There has recently been a renewed interest in the old idea that business cycles could be driven by changes in the expectations about future economic conditions, the so-called “animal spirits” (early references are Pigou, 1927, and Keynes, 1936). “Animal spirits” in technology are an important source of business cycles. They explain about 30 per cent of the volatility of GDP.

What are ‘animal spirits’ in technology?

Suppose that a discovery of a potential new technology is announced: a new and cheap material has been developed at the research laboratory of company XY and there are rumours that this new material could be used to produce fast, reliable, cheap and efficient microprocessors. Now the industrialisation phase of the new microprocessor is happening.

Suppose that you are an investor deciding whether to invest in the development of the microprocessor by buying stocks of company XY. After the announcement has been made public, there is still uncertainty on the outcome of the industrialisation phase. It could be that it will turn out positive, granting profits to the investors and the general state of technology will improve. Technology reaches a new frontier and stimulates GDP, consumption and investment. Or it could also be that the development phase fails: it may turn out to be impossible to use the new material to develop the new microprocessor. The general level of technology does not improve and in turn, GDP, consumption and investment do not react.

We model this situation, as other authors in the literature, as individuals receiving signals from the firm. The signals are the sum of two unobservable components: one is a component that relates to improvements in technology; the other is a component that shifts expectations of a technological improvement, but eventually no improvement happens. Clearly, the two components are unobservable.

Given the signal, the investor has to decide how much to invest in the firm. Only after some time she will realise whether the investment is profitable or not.

We study the role of “animal spirits” as sources of business cycle fluctuations surrounding the arrival of new technology, and find that they explain a substantial fraction of the volatility of GDP, consumption and investment, in the order, on average, of 35 per cent. We also find that the response of GDP, consumption and investment to “animal spirit” shocks is hump-shaped and the long-run effect is zero. Given our results, we claim that expectations of future changes in economic fundamentals should be considered as a major source of business cycle fluctuations.

A classical result in this literature shows that, given the uncertainty on what caused the increase in the signal, the response of the economy to both components, a shock to technology and a shock to expectations unrelated to technology, is the same on impact.

As investors only see the signal increasing without knowing what is the cause of the increase, they react by buying stocks. GDP, consumption and investment increase. But the positive response of the economy is smaller than the response that would have happened if investors knew for sure that there was a shock to technology. The increase in GDP, consumption and investment on the other side is larger than the increase that would have happened if investors knew that there was an “animal spirit” shock.

Suppose now that after some time it is possible to see the final effect of the industrialisation phase. If it was successful and technology is increasing, the economy gradually reaches a new level of activity; if it was unsuccessful, technology stays put and the economy returns to its initial state. As you can see, business cycles are generated by shifts in expectations, unrelated to economic fundamentals or to technological shifts.

We believe that assuming that agents base their decisions on noisy information seems quite plausible, in particular for events – like improvements in technology – whose effects propagate slowly and therefore are not immediately revealed by observable economic variables. In the world, agents are often uncertain about the future effects of news becoming available. Assuming that they are not aware of the exact nature of such news and use the information at hand optimally, is a simple and convenient way to model this kind of “conditional” uncertainty.

In our empirical work, we measure the response of the US economy to an unobserved shock that increases technology (we call it a “real” shock) and an unobserved shock that does not affect technology (we call it a “noise shock”). The latter is an “animal spirit” shock: an event that changes public’s expectations, but does not change the economic fundamentals.

The econometric methodology is quite complex — we refer to the paper for details. It suffices to highlight that our strategy uses the idea that sometime in the future it is possible to see the final effect of the industrialisation phase.

