There is a growing body of literature focused on the link between income inequality and current account positions (see, for instance, this IMF working paper). The argument is essentially that rising income inequality induces ‘losers’ to borrow from abroad either out of habit or to “keep up with the Joneses”. This can have an impact on the extent to which a state has a current account deficit/surplus

Other studies support the idea that financial liberalisation causes income inequality rather than being the consequence of socio-economic pressures for liberalisation. Increasingly, capital flows, inequality and crises tend to be seen as components of the same phenomenon. Given recent developments in Europe, what can these insights have for the Eurozone?

Income inequality and Eurozone macroeconomic imbalances

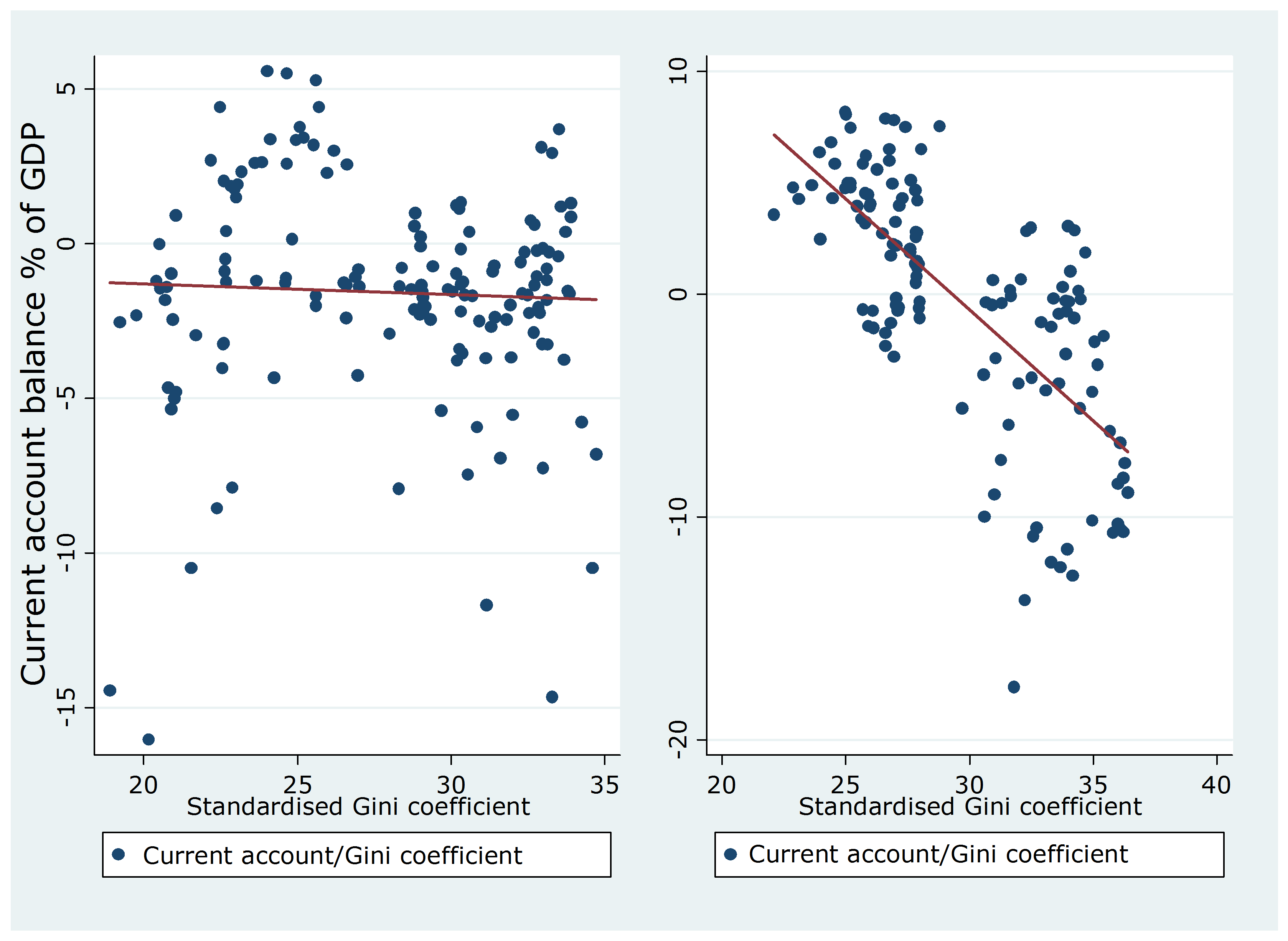

Figure 1 shows the relationship between current account positions and the standardised Gini coefficient for all the countries that entered the Economic and Monetary Union (EMU) in the first wave plus Greece. The Gini coefficient is a measure of the level of inequality within a state – as such the chart shows how levels of inequality and current account positions relate to one another.

