One of the great concerns for EU states over the on-going situation in Crimea is their reliance on Russian gas to meet their energy demands, with around 60 per cent of these imports being delivered through pipelines in Ukraine. Jack Sharples and Andy Judge provide a comprehensive assessment of what the impact would be if the transit routes via Ukraine were suspended. They note that while the situation has generally been portrayed as an ‘EU problem’, the risk to Western Europe would be minimal. Rather, the problem would be a distinctly regional one, with Bulgaria and Macedonia facing a serious loss of gas supplies. Other states in Central and Eastern Europe would not face immediate problems due to existing gas stocks, provided the suspension of transit through Ukraine did not last longer than approximately two months.

One of the great concerns for EU states over the on-going situation in Crimea is their reliance on Russian gas to meet their energy demands, with around 60 per cent of these imports being delivered through pipelines in Ukraine. Jack Sharples and Andy Judge provide a comprehensive assessment of what the impact would be if the transit routes via Ukraine were suspended. They note that while the situation has generally been portrayed as an ‘EU problem’, the risk to Western Europe would be minimal. Rather, the problem would be a distinctly regional one, with Bulgaria and Macedonia facing a serious loss of gas supplies. Other states in Central and Eastern Europe would not face immediate problems due to existing gas stocks, provided the suspension of transit through Ukraine did not last longer than approximately two months.

Russia-Ukrainian gas relations are currently severely strained. The accumulation of debt by Ukraine’s state-owned wholesale gas importer, Naftogaz, and the plans by Gazprom to end its temporary discount on the price at which it exports gas to Ukraine, have resulted in a difficult commercial relationship between Gazprom and Naftogaz. These difficult commercial relations are contextualised by the current tensions about Russian military deployment in Crimea, and there has been considerable speculation in the European and American media about the security of Russian gas supplies to the EU.

Such speculation is generated by concerns over the level of dependency on Russian gas imports faced by several EU member states. Given that almost 60 per cent of Russian gas exports to the EU (not including Finland and the Baltic States) are delivered via Ukraine, any suspension of Russian gas supplies to Ukraine would have a significant effect on European imports of Russian gas. In the context of the current tensions, this short article will address the inherently regional nature of EU energy security and dependency on Russian gas imports via Ukraine. In doing so, we draw on a variety of statistical sources to illustrate and explain the impact of a potential suspension in gas transit via Ukraine on different EU member states.

The role of Russia in EU gas import dependence

The EU’s gas import dependence is the most commonly cited fact used to support claims about EU energy insecurity. This statistic refers to the level of net imports as a share of gross inland consumption. The most recent figure from Eurostat places EU-28 gas dependence at 65.8 per cent of consumption in 2012. With the exception of the Netherlands and the UK, relatively little gas is produced within the borders of the EU, although some Member States such as Denmark, Germany, Italy and Romania have a limited amount of domestic production. As a result, approximately two-thirds of EU gas consumption has to be sourced from outside the EU.

There are three main suppliers of pipeline gas to the EU – Russia, Norway, and Algeria – along with several other suppliers of liquefied gas, most notably Qatar. Russia was the largest single supplier to the EU in 2012, providing 36.5 per cent of EU gas imports. This gave Russian gas a share of 24.2 percent of total EU gas consumption. For comparison, Norway accounted for 34.2 per cent of EU gas imports in 2012, while Algeria and Qatar provided 14.2 per cent and 9.2 per cent respectively.

In light of Gazprom’s increased exports to Europe over the last 12 months, a slight fall in Norwegian exports, the re-direction of liquefied natural gas supplies to the Asia-Pacific market (where prices are higher) and the stability of EU gas consumption, the share of Russian gas in total EU gas consumption in 2013 is likely to have been slightly higher than in 2012. Indeed, reports suggest that Russia’s share of European gas consumption reached 30 per cent in 2013. However, given that Gazprom’s definition of ‘Europe’ includes Turkey (where Russian gas accounts for more than half of total gas consumption), the figure for the EU-28 is likely to be slightly lower.

