In April 2017, the World Bank tabled a fairly optimistic forecast for commodity prices for 2017 and 2018 anticipating: crude oil to average $55 per barrel in 2017 before nudging further north to $60 in 2018; a 26 per cent rise in the price of energy commodities (including natural gas and coal) in 2017 and a more moderate 8 per cent increase in 2018; and finally the first rise in five years of non-energy commodities prices in 2017.

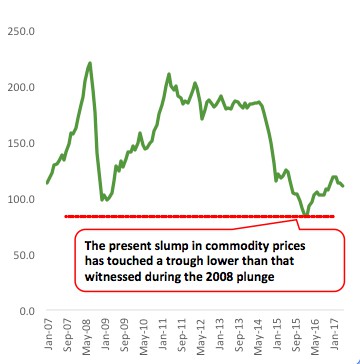

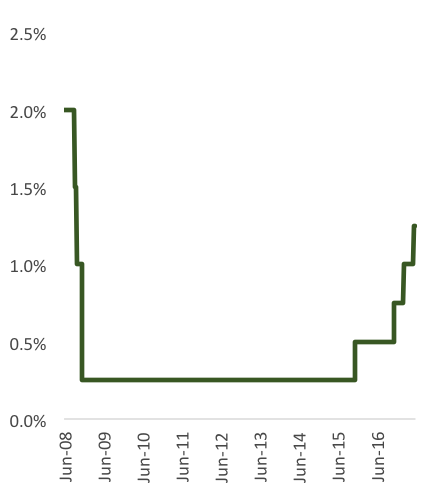

Whereas there is little, if any, consensus that the trough of the present rout in commodity prices could be behind us, sustained uptick in the overall commodity price index from the January 2016 low has presented a reassuring indicator for many countries. In Africa, subdued commodity prices and anticipated rate hikes in advanced markets had necessitated a common monetary policy path between 2014 and 2015. Now, evidence of growing divergence in monetary policy suggests there is mounting confidence amongst central banks that those pressures are declining.

Today, countries such as Uganda, Ghana and Rwanda have assumed a dovish stance; Kenya, South Africa and Nigeria have adopted a generally neutral approach characterised by retention of benchmark rates; whilst in economies such as the Democratic Republic of Congo (DRC) and Egypt, central banks continue to tighten the monetary environment.

Figure 1. All Commodity Price Index (2005 = 100)

Source: International Monetary Fund, Bloomberg

Figure 2. USA Federal Funds Rate (Upper Target)

Source: International Monetary Fund, Bloomberg

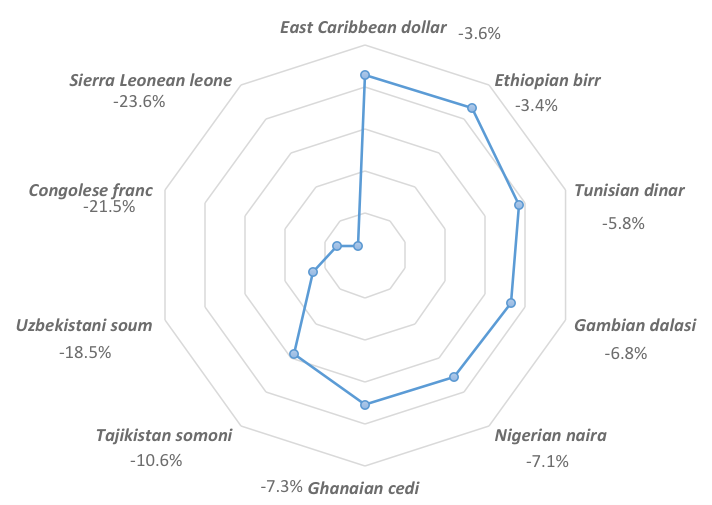

This checkered picture has, however, veiled a trend that ought to prick our interest with regard to the foreign exchange market and could be one of the defining legacies, in Africa, of the plunge in commodity prices. In the first six months of 2017, 70 per cent of the world’s worst performing currencies were in Africa, with the list including Ethiopia’s birr, Tunisia’s dinar, Gambia’s dalasi, Nigeria’s naira, Ghana’s cedi, the DRC’s franc and Sierra Leone’s leone. In the same period in 2014, 2015 and 2016, African currencies accounted for 30 per cent, 40 per cent and 60 per cent, respectively, of the world’s worst performing currencies.

