Each day brings with it new drama in UK politics and the course of Brexit – and it’s playing havoc with the UK economy. The following four graphs show the extent that the UK is at risk of a recession – and I conclude that the only way to put an end to all the uncertainty that is plaguing investment and markets is to have another referendum.

1. Uncertainty

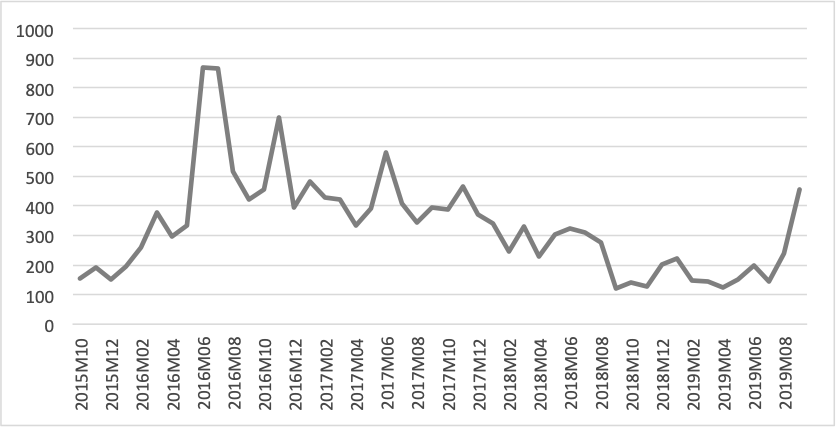

Boris Johnson wants to deliver Brexit, with or without a deal. Of this he is certain. But Brexit-related policy uncertainty is on the rise and this is already harming the UK economy. The following graph shows how UK policy uncertainty spiked in 2016 around the time of the Brexit referendum and is on the rise again now.

Figure 1. UK policy uncertainty index

Source: Economic Policy Uncertainty Index. The Conversation CC-BY-ND

Uncertainty is measured by the discussion of policy uncertainty across 650 UK newspapers, reflecting business and consumer confidence in the economy. When uncertainty rises, this knocks the pound sterling currency down as investor confidence in the UK falls.

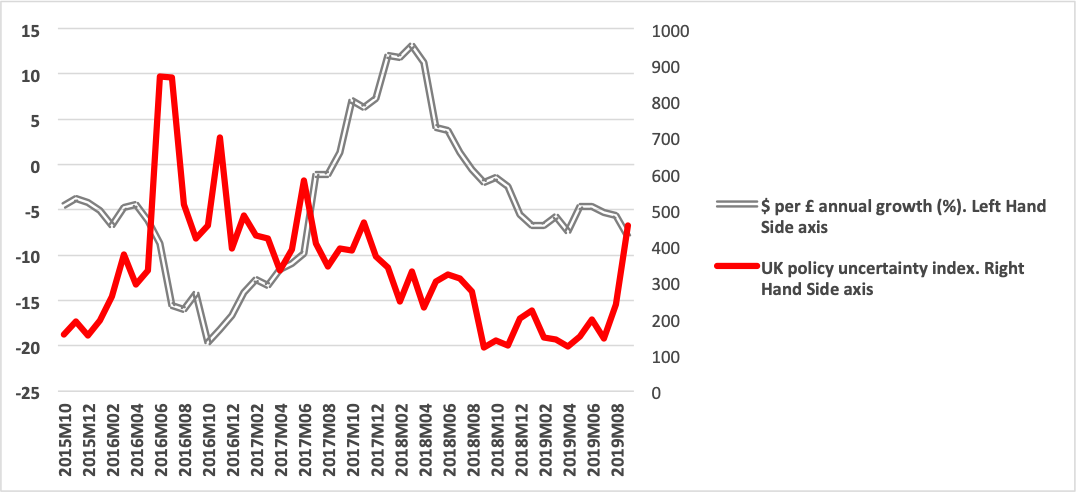

2. Fall in the pound

Figure 2. Spot exchange rate (US$ into sterling) movements and policy uncertainty

Notes: Chart – The Conversation. Source: Bank of England. The Conversation CC-BY-ND

The weaker pound makes imports more expensive, which pushes up the prices of a number of consumer goods, causing inflation. In its July report, the Bank of England had predicted inflation to drop from 2.1 per cent in July 2019 to 1.56 per cent by the end of the year and remain below the 2 per cent inflation target until the third quarter of 2020. But, following recent events, the bank’s governor, Mark Carney, has revised his inflation estimates, saying it could more than double to 5.5 per cent.

