also been cited in academic media outlets such as the Columbia Law School Blue Sky Blog and the Harvard Law School Bankruptcy Roundtable. He has received funding and research grants from the Institute of Chartered Accountants of Scotland (ICAS) and the European Financial Reporting Advisory Group (EFRAG). He is a member of the editorial board of Accounting and Business Research. For his dedication to teaching, he received in 2012 the LSE Teaching Excellence Award, and the LSE Education Excellence Award both in 2016 and 2017. He holds a PhD in Business Economics (Accounting) from the University of Naples Federico II and is a Certified Public Accountant (CPA) and Registered Auditor (Italy).

Stefano Cascino is an assistant professor of accounting at LSE. His primary research interests include disclosure regulation, corporate governance and credit markets. He has been a visiting researcher at the Humboldt University of Berlin (Germany) and at the Queensland University of Technology (Australia). His research has been published in leading accounting journals and has generated the interests of practitioners and standard setters including the International Accounting Standards Board (IASB). His research has also been cited in academic media outlets such as the Columbia Law School Blue Sky Blog and the Harvard Law School Bankruptcy Roundtable. He has received funding and research grants from the Institute of Chartered Accountants of Scotland (ICAS) and the European Financial Reporting Advisory Group (EFRAG). He is a member of the editorial board of Accounting and Business Research. For his dedication to teaching, he received in 2012 the LSE Teaching Excellence Award, and the LSE Education Excellence Award both in 2016 and 2017. He holds a PhD in Business Economics (Accounting) from the University of Naples Federico II and is a Certified Public Accountant (CPA) and Registered Auditor (Italy).