The period 1980-2007 is divided in two sub-periods, 1980-1994 (the chart on the left) and 1995-2007 (the chart on the right). I choose the year 1995 to isolate the beginning of full capital mobility, as this is the average time around which the capital account was significantly liberalised for most prospective EMU members, as recorded by the so-called Chinn-Ito index. The data indicate that there is something about the relation between income inequality and current accounts that is specific to the 1990s, when European capital accounts were fully liberalised.

Figure 1: Income inequality and current account balances in the Eurozone between 1980 and 2007

Note: The chart on the left refers to the period between 1980 and 1994, while the chart on the right refers to the period between 1995 and 2007. The line shows that between 1995 and 2007, higher levels of inequality within a given country were correlated with greater current account deficits. Source: Own elaboration based on AMECO Database and Standardised World Income Inequality Database. The sample includes all countries that participated in the first wave of EMU (AT, BE, FI, FR, DE, IE, IT, LU, NL, PT, ES) plus Greece.

Financial liberalisation and household debt

The existing literature on euro area macroeconomic imbalances has not paid sufficient attention to within-country heterogeneity. Euro area countries are described in dichotomous terms as consisting of borrowers and creditors, but in fact household debt tends to be differently distributed across income groups in ways that vary from country to country. Available evidence indicates that socio-economic groups at the lower end of the income distribution tend to get more indebted than others, especially in unequal countries.

I argue that the large credit supply shock associated with EMU-induced capital account openness and the softening of credit market regulation during the mid-1990s implied a relaxation of collateral constraints for lower-income groups, whilst having no specific impact on other socio-economic groups. This generates the evidence that, with the establishment of the euro area, unequal countries – where the share of lower-income groups is relatively high – had worse external positions than equal ones, a hypothesis that finds support in the data.

Deleveraging

The question of who holds debt is important because it sheds light on the macroeconomic effects of deleveraging. To the extent that lower-income/skill groups were the first to be pulled out of the labour market during the crisis and hardly had financial buffers, they had no alternative but to deleverage the hard way, i.e. by significantly cutting down on consumption.