Africa’s growing presence in this basket of underperforming currencies should be of interest to both investors and policy makers. It brings to visibility the double whammy that a number of economies in the continent are confronting ─ constrained fiscal space to mitigate the economic downturn, occasioned by depressed commodity prices, as well as minimal capacity to adopt expansionary monetary policy as local currencies come under pressure and, in some instances, inflation surges to double digits, necessitating hawkish adjustment. This challenge is particularly dire for commodity-reliant low-income countries (those with Gross National Income per Capita that is less than $ 1,025).

Figure 3. World’s Worst Performing Currencies (Spot Rate to $ Change January – June 2017)

Source: Bloomberg

Consider the case of Sierra Leone and DRC, both countries having their currencies at the bottom of the heap of worst performing. With domestic credit to the private sector/GDP ratio at 4.8 per cent and 6.8 per cent, respectively, against an average of 46.1 per cent for Sub-Saharan Africa (excluding high income countries), shallow financial depth becomes the first impediment to the potency of monetary policy in mitigating the effects of the ongoing economic slump.

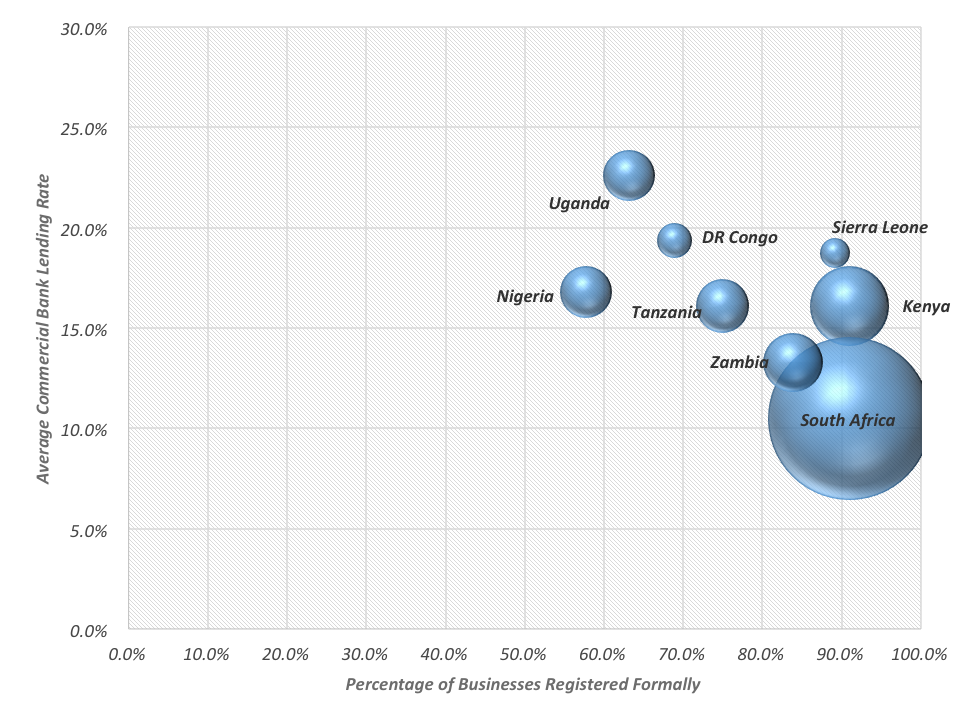

This shallow penetration of domestic credit to the private sector could be informed by a number of factors, two of which are a large informal economy that inhibits businesses’ ability to access credit from formal lenders and a relatively high cost of credit that locks out would-be borrowers. As illustrated in the graph below, DRC has both a low proportion of businesses which are formally registered at the point of inception and relatively high commercial bank lending rates, whereas South Africa enjoys both low cost credit and a high proportion of businesses which are formally registered at the start of operations.

