Since Britain’s EU referendum, UK inflation has risen faster than that of the Eurozone. Price rises have varied across sectors, but as Josh De Lyon, Swati Dhingra, and Stephen Machin show, the rise in the growth rate of food prices has been particularly pronounced. As a result, real wage growth in the UK has again turned negative.

Since Britain’s EU referendum, UK inflation has risen faster than that of the Eurozone. Price rises have varied across sectors, but as Josh De Lyon, Swati Dhingra, and Stephen Machin show, the rise in the growth rate of food prices has been particularly pronounced. As a result, real wage growth in the UK has again turned negative.

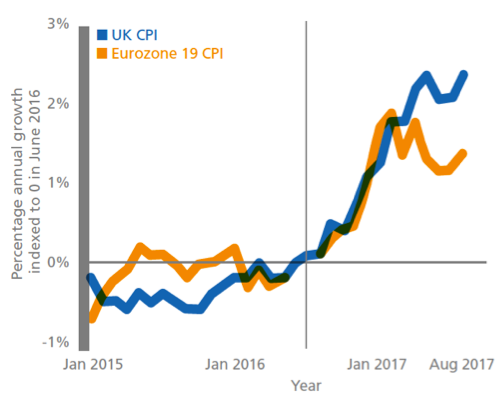

The pattern of significantly higher price inflation is shown in Figure 1. This plots the annual consumer price index (CPI) before and after the Brexit vote, comparing the UK with what has happened in the 19 Eurozone countries. To a large extent, the CPI growth rates of both the UK and Eurozone move together, with both being driven by worldwide commodity prices.

Figure 1: Consumer price inflation trends pre- and post-Brexit vote

Note: See the accompanying Centre for Economic Performance report for more details.

The index is a cumulated annual index and so only shows the full effect of the referendum from May 2017, when it is no longer diluted by pre-referendum data. Taking this into account, the spike observed shortly after the referendum is significant. It is likely to have been driven by the devaluation of sterling, which occurred immediately after the referendum result.

The full effect is indicated by the divergence of CPI annual growth rates between the UK and the Eurozone a year after the referendum. This divergence in consumer price inflation partly reverses the convergence in price changes that occurred in the single market, when price dispersion of tradable goods started to converge to levels seen across US cities by the mid-1990s (Rogers, 2001).

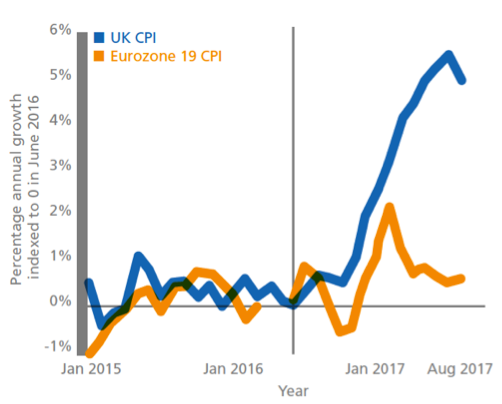

For certain commodity groups, the increase in the CPI growth rate has been more pronounced. Figure 2 presents the annual growth rate of CPI where the sample of goods and services is restricted to food. There is a distinct and substantial rise in the rate of CPI food inflation for the UK relative to the Eurozone.

Figure 2: Food consumer price inflation trends pre- and post-Brexit vote

Note: See the accompanying Centre for Economic Performance report for more details.

The divergence that immediately followed the referendum is quite a bit larger than that observed for all goods in Figure 1, and becomes larger when amplified over time. This has important implications for how the vote has affected the purchasing power of different income groups. Low-income households spend a higher proportion of their income on food than rich households.

Credit: CC0 Public Domain

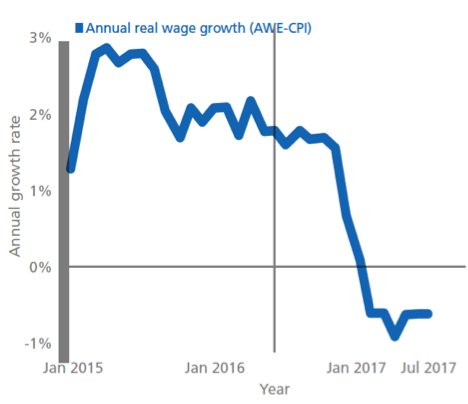

The UK experienced several years of real wage falls following the financial crisis of 2007/08, but in the period before the referendum, real wage growth in the UK had become positive (see Blanchflower and Machin, 2016; Blanchflower et al, 2017). This arose because of very low inflation, not because of any strength in nominal wage growth (which seems to have become stuck at a norm of 2% per year since the start of the decade).

But the increase in prices following the Brexit vote coupled with no significant rise in nominal wages has again caused real wage growth to become negative. This is shown in Figure 3, which indicates that the real wages squeeze is back because of the post-referendum price increases.

Figure 3: Real wage trends pre- and post-Brexit vote

Note: See the accompanying Centre for Economic Performance report for more details.

By the end of our data period, the price increases following the referendum have now fully appeared in the annual index. It seems that the Brexit vote has caused a one-off rise in prices, and that the annual growth rate of prices will begin to fall out of the index once it no longer includes the months that immediately followed the referendum.

Overall, this research points to a significant rise in prices occurring after the EU referendum. Future work that builds on these initial findings will quantify the role of the devaluation of sterling by focusing closely on price changes for imported goods and services.

Please read our comments policy before commenting.

Note: This article gives the views of the authors, not the position of EUROPP – European Politics and Policy or the London School of Economics. The article first appeared at our sister site, LSE Brexit, and is based on the LSE’s Centre for Economic Performance report Brexit: the impact on prices.

_________________________________

Josh De Lyon – CEP

Josh De Lyon is a research assistant in CEP’s trade programme.

