Quantitative easing is called ‘unconventional monetary policy’, but monetary policy could get much more ‘unconventional’. Things like ‘helicopter money’, abolishing currency and negative nominal interest rates have entered the public policy debate. This column reports the views of leading experts on the future role of unconventional monetary policy, and what might be called ‘unconventional unconventional monetary policies’. Opinions are divided. There is a healthy dose of scepticism on the effectiveness of current and future policies, but also many respondents express urgency that central banks should have more policy tools to affect inflation and real activity when the need arises. Ultimately, the experts’ hesitations match those of central banks.

Background

The Bank of England’s Monetary Policy Committee (MPC) last changed interest rates in March 2009 when the official interest rate was lowered to 0.5% and has stayed there since then (which suggests that this may be the perceived effective lower bound on nominal interest rates). At the same time, the Bank of England began to make purchases of financial assets direct from the non-bank financial sector.

The MPC began with £200 billion of asset purchases, mostly UK government debt, between March 2009 and November 2009. It then increased the stock of asset purchases to £375 billion in three increments (£75 billion in October 2011; £50 billion in February 2012; and £50 billion in July 2012). While there have been no further purchases of assets for over three and a half years, the returns and proceeds on maturing bonds have been reinvested, which means that the outstanding portfolio of purchased assets is £375 billion.

This form of monetary policy, know as quantitative easing (QE), was unconventional because it consisted of large purchases of government bonds of long maturities funded by interest-paying reserves. Textbook conventional open market operations instead consist of purchases of short-term bonds in small quantities, paid for by currency or non-interest paying reserves. Moreover, QE purchases of long-maturity assets are executed for reasons other than the implementation of a decision to change the (short-term) policy rate.

Similar unconventional policies have been adopted by other central banks at times over the last seven years, although other central banks went further by also buying many other non-government issued securities and/or lending against a broad set of collateral for long periods of time. Such forms of unconventional monetary policy have become so common that they have been called ‘conventional unconventional monetary policy’.

There has been active research on the effects of QE policies. Most work finds that QE increases the prices of the assets that are bought, lowers long-term interest rates, and decreases expectations of future short-term interest rates. The effect of these policies on inflation and real outcomes are more disputed, as are their effects on financial stability. The classic references that started the literature are Gagnon et al. (2011) and Krishnamurthy and Vissing-Jorgensen (2011) for the US and Joyce and Tong (2012) for the UK, while Rogers et al. (2014) provide a review across countries.

Unconventional monetary policy in ‘normal’ times

There is disagreement about the current strength (or weakness) of economic conditions in the UK and elsewhere, and therefore on the desirability of further monetary stimulus. The first question in the Centre for Macroeconomics (CFM) survey asked the experts to set aside their views as to whether the current state of the economy warrants the use of further unconventional policies, and asked them to consider whether these unconventional policies should become part of the conventional tools of monetary policy under ‘normal’ economic conditions.

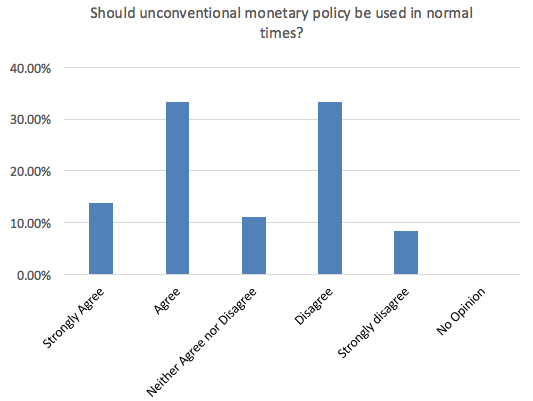

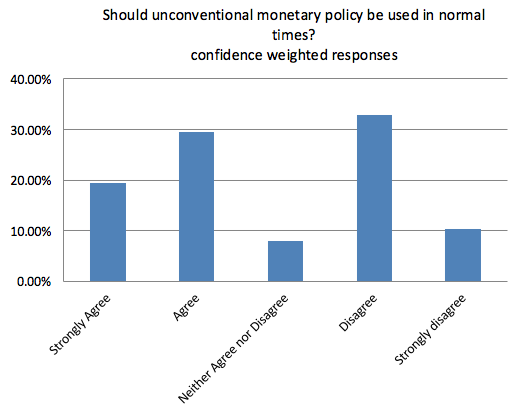

QUESTION 1: Do you agree that central banks should continue to use the unconventional tools of monetary policy deployed in response to the global financial crisis as part of conventional monetary policy under normal economic conditions?