Figure 4 Commercial Bank Lending Rates, Formal Registration of Businesses & Domestic Credit to Private Sector to GDP Ratio

Note: Size of bubble denotes domestic credit to private sector to GDP ratio. Source: World Bank Enterprise Survey, World Bank Development Indicators

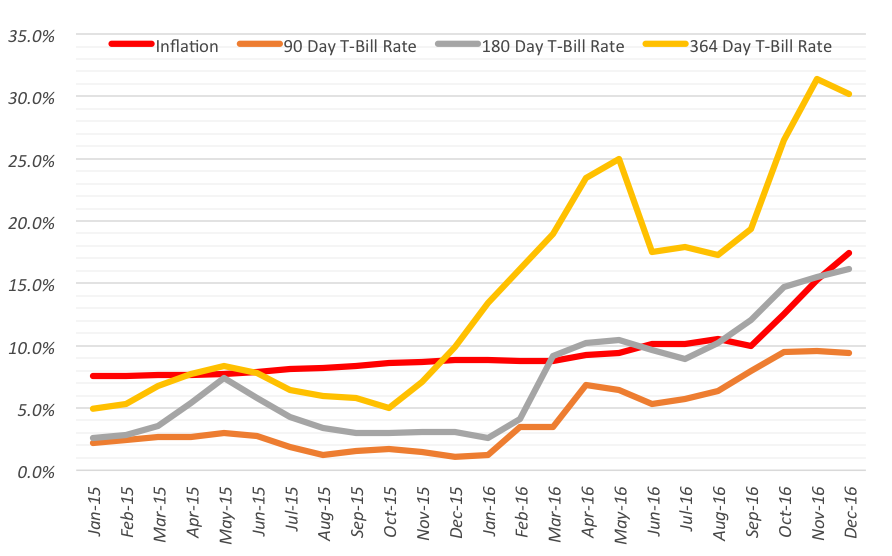

In low-income economies such as Sierra Leone, where inflation has soared to double digits, expensive credit is as much a headache for the public sector as it is for the private. Yields in the fixed income market are trending upwards to highs which in the recent past would have been widely deemed beyond reach (the latest available data from the Bank of Sierra Leone shows that the country’s 364-day Treasury Bill yield stands at about 30 per cent from a low of 4.9 per cent in January 2015). This is important for two reasons:

- From a monetary perspective, it suggests there is a sense in which investors are far from convinced that runaway inflation has been tamed in such economies in spite of sustained monetary tightening. This could explain why in just six months, January to June 2017, DRC’s Central Bank hiked its benchmark rate by 1,300 basis points to 20 per cent as inflation closed May at 33.7 per cent (National Bureau of Statistics DRC)

- From a fiscal standpoint, it shows that already cash strapped governments are having to bear the burden of borrowing from the domestic markets at interest rates they can ill afford for such short periods. The first challenge stemming from this trend is a potentially weakened debt sustainability position should governments undertake a debt binge at such expensive rates. An accompanying challenge is the fact that with evolving global monetary conditions, Sub-Saharan Africa’s leverage in a low interest rate environment for cheap credit from the international market is diminishing.

Figure 5. Interest Rate Trend in Sierra Leone

Source: Bank of Sierra Leone

Despite the size, we should be wary of frail recovery by low-income economies

A lot of focus is presently directed towards the risks that South Africa and Nigeria, both economies in the throes of a recession, pose for Africa’s economy. This focus is not misplaced. The two economies account for 35.8 per cent of the continent’s GDP (World Bank 2015 GDP Data) and adverse conditions are likely to drag the entire region’s momentum.