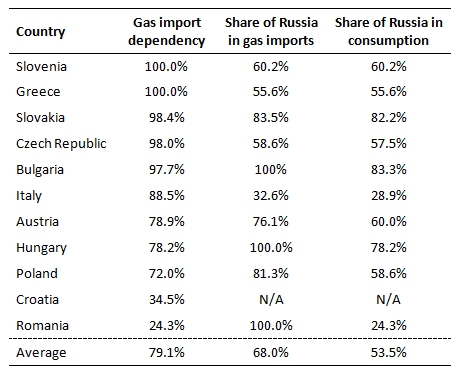

It is important to note that dependence on Russian gas imports is highly differentiated by region and between EU member states. The average level of gas import dependency (79.1 per cent) and the average share of Russia in gas consumption (53.5 per cent) for Central and South-Eastern Europe are both significantly higher than the EU averages (see Table 1). Therefore, these states are more vulnerable to disruptions in Russian gas deliveries to Europe. When examining the importance of gas transit via Ukraine, it is misleading to frame the issue in terms of EU-28 energy security. Rather, it is an issue for a specific geographical part of the EU.

Table 1: Gas import dependency in Central and South-Eastern Europe (2012)

Source: Eurogas

The role of Ukraine as a transit route for the delivery of Russian gas to Europe

Both the EU and Russia are dependent on fixed pipelines for the transit of gas. There are four main routes for Russian gas exports to the EU – direct pipelines to Finland and the Baltic States (collectively referred to hereafter as ‘Baltic exports’), the Nord Stream pipeline under the Baltic Sea to Germany, and transit pipelines via Belarus and Ukraine. Figure 1 below shows the routes of these pipelines.

Figure 1: Map of gas pipelines from Russia to Europe

Note: Map created by Dr A. Judge (CC-BY-SA-3.0)

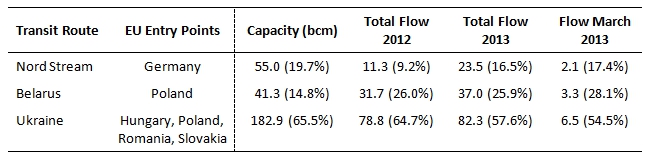

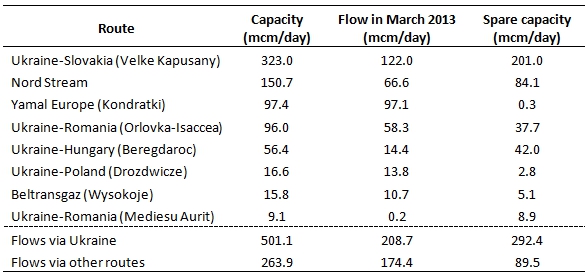

There are, however, some difficulties with calculating exact figures for the level of mutual dependence on these transit routes. The capacity of pipelines is significantly higher than the actual flows of gas supplies, which vary both annually and seasonally depending on demand (see Table 2). In March 2013, for instance, 54.5 per cent of Russia’s non-Baltic gas exports to the EU were transported via Ukraine to Hungary, Poland, Romania and Slovakia. By comparison, 17.4 per cent was exported through the Nord Stream pipeline to Germany, while transit via Belarus to Poland accounted for 28.1 per cent.