Thirty-six of the panel answered this question, and they are close to being evenly divided in their assessments: 47% agree, while 41% disagree, with the remainder in between. There is also a match at the extremes, with only the slightest advantage to those that agree strongly, 14%, versus those that disagree strongly, 8%.

On the side of those that are suspicious of unconventional policies in normal times, four arguments stand out. The first is that using conventional interest rate setting is more effective, and less prone to error. As Sir Charles Bean (London School of Economics, LSE) puts it, ‘the conventional short-term policy rate should be the preferred monetary policy instrument once the policy rate is clear of its floor (i.e. in ‘normal’ times). That is because there is less uncertainty around the impact on the economy of variations in the policy rate than there is surrounding the impact of asset purchases.’

Panicos Demetriades (Leicester) agrees: ‘Unconventional monetary policies are intended to be used when conventional policy has reached its limits, when interest rates have reached the zero lower bound and negative interest rates cannot be relied upon. They have too many side effects, some of which are not well understood, to become part of conventional monetary policy.’

The second argument is that unconventional policies don’t work well. As Michael Wickens (Cardiff Business School and University of York) states, ‘Even in the current abnormal conditions, unconventional monetary policy has proved ineffective in stimulating private credit expansion.’

A third argument worries that using unconventional policies makes it hard to be transparent and to pursue clear rules. Morten Ravn (University College London) says ‘Using also unconventional policies would be a return to the fine-tuning policies of the past which was no big success to put it mildly. Moreover, it would make central bank communication very challenging and most likely be costly in terms of reputation.’

The fourth argument notes that unconventional policies are quasi-fiscal operations that can lead to losses and danger to the central bank’s independence, as Martin Ellison (Oxford) notes: ‘QE exposes the central bank to making capital losses and gains that ultimately have to be underwritten by the Treasury.’

On the side of those that are in favour of using unconventional policies in normal times, Ray Barrell (Brunel) argues that: ‘Monetary policy has normally operated at the short end of the yield curve, whilst the long end is probably more important for both wealth effects and investment decisions… Central banks should look at the situation they find themselves in and operate where it is most appropriate.’ Sir Christopher Pissarides (LSE) agrees: ‘Monetary policy is not easy and the more tools that the central bank uses the more effective its policy will be’.

Ricardo Reis (LSE) argues that these policies are really not all that unconventional: ‘The central bank’s balance sheet has ‘always’ been a policy tool, especially in open economies where central banks hold foreign reserves… The use of QE and other unconventional tools in the recent past has just made us study these issues better, learn more about their effects, and so become more confident about using them in the present and in the future.’

Helicopter money and other ‘unconventional unconventional policies’

Some economists have expressed concerns that there are economic conditions under which existing tools, including unconventional monetary policy tools, are not sufficient to achieve central bank objectives. In fact, some have argued that current conditions warrant more innovative tools being introduced. These ‘unconventional unconventional policies’ include the financing of public spending (or tax cuts) through printing money – the idea that was called ‘helicopter money’ by Milton Friedman. These policies also include abolishing currency and setting substantially negative nominal interest rates.

Others feel that even if current tools may be enough for now, it is necessary to undertake a more radical rethink of the tools of monetary policy to ensure that the central bank is ready to deal with future crises as they arise.

Against further expansion of the tools of monetary policy, some argue that QE, if continued and expanded, is enough. Further increasing the size of the central bank balance sheet or making this set of tools more permanent leaves enough room for the Bank of England to intervene further. Moreover, they argue that the changes to the current monetary policy arrangements necessitated by the adoption of these tools are too uncertain and/or too costly (for example, giving up hard-earned monetary independence and credibility, or radically changing the payment systems in society).

