Almost no economist or financial commentator saw the 2008 crisis coming: next to no one anticipated in early 2009 that recovery would prove so difficult and slow: nobody foresaw that seven years after the crisis, interest rates today would be close to zero in all major advanced economies.

I became chair of the UK Financial Services Authority in September 2008, five days after Lehman Brothers collapsed, and from 2009 to 2013 I played a major role in the redesign of global financial regulation, chairing a leading policy committee of regulators and central bankers. I think we did a good job, and that the higher capital and liquidity standards we imposed will make the global financial system far more resilient. But increasingly I became convinced that our reforms failed to address the fundamentals of why 2008 occurred and why recovery has proved so difficult, and that without far more radical policy reforms we will be stuck for many years in unnecessarily slow growth, and vulnerable to future financial and economic crises.

The fundamental problem is that the private banking system left to itself creates “too much of the wrong sort of debt”. In 1950, private credit to GDP in the advanced economies stood at 50 percent: by 2007 it had reached 170 percent. And contrary to what economics and finance textbooks assert, most of this debt did not support business capital investment: instead it primarily funded the purchase of already existing real estate, with increasing credit supply producing asset price rises which in turn stimulated increased credit supply and demand. Every year on average, private credit grew at around 10 to 15 percent per annum, while nominal income grew at only around five percent. And it seemed at the time that we needed that rapid credit growth in order to ensure sufficient demand to support real growth in line with potential and inflation in line with target.

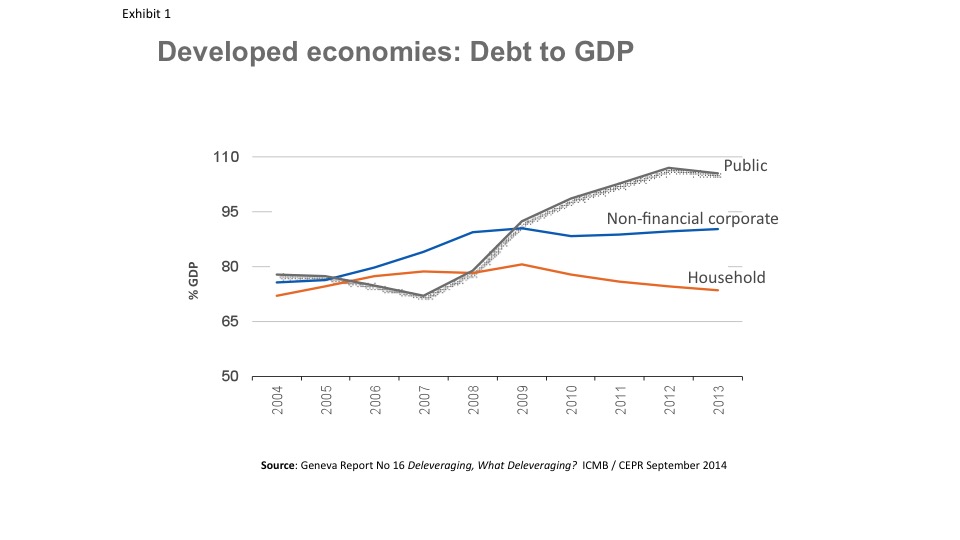

But if we really do need such rapid credit growth, we have an economic model which is bound to end in crisis. And bound in turn to leave us struggling with a sustained post-crisis recession in which debt doesn’t actually go away, but simply shifts around the economy. In the developed economies, debt has moved from private to public sectors, as private deleveraging has been offset by large public deficits, but total debt to GDP has continued to rise ( Exhibit 1 ):

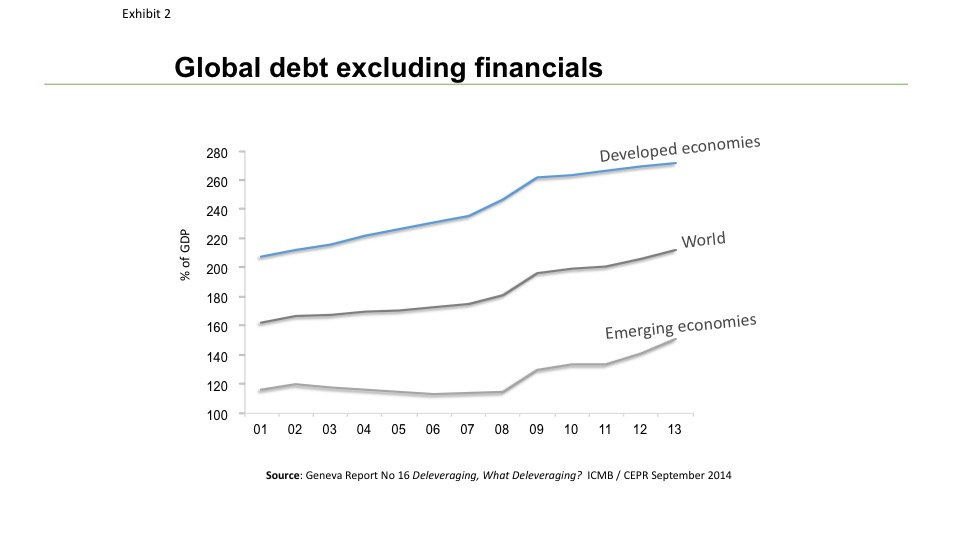

And across the world it has shifted from developed to developing countries, with , for instance, China unleashing in 2009 an enormous credit fuelled investment boom to offset the export demand it lost when US households began to pay down their debts. ( Exhibit 2 ).

The result is a sustained malaise in which all our traditional policy levers seem blocked – with fiscal policy restrained by fears about public debt sustainability, and with ultra-loose monetary policy more effective in driving asset bubbles than in producing investment in the real economy, and only ultimately effective if it restimulates the very growth of private credit which first got us into the debt overhang trap.

Two questions for public policy follow: the first is how to manage our economies in future so that growth is not so dependent on rising debt. I argue in Between Debt and the Devil that we will only succeed in that if we address the fundamental causes of credit intensive growth – the role of real estate in our economies, rising inequality, and global imbalances – as well as introducing radically tighter bank regulations, with banks leveraged more like 5 to 1 than the 20 to 1 we have in the past allowed.

The second is how to get out of the mess in which past policy errors and rising leverage have left us. Here I suggest we must be willing to break a taboo, and accept, as Milton Friedman among other economists proposed, that in some circumstances the most effective and least risky way to stimulate nominal demand is to run somewhat larger fiscal deficits permanently financed with central bank money creation.

There are no technical reasons why this is impossible, nor why it will result in excessive inflation: but there are great political dangers that once politicians realise that money finance is possible, they will use it continually and to excess. But those political dangers can be overcome, by locating authority to approve money finance within a central bank pursuing a clearly defined inflation target. By refusing to consider this probability, we have made the consequences of 2008 still more adverse than they needed to be.

♣♣♣

Notes:

- This post gives the views of the author, and not the position of LSE Business Review or the London School of Economics.

- Featured image credit: liz west CC-BY-2.0

Adair Turner was Chair of the UK Financial Services Authority from 2008 -2013 and chair of the major policy committee of the international Financial Stability Board from 2009-13 . He is currently Chair of the Institute for New Economic Thinking and author of Between Debt and the Devil – Money, Credit and Fixing Global Finance ( Princeton 2015).

Adair Turner was Chair of the UK Financial Services Authority from 2008 -2013 and chair of the major policy committee of the international Financial Stability Board from 2009-13 . He is currently Chair of the Institute for New Economic Thinking and author of Between Debt and the Devil – Money, Credit and Fixing Global Finance ( Princeton 2015).