Table 2: Capacity and total flow for Nord Stream, Belarus and Ukraine transit routes for Russian gas exports to EU

Note: Figures shown are in billion cubic metres (bcm). Percentages shown for capacity refer to the percentage of total capacity across all three pipelines, while percentages for flow refer to the percentage of total flow across all three pipelines for the date shown (due to rounding percentages may not add up to 100 in all cases). Sources: IEA Gas Trade Flows in Europe; Nord Stream website

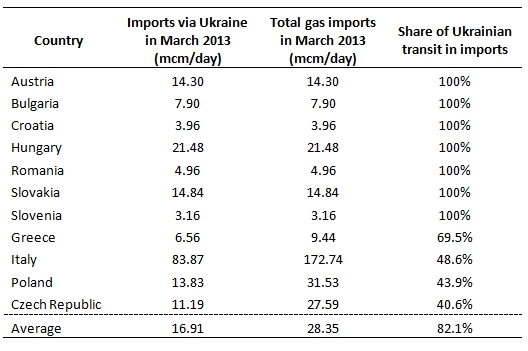

This multiplicity of transit routes has been developed with the explicit purpose of reducing Russia’s dependence on Ukraine as a transit state for its deliveries of gas to Europe, which reached 90 per cent in the early 1990s. The 33 bcm per year capacity Yamal-Europe pipeline (via Belarus) was constructed during the late 1990s, reaching full capacity in 2006. The 55 bcm per year capacity Nord Stream pipeline, direct from Russia to Germany under the Baltic Sea, was launched in two stages in 2011-12. However, the continued importance of Ukrainian gas transit for Italy, the Czech Republic, the Slovak Republic, Austria, Hungary, Slovenia, Croatia, Romania, Bulgaria, Greece, Serbia, Macedonia, and Bosnia-Herzegovina is illustrated by Table 3.

Table 3: Share of Ukrainian transit in Russian gas imports by Central and South-Eastern European countries

Note: Figures are in million cubic metres (mcm) per day. Sources: IEA Gas Trade Flows in Europe

Lessons from the January 2009 gas supply disruption

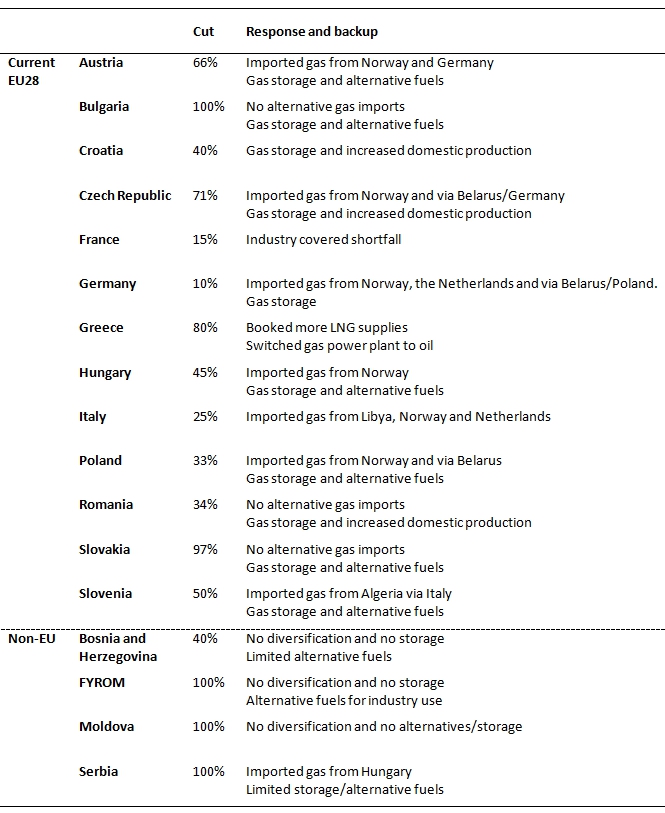

The January 2009 gas dispute between Russia and Ukraine resulted in the most serious disruption of Russian gas supplies to Europe that the region had ever seen. The dispute, its origins, and its resolution have been examined in excellent detail by experts from the Oxford Institute of Energy Studies. For the purpose of this article, one of the most important details of the dispute was the highly differentiated impact the suspension of gas transit via Ukraine had on different European states, both EU members and non-EU members.