The second question in the CFM survey asked the experts whether they believe that the central bank toolkit needs further new tools to become potential instruments of monetary policy (again ignoring whether they believe current conditions necessitate such instruments). In the context of this question, operationalising the tools means that the central bank takes whatever steps are necessary to add the instrument to their menu of possible policy options, even if no immediate use of the policies is made. New policies whose first objective is financial stability were not be considered in this question.

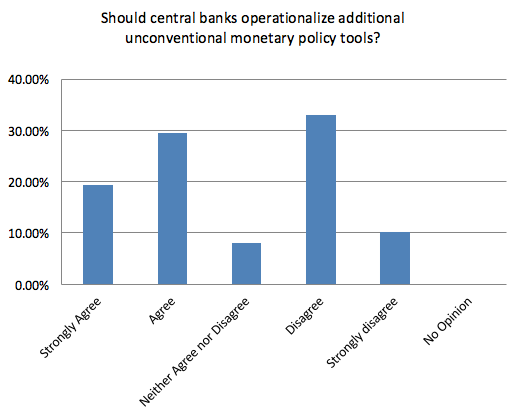

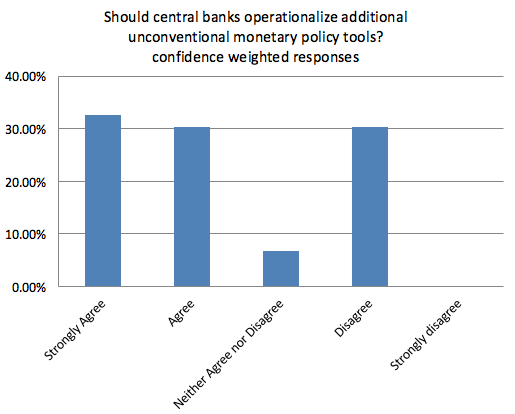

Question 2: Do you agree that central banks should operationalise the use of these alternative tools of unconventional monetary policy for use either in the near term, or in the future, as economic conditions warrant?

The experts are weakly in favour of these alternatives, as slightly more than half agree, with only 36% disagreeing. But it is those who disagree that are more vocal in their opinions, justifying them at greater length.

Ethan Ilzetzki (LSE) thinks that these tools, and especially helicopter money, are clearly fiscal operations: ‘I support the use of fiscal policy as a countercyclical tool, but do believe this should remain within the remit of the Treasury. Helicopter money may be a way to exploit the Bank of England’s independence to circumvent the political process, but I think this would be unwise.’ Kate Barker (Credit Suisse) makes a similar point.

David Miles (Imperial College) sees helicopter money as being likely to have no effect: ‘If the question is asking about helicopter drops I do not agree that they are likely to be a useful tool… Distributing newly printed bank notes in exchange for government debt would, in fact, almost immediately be turned back into reserves. If reserves pay interest – as they do now and as I think they should – then ‘printing money’ is just financing government spending by the government borrowing at Bank Rate, something it can do anyway by issuing Treasury Bills.’

More generally, Wouter Den Haan (LSE) is sceptical that it is better to have more instruments: ‘It is not clear to me that achieving central banks’ objectives will become more manageable with these quite revolutionary instruments. In fact, steering a ship in a storm may become more difficult when the captain has many controls and it becomes more difficult for the ship’s sailors and other ships to understand what is going to happen.’

Michael McMahon (Warwick) concludes that while these alternative policies should be studied, they are not ready to be implemented: ‘It is clear that central banks should be thinking about the practicalities of a number of alternative tools for possible future use, but I think I fall short of fully advocating their operationalisation at the moment.’

Of those that agree that central banks should operationalise alternative tools, Nicholas Oulton (LSE) thinks that these policies are already been in place, just in disguise: ‘In the UK case we have in effect already operationalised the use of helicopter money since the period of active QE coincided with a large budget deficit.’

Simon Wren Lewis (Oxford) agrees that the policies are fiscal, but sees this as a virtue: ‘One of the undesirable side effects of central bank independence is that governments are no longer able to undertake a money financed fiscal stimulus in a deep recession. Governments and central banks need to put that right by one means or another.’

