There is broad consensus on the desirability of making markets more efficient, across several economies to increase competitiveness and improve future growth prospects (OECD, 2012; European Commission, 2013; IMF, 2016; OECD, 2012). In the current policy context, advancing structural reforms is of paramount importance to address the decline in productivity growth — the key long-term driver of living standards — which fell sharply following the global financial crisis and has remained sluggish ever since (IMF, 2017).

Growing focus is also placed on the link between structural reforms and public finances, to address the growing public indebtedness across the world since the global financial crisis. In this context, better knowledge of the implications of structural reforms for public finances is required to better design and prioritise packages of growth-enhancing reforms. Two broadly opposite views have been expressed in the recent debate on the relations between fiscal policy and structural reforms (Buti et al., 2007). The first view suggests that structural reforms and improvements in the fiscal stance are hardly compatible, so that policy authorities may be left with a dilemma. According to this view, excessively tight constraints to fiscal policy may be incompatible with reform objectives and may reduce the political capital of government to implement reforms. Another view suggests that fiscal discipline and reforms not only are not incompatible but tend to go hand in hand. In addition, reforms can improve debt sustainability by increasing output, the tax base, and, therefore, reducing debt-to-GDP ratios.

In addition to these views, two key considerations must be taken into account. First, the budgetary effects of structural reforms may materialise over different horizons, requiring an analysis of their impact over time. Second, the channels of transmission can be complex because the effect of reforms on fiscal positions may depend on initial conditions. These aspects warrant a systematic analysis of the interaction between fiscal policy and structural reforms.

A few theoretical papers have directly studied the relationship between structural reforms and fiscal policy (e.g. Campoy and Negrete, 2010; Muller et al., 2016; Papageorgiou and Vourvachaki, 2017; Sajedi, 2018). Empirically, some papers have related structural reforms to fiscal adjustment programs (e.g. Kumar et al., 2007; Tagkalakis, 2009; Heylen et al., 2013; Deroose and Turrini, 2005). Contributing to the existing empirical literature, in a recent study we examined the effect of structural (domestic and external finance, trade, and product market) reforms on public debt for a sample of ninety advanced and developing countries spanning between 1973 and 2003. Our study, forthcoming in Campos, De Grauwe and Ji (2020) was built on earlier work by Ostry et al. (2009). More specifically, using these authors´ cross-country dataset of major regulatory policy changes, we estimated the dynamic response of public debt to these reforms using the local projection method (Jordà, 2005).

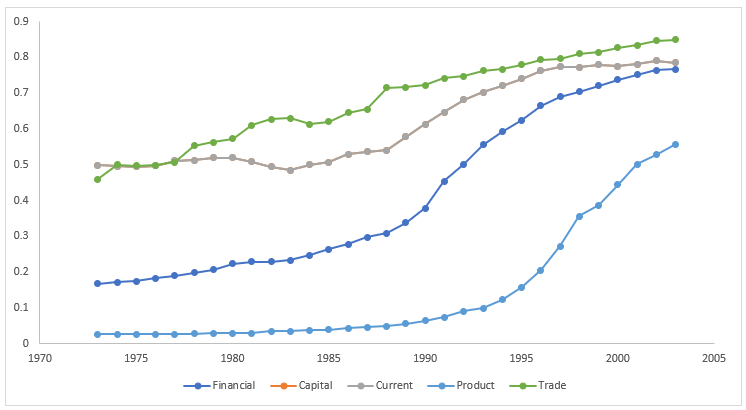

Figure 1 sums up the different structural reforms’ cross-country and time-series patterns for the entire sample. On average, trade reforms display a gradual liberalising trend throughout the entire period, while both capital and current account reforms tightened slightly in the late 1970s and early 1980s. Both domestic finance and product market reforms witnessed relatively little action until the late 1980s, but they picked up a liberalising path very fast afterwards.

Figure 1. Evolution of all structural reform indicators, full sample

Source: Ostry et al. (2009)

The average patterns shown in Figure 1 hide several heterogeneities between income groups. For domestic finance and product market reforms, the aggregate average patterns translate well the behaviour of the different income groups. However, capital account reforms show different trends: in advanced economies liberalisation has been the norm since the early 1970s, while in emerging and low-income countries, this movement only began in the later 1980s and mid-1990s, respectively. A similar picture emerges from current account reforms. The time dynamics of trade reforms is more volatile but in all income groups the trend has been towards increased liberalisation, particularly since after the early 1980s.

The empirical analysis in the study consists in estimating and tracing out the average evolution of the public debt-to-GDP ratio in the aftermath of major policy changes. Jordás (2005) approach has been advocated by Auerbach and Gorodnichencko (2013) and Romer and Romer (2017), as a flexible alternative to vector auto-regression specifications since it does not impose dynamic restrictions.