The suspension of gas transit via Ukraine illustrated the disproportionate extent to which the states of Central and South-Eastern Europe were dependent on Russian gas supplies and Ukrainian gas transit in a ‘Business as Usual’ scenario. Furthermore, it demonstrated the limited ability of these states to source alternative supplies in an emergency situation. The response from affected EU states in 2009 is shown in Table 4 below.

Table 4: Responses from EU states to gas supply cats during the 2009 Russia-Ukraine dispute

Note: The percentages indicate the level of total gas imports from Russia which were cut for each country. Source: Gas Coordination Group (2009) ‘Member State Situation According to Significance of Impact’, Memo 09/3, 9th January

The potential impact of a suspension of gas transit via Ukraine in spring 2014

Much has changed since 2009. As noted above, the Nord Stream pipeline is now operational. Furthermore, the EU and its Member States have made efforts to increase their readiness to respond to supply disruptions. This includes the development of storage and reverse-flows on some interconnection pipelines between certain Member States. Under EU regulation 994/2010, adopted by the EU following the 2009 disruption, Member States are required to set out national preparatory action and emergency plans to prepare for and respond to supply disruptions should they occur. There remain, however, uncertainties about the EU’s ability to cope with a supply disruption on the scale of January 2009 through the Ukraine route.

For instance, the Nord Stream pipeline now provides significantly more capacity for the transit of gas to non-Baltic Europe. If supplies were to be shut off on the Ukraine route, there is the possibility of rerouting supplies via Nord Stream and Belarus. To assess whether this is possible, we have analysed the daily flows for March of last year (which accounts for seasonal variation) through each of these routes, their total capacity and their related spare capacity, shown in Table 5 below.

Table 5: Capacity and flows for Russian gas exports in March 2013

Note: As shown in the map above, the Nord Stream route runs through the Baltic Sea, while Yamal Europe and Beltransgaz run through Belarus. Sources: IEA Gas Trade Flows in Europe; Nord Stream website

Our analysis indicates that 208.7 mcm/day of Russian gas flowed via Ukraine, out of total Russian gas exports to (non-Baltic) Europe of 383.1 mcm/day. Therefore, transit via Ukraine accounted for 54.5 per cent of Russia’s gas exports to (non-Baltic) Europe in March 2013. There existed 89.5 mcm/day of spare capacity on the non-Ukrainian routes, leaving 119.2 mcm/day (equivalent to 43.5 bcm per year) that would be non-deliverable in the case of a shutdown of Ukrainian transit. While figures for March 2014 will differ somewhat, this gives a clear indication that a supply shortfall due to a disruption on the Ukraine route could not be entirely compensated for through alternative transit routes for Russian gas.

There are other elements that would come into play in the event of a supply disruption, such as alternative sources of gas supplies, particularly from Norway, Algeria and liquefied natural gas shipments. In recent days the Speaker of the United States’ House of Representatives, John Boehner, lent his support to a request from the Czech Republic, Hungary, Poland and Slovakia to accelerate plans to export US shale gas to Europe. While this may eventually contribute to greater diversification in the EU, it will have no impact on any potential supply disruption over the coming months.

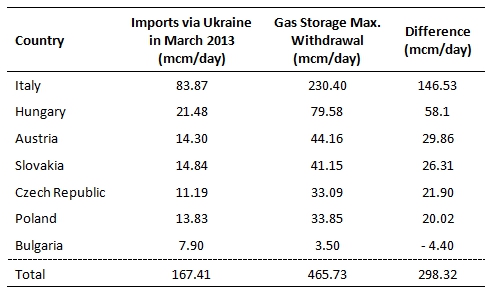

Gas storage will also be a key issue in the event of a short-term supply disruption. Table 6 and Table 7 below illustrate the current gas storage capacities and gas stocks of the states of Central and South Eastern Europe in relation to their imports of Russian gas via Ukraine.