This puts the Bank of England in a tricky situation. It will have to decide whether to raise interest rates to tackle inflation or cut them to stimulate economic growth.

3. Risk of recession

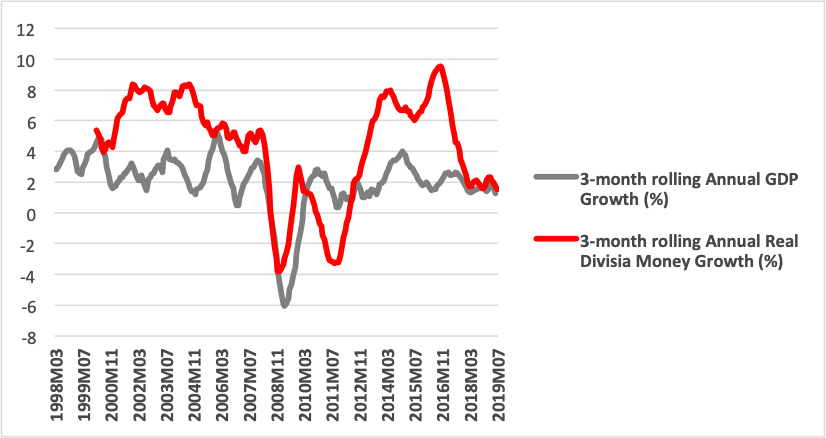

Government data suggests that the UK economy contracted by 0.2 per cent in the second quarter of 2019. A recession occurs when there are two successive quarters of negative GDP growth. Early evidence suggests that the economy might already be heading this way because money growth, a reliable predictor of UK GDP growth, has weakened significantly.

The next chart plots together real money growth, using the Divisia money index, and GDP growth. The Divisia index weighs different forms of money according to their likelihood of being spent – notes and coins have a higher weight than money held in mutual funds, for example. My research shows this measure of money has strong predictive power for the UK economy, and the latest growth rates of money are at a seven-year low.

Figure 3. Real money growth, using the Divisia money index, and GDP growth

Source: Costas Milas, CC-BY-ND.

This indicates that GDP growth in the third quarter of 2019 might be as bad as in the second quarter of 2019. In other words, there is evidence of a looming recession whether or not the UK leaves the EU on October 31. The latest UK output surveys also point to a looming recession.