Results in Figure 2 show the response of the debt-to-GDP ratio to major reform episodes — defined as a change in the reform indicator equivalent to 2 standard deviations of the annual change — and its associated 90 per cent confidence bands. Reforms contribute to lower the debt-to-GDP ratio in the medium term — that is, four to six years after the reform takes place. In particular, the medium-term debt effect of major reforms ranges between -2 percentage point (for trade reforms) and -4 percentage points (for domestic finance reforms). The effect is more precisely estimated for financial reforms. Moreover, conducting sub-sampling analysis revealed that while trade reforms have larger effects in advanced economies, financial reforms tend to have more significant effects in developing economies.

Figure 2. The effect of structural reforms on public debt (percent of GDP)

Note: Solid line denotes the public debt effect of reforms. Dotted lines indicate 90 per cent confidence interval based on standard errors clustered at country level.

In general, unconditional effects on the public debt stemming from reforms can be considered economically small. That said, allowing the dynamic response of debt to vary with its initial level reveals interesting findings. By means of applying an approach equivalent to Granger and Teravistra´s (1993), smooth transition auto-regressive model, we observed that financial and product market reforms increased debt for low indebtedness levels, but decreased it if prior to enacting a reform, countries were characterised by high indebtedness. In the case of trade reforms, these had the largest impact (in terms of decreasing public debt) at low initial indebtedness levels.

All in all, the findings in the paper are consistently robust to the inclusion of all reforms simultaneously and an instrumental variable approach, which uses political economy drivers of reforms as instruments (see Duval, Furceri and Miethe, 2018).

Note however that the empirical results should be treated with care: the set of structural reforms considered have often been accompanied by other fiscal and monetary measures that cannot be fully controlled for in the analysis. Moreover, the empirical estimates capture the average historical impact of major reforms on a proxy of fiscal sustainability. As such, they do not explicitly account for inherent uncertainty and cross-country heterogeneity regarding key variables (for example, fiscal multipliers, government funding costs, etc.). Furthermore, our empirical analysis of the impact of structural reforms on fiscal sustainability suffers from an inevitable problem of self-selection bias: the reforms observed are only those that have not been blocked in the political process, that is, many reform projects may have been blocked exactly because of their (short-term direct) budgetary impact, but the analysis does not take that into account. All in all, while some generalisations can be made in what concerns the link between structural reforms and fiscal sustainability in the short to medium term, caution is warranted, as there is no one size fits all.

♣♣♣

Notes:

- This blog post is based on the authors’ chapter, which is forthcoming in N. Campos, P. De Grauwe and Y. Ji (eds.), Economic Growth and Structural Reforms in Europe, Cambridge University Press.

- The post expresses the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by Yuri Catalano on Unsplash

- When you leave a comment, you’re agreeing to our Comment Policy

Davide Furceri is currently mission chief for Brunei in the Asia Pacific department of the IMF. Before that he was deputy division chief of the development macroeconomic division in the IMF´s research department. Prior to joining the Fund, he was an economist at the fiscal policy division of the European Central Bank, and at the macroeconomic analysis division of the OECD economics department. He has published extensively in leading academic and policy-oriented journals on a wide range of topics in the area of macroeconomics, public finance, international macroeconomics and structural reforms. He holds a PhD in economics from the University of Illinois and University of Palermo.

Davide Furceri is currently mission chief for Brunei in the Asia Pacific department of the IMF. Before that he was deputy division chief of the development macroeconomic division in the IMF´s research department. Prior to joining the Fund, he was an economist at the fiscal policy division of the European Central Bank, and at the macroeconomic analysis division of the OECD economics department. He has published extensively in leading academic and policy-oriented journals on a wide range of topics in the area of macroeconomics, public finance, international macroeconomics and structural reforms. He holds a PhD in economics from the University of Illinois and University of Palermo.

João Tovar Jalles is an assistant professor of economics at University of Lisbon´s ISEG. Previously, he was a senior economist at the Portuguese Public Finance Council and before that he spent 5 years at the IMF. Before joining the Fund, João held economist positions at the OECD and at the ECB. Academically, he was an invited lecturer at Sciences Po and assistant professor at the University of Aberdeen. João´s main research areas include fiscal policy and public finance, assessment of forecasting performance, structural reforms, macro-financial linkages and energy economics. He has published more than 100 academic papers in refereed journals. João holds a Ph.D. in economics from the University of Cambridge.

João Tovar Jalles is an assistant professor of economics at University of Lisbon´s ISEG. Previously, he was a senior economist at the Portuguese Public Finance Council and before that he spent 5 years at the IMF. Before joining the Fund, João held economist positions at the OECD and at the ECB. Academically, he was an invited lecturer at Sciences Po and assistant professor at the University of Aberdeen. João´s main research areas include fiscal policy and public finance, assessment of forecasting performance, structural reforms, macro-financial linkages and energy economics. He has published more than 100 academic papers in refereed journals. João holds a Ph.D. in economics from the University of Cambridge.