Table 6: Gas storage withdrawal capabilities in selected Central and South Eastern European countries in relation to imports via Ukraine (March 2013 levels)

Note: The table illustrates the difference between daily gas imports via Ukraine in each country and the maximum potential gas that can be withdrawn per day from existing storage. Sources: IEA Gas Trade Flows in Europe; Nord Stream website.

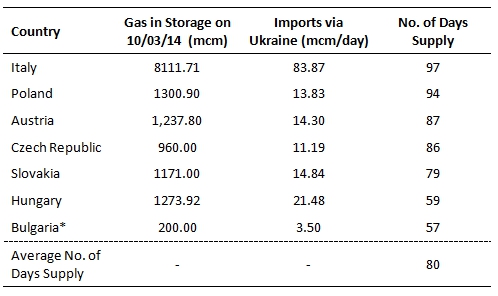

Table 7: Number of days the supply of gas in storage would last if compensating for imports via Ukraine in selected Central and South Eastern European countries

Note: The table shows how long the gas in storage in each country would last if it were withdrawn to compensate for the loss of gas imports via Ukraine. For Bulgaria the figure of 3.5 mcm/day is not sufficient to compensate for the amount of gas that is imported via Ukraine. This means there would be a shortfall, but the number of days of supply shown nevertheless represents the length of time that Bulgaria could continue to withdraw gas from its storage supply at the maximum rate of 3.5 mcm/day. Sources: Gas Infrastructure Europe.

Gas-producing Romania has ample gas storage facilities. Data on Romanian gas storage was not provided to Gas Infrastructure Europe, but the Romanian energy expert, Dr Radu Dudau estimates that Romania has approximately 1000 mcm in storage – more than enough to replace imports via Ukraine. On the 6th of March Reuters reported an emergency meeting of the EU Gas Coordination Group, at which the Romanian representative declined to give detailed information about Romanian gas stocks, noting only that “Romania said in the event of a fall in temperature, it could not help neighbouring Bulgaria, one of the nations most dependent on Russian gas”. During the January 2009 crisis Romania was able to step up its domestic gas production and draw on gas storage stocks. Despite the lack of explicit data on Romanian gas storage, we expect that in the event of another suspension of gas transit via Ukraine, the Romanian response would be similar.

As can be seen from the two tables above, Bulgaria is the only country for whom withdrawals from gas storage facilities would not be sufficient to replace imports via Ukraine. The Bulgarian cross-border connection with Greece cannot be reversed to take advantage of increased Greek liquefied natural gas imports. Turkey would be able to make up only part of its shortfall by using spare capacity in the Blue Stream pipeline, and so would be unable to transit extra Russian gas supplies to Greece or to reverse the cross-border pipeline connection with Bulgaria. Macedonia relies completely on transit via Bulgaria for access to its Russian gas supplies. If Bulgaria faces a complete lack of import supplies, so too will Macedonia. Therefore, Bulgaria and Macedonia would face significant shortfalls in their gas imports.

Although Greece has no gas storage facilities, in March 2013, Greek had 11.4 mcm/day of spare liquefied natural gas import capacity, compared to 6.56 mcm/day of gas imports via Ukraine. Serbia receives its Russian gas imports via Hungary. In March 2013, these amounted to 4.15 mcm/day. Serbia has its own gas storage facility (Banatski Dvor), which has a capacity of 450 mcm and a maximum daily output of 5 mcm. It is not known how much gas Serbia has in storage, but gas withdrawals from Hungarian storage would be available for export to Serbia, if Serbian gas stocks proved insufficient.

On this basis, Bulgaria, and Macedonia would face a serious loss of gas supplies in the event of a suspension of gas transit via Ukraine. The other states in the region would be able to manage the situation, as long as it did not last for more than approximately two months. Austria, Czech Republic, Hungary, Italy, Poland, and Slovakia currently have sufficient gas storage to withstand 2-3 months of disruption to their gas imports via Ukraine, while Serbia could draw on Hungarian gas stocks. Slovenia and Croatia could draw upon Italian, Austrian, and Hungarian gas stocks.

