Had things gone as most commentators expected, the UK would now be entering hard Brexit talks with the near certainty of leaving the single market and/or customs union and the consequent ending of free movement of people from the European Union. Two weeks later and that near certainty no longer seems as certain, with murmurings of a softer Brexit and the implication that allowing freer movement of labour from the EU may now be up for discussion.

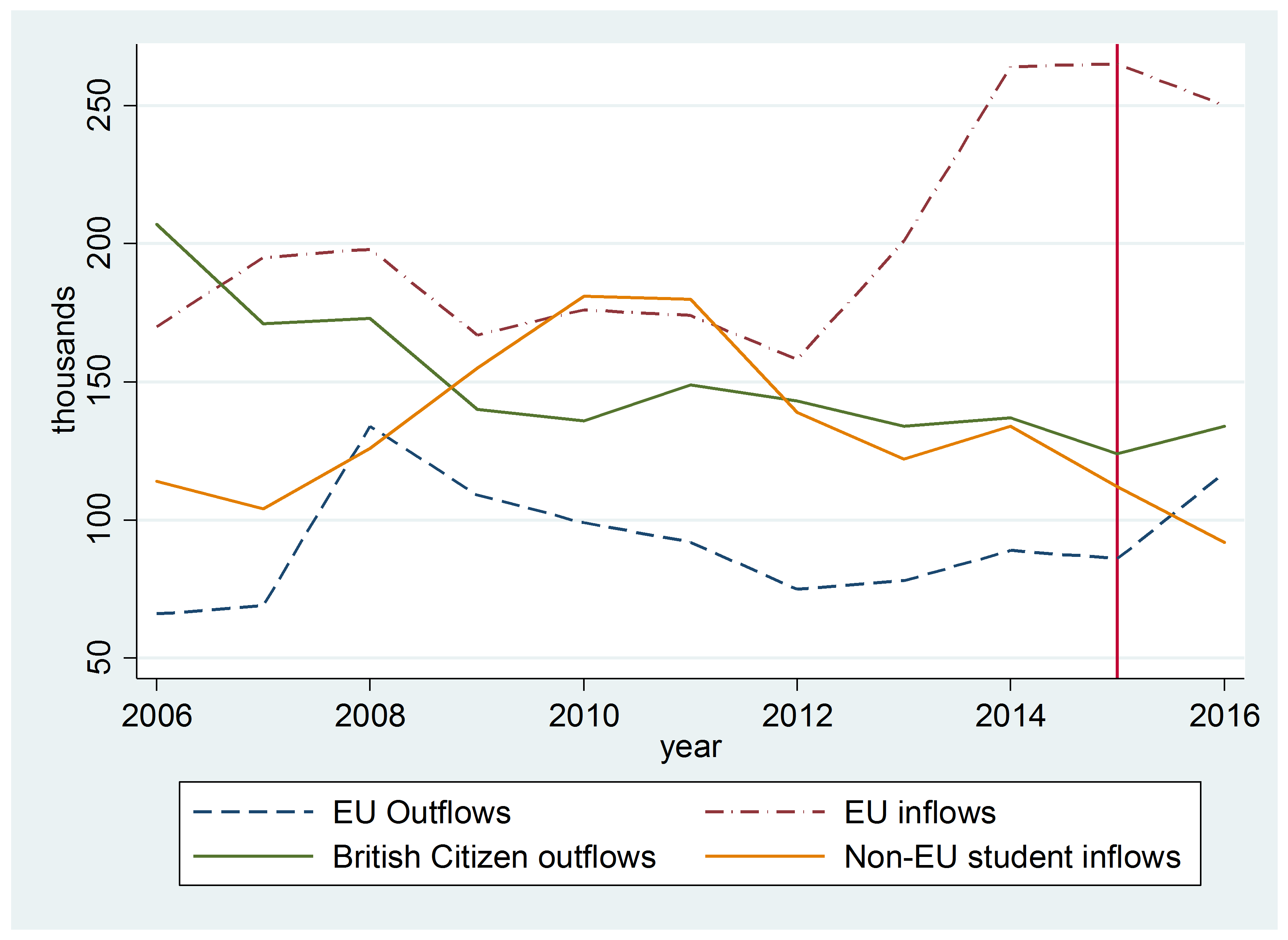

Net migration to the UK has been falling for around a year now. Figure 1 shows that this is not simply because of reduced inflows from the European Union, but largely because of a rise in the number of EU nationals leaving the UK, alongside a rise in emigration of British citizens (and a fall in the numbers of non-EU students, at least according to the International Passenger Survey from which the migration figures are taken). These features are normally associated with an economic slowdown and are largely beyond government control.