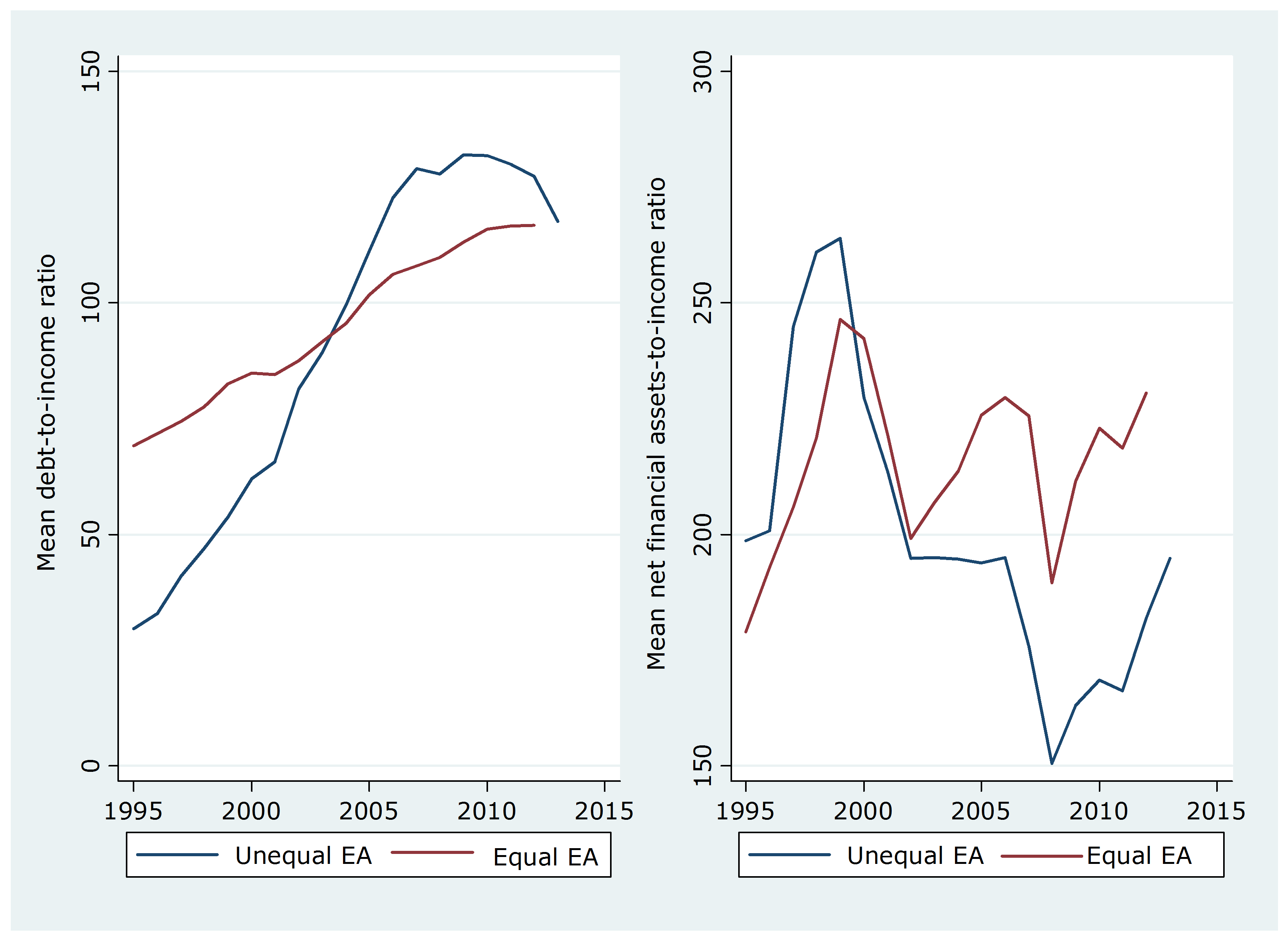

The chart on the left of Figure 2 compares the mean debt-to-income ratios in the unequal periphery with that of the equal core. While household indebtedness was on average higher in core countries for most of the 1990s, with the Netherlands in particular driving the results, it rose significantly in Southern European countries starting from the early 1990s, eventually overshooting the mean debt leverage of the core as of 2003. The phenomenon went hand in hand with an erosion of the net financial assets to income ratio in the periphery as opposed to the core, as shown in the chart on the right of Figure 2. That explains why households in the periphery were unprepared to withstand the large crisis shock.

Figure 2: Debt and net financial assets to income ratios, 1995-2011

Source: Own elaboration based on Eurostat. The sample includes all countries that participated in the first wave of EMU (AT, BE, FI, FR, DE, IE, IT, LU, NL, PT, ES) plus Greece.