Gas flow from Russia to Europe via Ukraine in March 2013 was 208 mcm/day. Of these flows, 167.41 were delivered to Austria, Bulgaria, the Czech Republic, Hungary, Italy, Poland, and Slovakia. A further 4.95 mcm/day was delivered to Romania, 4.15 mcm/day to Serbia, 3.16 mcm/day to Slovenia, 3.96 mcm/day to Croatia, and 0.38 mcm/day to Macedonia. The total flow to Central and South-Eastern Europe was 184 mcm/day, meaning that just 24 mcm/day was delivered via Ukraine to Western Europe in March 2013. If similar flows were recorded in March 2014, the spare capacity of Nord Stream (84 mcm/day) would be more than sufficient to meet the additional needs of those Western European states that import Russian gas via Ukraine.

Conclusions

Russia-Ukraine gas relations are currently contextualised by tense political relations, and characterised by indebtedness and politically negotiated gas prices. With Naftogaz struggling to pay its debts to Gazprom and the discount on Russian gas supplies due to expire on the 1st of April, the current situation is every bit as serious as that, which preceded the January 2009 dispute. The one redeeming feature is that at least Gazprom and Naftogaz have existing gas supply and gas transit contracts that are not on the verge of expiring.

Whilst we are not predicting a repeat of the January 2009 suspension of gas supplies to Ukraine, the possibility remains. The suspension of Russian gas supplies to Ukraine would almost certainly result in the suspension of gas transit via Ukraine, as Naftogaz draws on its gas storage in the west of the country and reverses the flow of its pipelines to carry that gas back across Ukraine to consumers in the East of the country. If such a flow reversal does not take place, the siphoning of gas, as happened in January 2009, also cannot be ruled out.

In the event of a suspension of gas transit via Ukraine, we find that the states of Central, Southern, and South-Eastern Europe would be disproportionately affected. The disruption of gas supplies to Western Europe would be small, and the spare capacity of Nord Stream could easily be used to make up the shortfall. Indeed, Nord Stream’s spare capacity could also be used to redirect flows to Central Europe, although much depends on the domestic pipeline capacities of those states and their ability to reverse the flows of their domestic pipelines.

Greece and Italy have the option of utilising their spare liquefied natural gas import capacity. For the majority of those states that do not have access to alternative supplies, the issue of gas storage is crucial. Having examined current storage capacities and gas stocks, we find that the majority of states in the region are currently holding sufficient supplies to cope with a disruption of up to two months. Only Bulgaria and Macedonia would be unable to gain access to sufficient supplies from gas storage.

While the suspension of gas transit via Ukraine would be a significant event, it is not inevitable at this stage. If such a suspension does occur, most EU Member States that would be affected are well prepared and will be able to cope. The vulnerability of Bulgaria, and Macedonia should mark them out as a short-term priority for EU assistance in the event of a disruption. In the longer term, there clearly needs to be further development of cross-border interconnections and gas storage facilities in this region.

A longer version of this article is available at the European Geopolitical Forum

Please read our comments policy before commenting.

Note: This article gives the views of the authors, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/1gnh8IG

_________________________________

About the authors

Jack Sharples – European University of St Petersburg

Jack Sharples is a lecturer in Energy Politics at the European University of St. Petersburg. He recently defended his PhD on Russian Gas Exports at the University of Glasgow and also writes the monthly ‘Gazprom Monitor’ report for the European Geopolitical Forum. Contact: jsharples@eu.spb.ru / http://eu-spb.academia.edu/JackSharples

Andy Judge – University of Strathclyde

Andy Judge is a researcher at the School of Government and Public Policy at the University of Strathclyde, Glasgow. He recently defended his PhD on Securitisation and European Natural Gas Policy and is currently working on research into the EU’s crisis response mechanisms in the event of gas supply disruptions. Contact: a.judge@strath.ac.uk / http://independent.academia.edu/AndrewJudge

2 Comments