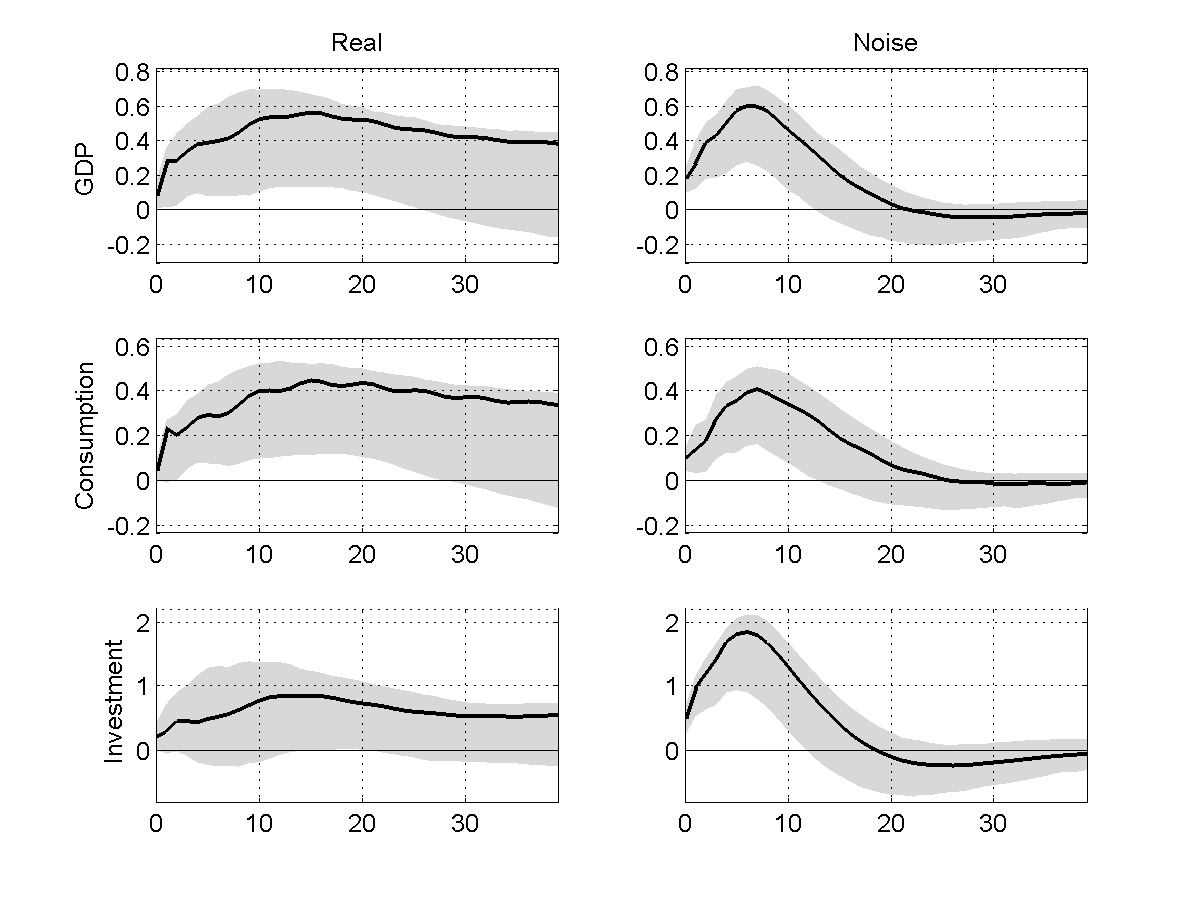

Figure 1. Estimated responses of the US economy (The left column displays the response of the economy after a technology shock. The right column displays the response after a “noise” shock.)

Both shocks increase on impact GDP, consumption and investment. The technology shock (left) has a long-run effect on the economy: agents realise that technology has increased and consume and invest more. The noise shock only has a temporary effect. Once agents realise that the shock was noise, they reduce consumption and investment. The long-run effect is zero. The fraction of the volatility of GDP generated by noise shocks is around 30 per cent. We therefore claim that expectations of future changes in economic fundamentals should be considered as a major source of business cycle fluctuations.

♣♣♣

Notes:

- This blog post is based on the authors’ paper Noisy News in Business Cycles, American Economic Journal: Macroeconomics, forthcoming.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Noisy signal (edited), by Mark Donovan, under a CC-BY-NC-SA-2.0 licence

- Before commenting, please read our Comment Policy.

Luca Sala is associate professor of economics at Bocconi University, Italy. He is also a research fellow at the Innocenzo Gasparini Institute for Economic Research (IGIER). He has participated in the European Central Bank’s graduate research program; been a visiting student at Tel Aviv University; and a visiting scholar at New York University’s Department of Economics. He has taught at Lisbon’s Universidade Nova and University of Oslo.

Luca Sala is associate professor of economics at Bocconi University, Italy. He is also a research fellow at the Innocenzo Gasparini Institute for Economic Research (IGIER). He has participated in the European Central Bank’s graduate research program; been a visiting student at Tel Aviv University; and a visiting scholar at New York University’s Department of Economics. He has taught at Lisbon’s Universidade Nova and University of Oslo.

Luca Gambetti is an associate research professor at Barcelona’s Graduate School of Economics (BGSE) and an associate professor of economics at Barcelona’s Autonomous University (UAB). He has a PhD in economics from the Pompeu Fabra University. His main research inteests are in macroeconometrics, macroeconomics, monetary economics and time series econometics.

Luca Gambetti is an associate research professor at Barcelona’s Graduate School of Economics (BGSE) and an associate professor of economics at Barcelona’s Autonomous University (UAB). He has a PhD in economics from the Pompeu Fabra University. His main research inteests are in macroeconometrics, macroeconomics, monetary economics and time series econometics.

Mario Forni is professor of economics at the University of Modena and Reggio Emilia (Unimore), Italy. His research interests are in the areas of dynamic macroeconomics, time series analysis, and large factor models. He had done work for the European Commission, Bank of Italy and Bank of France.

Mario Forni is professor of economics at the University of Modena and Reggio Emilia (Unimore), Italy. His research interests are in the areas of dynamic macroeconomics, time series analysis, and large factor models. He had done work for the European Commission, Bank of Italy and Bank of France.

Marco Lippi is a research fellow at the Einaudi Institute for Economics and Finance. His research interests are in prediction of macroeconomic aggregates; large-dimensional factor models; structural VAR analysis; aggregation in macroeconomics; stochastic processes; and time series.

Marco Lippi is a research fellow at the Einaudi Institute for Economics and Finance. His research interests are in prediction of macroeconomic aggregates; large-dimensional factor models; structural VAR analysis; aggregation in macroeconomics; stochastic processes; and time series.