Finally, Angus Armstrong (National Institute of Economic and Social Research) provides a precautionary defence of these policies: ‘From a risk management perspective it would be prudent to operationalise alternative tools at least for the near term. In fact, one could regard it as negligent if alternative tools were not operationalised given the extraordinary economic conditions and failures in forecasting.’

♣♣♣

Notes:

- This post appeared originally on Vox and is based on the Centre for Macroeconomics Survey The future role of (un)conventional unconventional monetary policy.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Roman Soto CC-BY-2.0

- Before commenting, please read our Comment Policy.

Wouter Den Haan is Professor of Economics at LSE and Co-Director of the Centre for Macroeconomics. HIs main research interests are in macroeconomics, the role of frictions in financial and labour markets for business cycles, business cycle models with heterogeneous agents and computational economics. He holds a PhD in Economics from Carnegie Mellon University.

Wouter Den Haan is Professor of Economics at LSE and Co-Director of the Centre for Macroeconomics. HIs main research interests are in macroeconomics, the role of frictions in financial and labour markets for business cycles, business cycle models with heterogeneous agents and computational economics. He holds a PhD in Economics from Carnegie Mellon University.

Martin Ellison is a British economist. He is Professor of economics at the University of Oxford and a Fellow of Nuffield College. He gained his PhD in economics in 2001 from the European University Institute in Florence. Ellison has worked as a consultant for the Bank of England and as a Professor at the University of Warwick before his current affiliation at the University of Oxford. He is specializing in macroeconomics; his PhD thesis was titled “Money Matters: Four Essays on Monetary Economics”. His main research interest is monetary policy and he is editing several journals in the field of economics.

Martin Ellison is a British economist. He is Professor of economics at the University of Oxford and a Fellow of Nuffield College. He gained his PhD in economics in 2001 from the European University Institute in Florence. Ellison has worked as a consultant for the Bank of England and as a Professor at the University of Warwick before his current affiliation at the University of Oxford. He is specializing in macroeconomics; his PhD thesis was titled “Money Matters: Four Essays on Monetary Economics”. His main research interest is monetary policy and he is editing several journals in the field of economics.

Ethan Ilzetzki is Assistant Professor of Economics at LSE. He is an Associate at the Centre for Macroeconomics and the Centre for Economic Performance. HIs research interests are in macroeconomics, international finance and fiscal policy. He holds a PhD in Economics from the University of Maryland.

Michael McMahon is Associate Professor of Economics at Warwick University. He is also a a Research Associate with the Centre for Macroeconomics (CFM), Research Affiliate with the Centre for Economic Policy Research (CEPR) and the Centre for Applied Macroeconomic Analysis (CAMA, ANU), International Consultant Economist at the IMF’s Singapore Training Institute and a Visiting Scholar at the Bank of England. He holds a PhD in Economics from LSE. Dr. McMahon’s research interests are macroeconomics of business cycles; monetary economics; inventories and applied econometrics.

Michael McMahon is Associate Professor of Economics at Warwick University. He is also a a Research Associate with the Centre for Macroeconomics (CFM), Research Affiliate with the Centre for Economic Policy Research (CEPR) and the Centre for Applied Macroeconomic Analysis (CAMA, ANU), International Consultant Economist at the IMF’s Singapore Training Institute and a Visiting Scholar at the Bank of England. He holds a PhD in Economics from LSE. Dr. McMahon’s research interests are macroeconomics of business cycles; monetary economics; inventories and applied econometrics.

Ricardo Reis is Professor of Economics at LSE, on leave from Columbia University. He received his PhD in Economics from Harvard University in 2004. He has published extensively and has had a number of editorial positions in leading academic journals. He is a Research Associate at CFM and NBER, a Research Fellow at the Centre for Economic Policy Research, and is also a member of NBER’s Macro Annual advisory board. Dr Reis is an academic consultant of the Federal Reserve Board of New York and Richmond.

Ricardo Reis is Professor of Economics at LSE, on leave from Columbia University. He received his PhD in Economics from Harvard University in 2004. He has published extensively and has had a number of editorial positions in leading academic journals. He is a Research Associate at CFM and NBER, a Research Fellow at the Centre for Economic Policy Research, and is also a member of NBER’s Macro Annual advisory board. Dr Reis is an academic consultant of the Federal Reserve Board of New York and Richmond.