Figure 1. Recent UK Migratory Inflows and Outflows

Source: IPS

If, as might be possible at time of writing, the UK economy stalls further while many of the EU economies begin to grow more rapidly, then there may be further falls in the net migration figure – again for reasons beyond government control. Migrants seeking work will be attracted to the best employment opportunities. If there are suddenly more opportunities in mainland Europe we would expect more migrants to choose Germany, France or Spain rather than the UK. The 15 per cent fall in sterling relative to the Euro over the last year also makes UK wages 15 per cent less attractive relative to a job in the Eurozone to prospective migrants. So the inflow to the UK could fall over the next few months reducing the net migration numbers without the government having done anything other than preside over a stalled economy. This means that even in the absence of a hard Brexit, a seemingly never-ending supply of European labour – faced with increasing better alternatives elsewhere – must be in doubt.

While government can do little to influence emigration by British citizens or the arrival rates of EU migrants – at least not while a member of the EU, here is the policy dilemma for the government. Any rowing back on ending free movement would immediately conflict with the net migration target of 100,000 – a key feature of the Conservative party manifesto. If we assume that this is still in play, the continued allowance of free movement from the EU is – around half of the net migration number – would obliterate any attempts to hit such a target within a parliament.

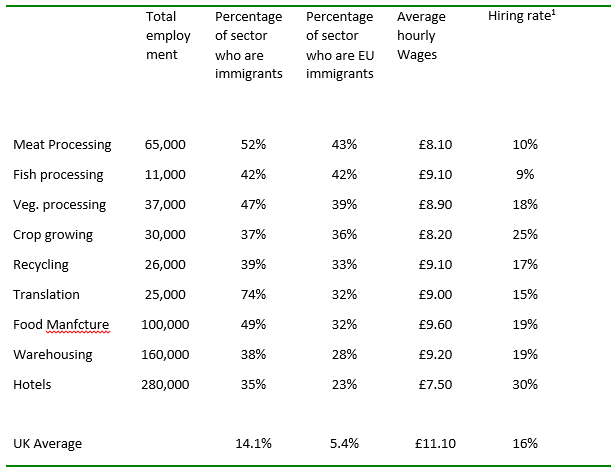

Would this matter for UK businesses? Certain businesses undoubtedly rely a lot on EU labour. Immigrants make up 14 per cent of the employed workforce and EU migrants comprise around 5 per cent of the workforce but these proportions rise significantly for certain agricultural and manufacturing sectors where, as the Table below shows, the immigrant share is close to 50 per cent and EU workers often comprise more than a third of the workforce. Most of these sectors are small in terms of total number employed but their reliance on migrant labour is clear. They are also typically low wage, high labour turnover sectors.

Should the UK end up with a hard Brexit then most of these existing EU workforce in these sectors and elsewhere would still be eligible for British citizenship or leave to remain (having the requisite years of residence). So the workforce is unlikely to disappear overnight.

It is at the hiring margin that employers in these industries may face difficulties after Brexit without some sort of sectoral quotas, seasonal schemes or adjustment period. The annual hiring rate is typically between 15 per cent of the total workforce. But low wage sectors such as those in the Table tend to have higher turnover. Turnover in the hotels sector is close to one third of the workforce.

Unless there is an eventual agreement to stay in the single market recruitment from the EU is unlikely to continue at similar volumes after Brexit.

Non-EU work visas to the UK are currently restricted to “graduate-level” jobs. Most of the sectors in the Table (excepting translation services) are non-graduate jobs – although there are some graduates undoubtedly working in these sectors.

Any quotas on work visas on EU nationals after Brexit are also likely to favour graduate sector jobs because the net fiscal benefit is higher. High paid workers tend to put in more than they take out in benefits and public services. So certain firms and sectors would also have to look around for different sources of labour, raise wages or change their methods of working (though any firm that relies on a never ending supply of EU workers in an environment of free movement has an unstable business model).

Table 1. Sectoral distribution of EU immigrants, 2016

Source: LFS. Note 1. Hiring rate is % of workforce in employment for less than 1 year. Average wage is median hourly wage of all employees in the sector.

Business has long argued for the freedom to hire the best people for the job – though no country in the world allows business unfettered access to migrant labour or allows them complete freedom to set wages or other employment conditions. In the UK, at the less skilled end of the labour market, the national minimum wage, the soon to be revamped Labour Inspectorate ensure that wages and working conditions are regulated. The issue for a minority of employers going forward is how to adjust to a labour market in which one particular source of less skilled workers is likely to be restricted.

♣♣♣

Notes:

- This blog post is based on the author’s Immigration and the UK Economy, Election Analyses Series, LSE’s Centre for Economic Performance (CEP).

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: London Heathrow Terminal 5 customs queue, by Cory Doctorow under a CC-BY-SA-2.0 licence

- Before commenting, please read our Comment Policy.

Jonathan Wadsworth is professor of economics at Royal Holloway College, University of London, and a senior research fellow at the LSE’s Centre for Economic Performance. He was a member of the Home Office’s Migration Advisory Committee from 2007 to 2016.

Jonathan Wadsworth is professor of economics at Royal Holloway College, University of London, and a senior research fellow at the LSE’s Centre for Economic Performance. He was a member of the Home Office’s Migration Advisory Committee from 2007 to 2016.