Swati Dhingra – CEP

Swati Dhingra is Assistant Professor of Economics at LSE and a research associate in CEP’s trade programme.

Stephen Machin – CEP

Stephen Machin is Professor of Economics at LSE and Director of CEP.

I understand all the ‘reasons’ such as commodity prices but yet I fail to understand why some prices have risen. I live in Cornwall and as an example a simple pack of local ( note) butter that was £1.38 is now £1.85 (at best) and even higher. The manufacturing uses ALL local produced ingredients , has no imported additions yet blossoms with price rises along with many other items of food.I can only assume that profiteering is being applied under the guise of Brexit fears. There seem no other explanation.

Prices can rise even for local produce in this situation. For instance, imagine that we buy 50% of our butter from abroad and the other 50% is made in the UK. If the price for a pack of butter from abroad doubles, then the price for our British butter doesn’t just stay the same because there’s now a lot more demand for British (cheaper) butter as nobody wants to buy the (expensive) imported stuff. That pushes up the price for the British butter as well and we end up with expensive imported butter and more expensive British butter because of the knock-on effect (even if it’s produced entirely locally).

Then there’s the supply chain effect. A farm in the UK has to buy machinery and we import a lot of it from countries like Germany. If machinery prices go up then the costs for UK farmers also go up and that gets passed on to consumers. What’s true of machinery is true of other farm supplies like animal feed and so on.

In short, once prices start to go up for imports, it can spillover into prices also going up for UK products as well.

A pretty daft argument until we have left the EU. Once we have left we can source food from any corner of the globe where prices aren’t artificially held high. Food at the grocers will crash in price to the benefit of all consumers benefiting the poorest members of society the most as that is where the lions share of their expenditure goes

It’s not an “argument” it’s a statement of what’s actually happened since June last year. Most people from my experience couldn’t care less about arguing over Brexit all day, what they care about is that their wages are being squeezed today (not tomorrow, not years from now, today) and it’s undermining their living standards. Brexit is already making us all worse off and for what? Just to win some nonsense argument about sovereignty and control that only a tiny percentage of people care about.

But while we’re discussing the long-term, your solution isn’t a solution at all. Unilaterally removing all tariffs on agricultural produce will decimate our own agricultural sector who will no longer be able to compete with cheap imports flooding the market. That’s the whole point in having tariffs in the first place.

The current government talks a lot about ” free trade” and an ” open Britain ” but it’s is for neither. No UK goverment , never mind a Tory one, is going to decimate British farming by having free trade in agricultural products. Australia, Brazil , New Zealand would love free trade in agriculture, but they won’t get.

The so called ability of the UK to open its trade and negoiate better ” trade deals” than the EU is delusional. Germany already does massively more trade with China than us, so the EU is not holding them or us back. What do we have to offer China that would make them give us a better deal than the much larger EU? If we were a small specialist economy, then our ” own trade deals ” might make sense. But not only is our economy more diverse but our biggest export is services. There is no ” trade deal” in the world, including NAFTA, that gives the kind of access for service exports that we currently enjoy within the Single Market.

Please excuse my dyslexic spelling.

We knew we would have to wait for at least two years for the benefits of leaving. No gain without the short term pain. The only people moaning are the opportunists in the Labour party that would argue black is white to cause unrest. There is no unrest amongst those that voted to leave. We can’t negotiate trade deals while we without adding EU imposed tariffs so as I said the article is pointless as are your comments

The Brexit vote tanked the pound, it’s pushed real wages down significantly, we’re all poorer as a result, the worst off in the country are having their living standards squeezed, and all you can offer to justify that is to tell people to shut up and ignore it in the hope some pie in the sky hopes about Brexit (which are rejected by 99% of economists) are going to make us all better off in the long run. That’s completely laughable.

People are worse off now, they’re struggling today, why on earth shouldn’t they complain about that? What exactly is it about putting trade barriers between us and our largest export market and scrapping the roughly 50 free trade deals the EU currently has with other countries around the world that you think is going to make us better off in the long run?

I completely understand that people like you don’t actually care about the lives of British citizens – you’re interested in winning an argument about Brexit, your own little pet obsession, and would happily throw the entire population under a bus if that’s what it takes. But the rest of us who actually care about people’s lives aren’t going to stand for it. The figures in this article are damning and nobody should be brushing them under the carpet.

More strawman arguments from Burns !

No Leaver is proposing

“putting trade barriers between us and our largest export market and scrapping the roughly 50 free trade deals the EU currently has with other countries ”

It is precisely because we DO care about the lives of British citizens – our children and grandchildren – that we want a free-er and wealthier future unshackled from an undemocratic and costly bureaucracy..

Those that like the EU so much are free to move there …. well at least until March 2019.

Leaving the EU without a deal means, by definition, that we’ll have extra trade barriers between ourselves and those states that participate in the single market. Leaving the EU with no deal means, by definition, that we’ll be leaving the 50 odd free trade agreements the EU has with other countries. If you’re calling for leaving the EU with no deal then that’s what you’re arguing for. Take ownership of it for once instead of constructing absurd arguments of the kind you’ve presented here.

“The Brexit vote tanked the pound”

Typical Remain exaggeration …..

Depending on the start date, GBP has fallen about 11% v. EUR and 9% v. USD.

Compared to past currency moves, that is hardly “tanked”.

Furthermore:

i) the B of E’s interest rate cut in August 2016 added up to 3% of the decline – before some recovery.

ii) Imports account for a little over 10% of our GDP – so the impact on a falling Pound should not have the exaggerated impact in the butter example above.

Lastly, what is the point of the exaggerated assertion “99% economists reject / agree ..”?

Is that from the same school as the old cat food advert “99% of cats prefer Whiskers”?