It should not be lost to us, however, that low-income economies today account for about 14.5 per cent of the continent’s GDP and that over the last decade, 2005 – 2015, countries such as Ethiopia and DRC have been growth pace setters across the continent, with the former quintupling its GDP size to $ 61.5 billion. Faced with fiscal and monetary policy constraints, commodity-reliant, low-income economies are set for a policy dilemma as far as stimulating recovery and launching onto a path of sustainable long-term growth is concerned.

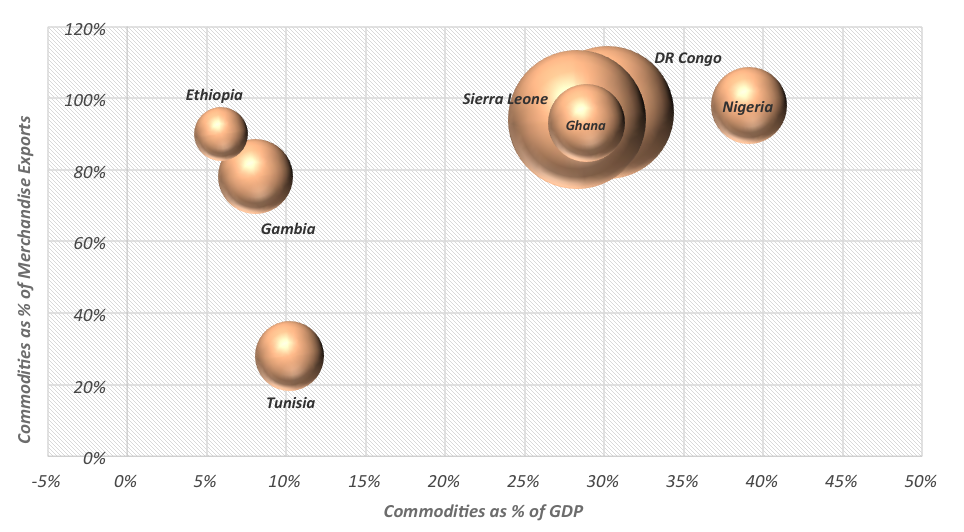

On the whole, there is need for economic transformation across these countries ─ one, at the risk of flogging a dead horse, more diversified economies should help mitigate the hangover from commodity related shocks in future. From the illustration below, one can see that currencies whose economies are less reliant on commodities such as Tunisia and the Gambia have been more resilient than currencies for Sierra Leone and DRC whose economies are significantly reliant on commodities.

Figure 6 Commodity Reliance & Currency Depreciation

Note: Size of bubble denotes the percentage of depreciation between January 2017 and June 2017 Source: UNCTAD data, Bloomberg

Last but not least, most low income economies need deeper savings reserves to facilitate governments’ ability to mobilise resources especially in times when adverse economic conditions occasion subdued tax revenue ─ in Mozambique, for instance, the gross savings-to-GDP ratio stands at 5.9 per cent compared to Sub-Saharan Africa’s average of 15.4 per cent.

♣♣♣

Notes:

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: by Julians Amboko

- When you leave a comment, you’re agreeing to our Comment Policy.

Julians Amboko is a Senior Research Analyst with StratLink Africa Ltd, a Nairobi-based financial advisory firm focusing on emerging and frontier markets. He covers macroeconomic research and analysis for Sub-Saharan Africa, including markets such as Nigeria, Kenya, Ethiopia, Ghana, and Angola. He tweets at @AmbokoJH

Julians Amboko is a Senior Research Analyst with StratLink Africa Ltd, a Nairobi-based financial advisory firm focusing on emerging and frontier markets. He covers macroeconomic research and analysis for Sub-Saharan Africa, including markets such as Nigeria, Kenya, Ethiopia, Ghana, and Angola. He tweets at @AmbokoJH