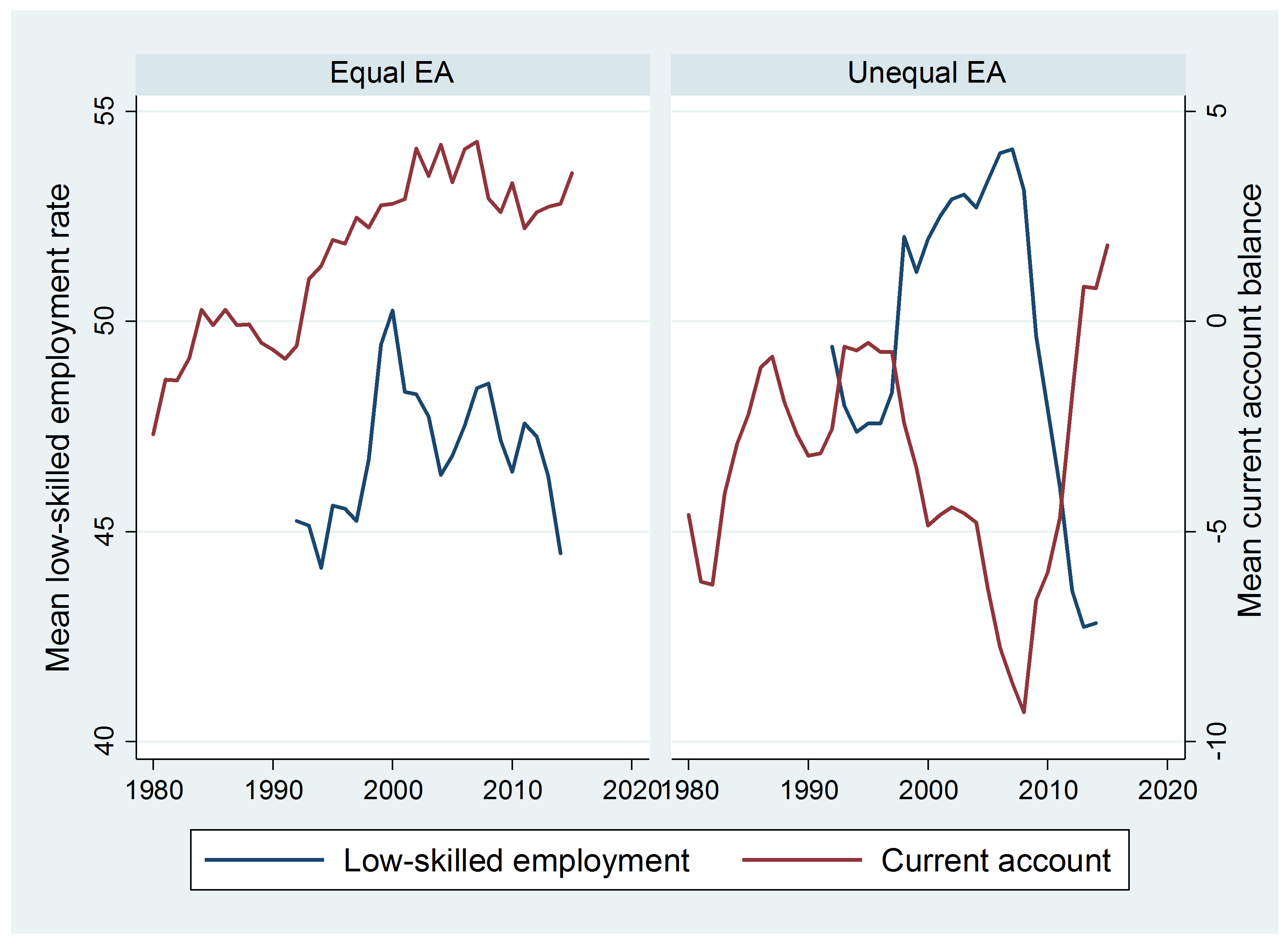

The distributional effects of the crisis on categories of workers adds to the explanation of an asymmetric reversal. Indebted low-skilled workers were the first to be pulled out of the labour market. Figure 3 plots the evolution of the current account balance and of the employment rate of the lowest-skilled across the equal core and the unequal periphery. In the periphery, with the massive collapse of employment for the least skilled came a drop in consumption that led to a significant correction in current account deficits (shown in the chart on the right of Figure 3. By contrast, the data do not suggest any significant relation between low-skilled employment and external positions in the core (as shown in the chart on the left of Figure 3).

Figure 3: Current account balances and low skilled employment in the euro area 1995-2014

Source: The low-skilled employment rate is given by the employment rate of those with pre-primary and primary education. Source: Own elaboration. Unequal countries = EL, ES, IR, IT, PT. Equal countries = AT, BE, DE, FI, FR, NL.

Policy lessons

EMU-induced financial liberalisation had a differentiated impact on euro area members depending on the country-specific income distribution. In particular, it generated large current account deficits in unequal countries, where the share of the lower-income previously credit-constrained group was relatively high.

The same perspective is useful for understanding the reversal of current account deficits, as the crisis and the ensuing credit constraints forced deleveraging onto the same portion of the population that got indebted in the first place and that had no alternative but to restrain consumption considering that lower-income/skill workers were the first to be pulled out of the labour market and hardly had financial buffers.

It follows that, first, appropriate financial regulation prior to the crisis would have contributed to softening the debt cycle in the periphery. Second, policy measures during the peak of the crisis should have included clear restructuring procedures and outspoken interventions in support of certain categories of workers in the periphery.

♣♣♣

Notes:

- This post appeared originally at LSE Europp.

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Before commenting, please read our Comment Policy

Benedicta Marzinotto is a Lecturer in Political Economy at the University of Udine, Visiting Professor at the College of Europe, and a Fellow at Large at Bruegel.

Benedicta Marzinotto is a Lecturer in Political Economy at the University of Udine, Visiting Professor at the College of Europe, and a Fellow at Large at Bruegel.