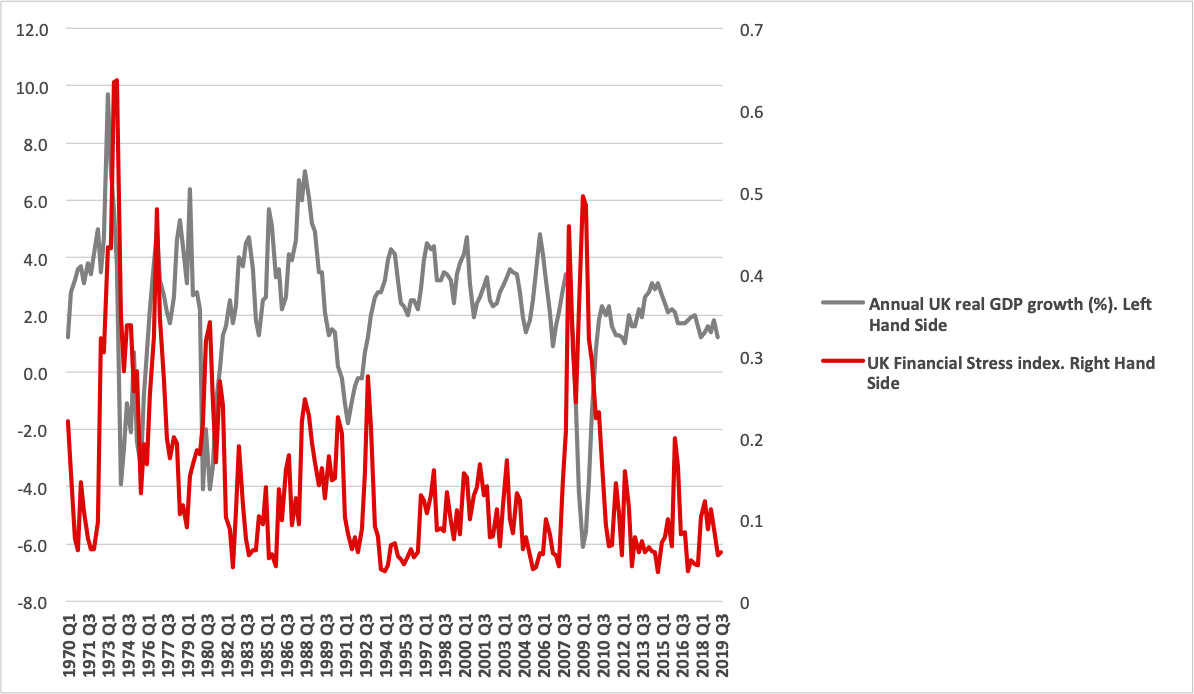

4. Financial stress

A Brexit-related UK recession is far from certain, however, and it might not be too late to change course. Another reliable predictor of UK growth developments is the UK financial stress indicator. This pools information from the volatility of the exchange rate, the volatility of the equity market, the volatility of the bond market and the risk premium that investors demand to hold UK corporate bonds rather than the less risky UK government bonds.

Figure 4. The UK financial stress indicator and UK growth

Source: Costas Milas, CC BY-ND

From a historical point of view, a rise in financial stress signals a slowdown in UK growth between one and three quarters prior to UK growth turning negative. Notice, however, that the latest financial stress data is pretty subdued – which does not point to a forthcoming UK recession. This is largely because market participants expect the Bank of England to step in by cutting interest rates and authorising additional quantitative easing to counteract the rise in financial stress caused by a possible no-deal Brexit.

What the UK needs

If there is a snap election, policy uncertainty will remain high. The latest polls suggest another hung parliament and this will solve nothing.

What the UK really needs is another referendum. There have been suggestions of a three-way referendum where people vote to remain in the EU or leave with the deal that Theresa May negotiated or a no-deal Brexit. Financial Times journalist James Blitz suggests a remain versus no-deal Brexit referendum to end the deadlock.

But I think the referendum should be solely between Theresa May’s deal (which is still on offer) versus a no-deal Brexit. Though I am myself a committed “Remainer”, I believe this is the only way to respect the previous referendum vote. It is also the best way to end the uncertainty that is plaguing business and investor confidence in the UK economy.

The best outcome will be to accept May’s withdrawal agreement (or a last minute slightly “tweaked” version of it) and move on. The Bank of England, and rightly in my view, forecasts that a no-deal Brexit will be very damaging.

I have argued further that the UK’s banking sector might struggle to absorb a potentially huge drop in bank deposits as customers will be looking for alternative returns outside a sinking (at least in the short-term) UK economy. So those in favour of no-deal should be brave and detailed enough to tell the rest of us why no-deal will not be damaging.![]()

♣♣♣

Notes:

- This blog post appeared originally in The Conversation. Please note that after feedback from readers, Professor Milas has supplied us with a version of Figure 2 which is slightly different from the one originally appearing in The Conversation.

- The post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image by Skitterphoto, under a Pixabay licence

- Before commenting, please read our Comment Policy

Costas Milas is professor of finance at the University of Liverpool. Email: costas.milas@liverpool.ac.uk

Costas Milas is professor of finance at the University of Liverpool. Email: costas.milas@liverpool.ac.uk

Whatever the results there will be pain as a result of Brexit. The process has dragged on for so long and the people and economy are paying the price. The UK should exit the EU with or without deal. The UK should move on in its relationship with EU and never look back. Bashar H. Malkawi