Climate change has shifted from a fringe issue to a worldwide emergency. Our understanding of the phenomena and our willingness to act have developed significantly, in part paralleling the ways in which climate change is being experienced around the globe.

Carbon pricing policy tools (both fiscal taxes and market permits) have been promoted as the core policy tools in mitigating greenhouse gas (GHG) emissions and in engendering sustainable economic growth. Substantial research and numerous analyses indicate that a carbon tax wedge helps reduce GHG emissions, thus effectively mitigating climate change.

The introduction of carbon fiscal policies in the EU economic area, for example EU ETS, has shown that green-friendly regulation leads to substantial drops in emission intensity levels (i.e. low emission-to-output ratio).

Despite the encouraging trends in emission intensity levels, the efforts in emissions reduction remain insufficient. Pushing for higher carbon taxes may prove to be extremely difficult with both politically and economically undesirable effects. As more reduction efforts are needed to better mitigate the potential catastrophic impacts of climate change, fiscal policy alone may not fill the inefficiency gap.

While the need for different and additional intervention is becoming acute, the role that other policies could play in mitigating climate change—especially short and medium-term policies, such as monetary and macroprudential ones—remain understudied. We show how it is relevant for monetary and macroprudential authorities to intervene in the current push for climate change mitigation strategies.

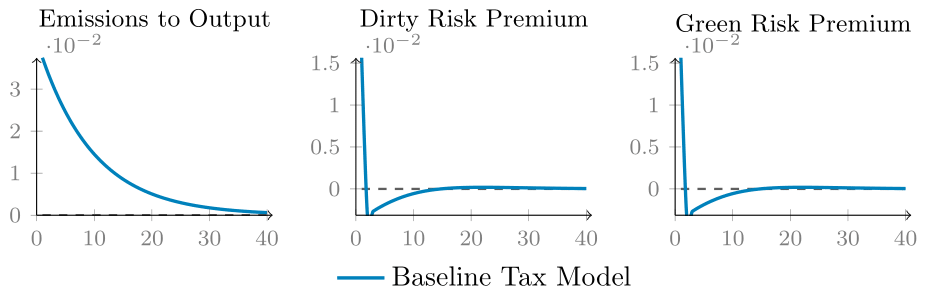

While scholars mostly agree that fiscal policy targeting carbon emissions is able at least theoretically to close the inefficiency gap induced by the environmental externality (greenhouse gas emissions), the political feasibility, the welfare impacts, and the role monetary and macroprudential authorities could play all remain under debate. Climate change is considered a long-term challenge, thus the inefficiency it introduces is not perceived to have an impact on short-term monetary policies. However, a small increase in emission intensity—due to, for example the US withdrawal from the Paris Agreement or potential Covid-19 macroeconomic consequences as argued by Hepburn et al. (2020)—is shown to increase the risk premium (Figure 1), which in turn has the potential to alter monetary policy transmission.

Figure 1. Effect of a negative abatement shock on the spread in an economy with no macroprudential rule – percentage deviations from steady state

Our approach offers new insight on the use of two central financial and monetary policy tools, namely macroprudential and quantitative easing (QE), to allow for the closing of the inefficiency gap induced by climate change, which we show is not achieved by fiscal policy alone.

Within our framework there are trade-offs between maximising output and consumption and reducing the impact of the economy on climate change. In particular, we find that a 10 per cent environmental tax (as percentage of output) is needed in order to be aligned with the Paris Agreement targets. However, this tax heavily depends on the efficiency of emission abatement levels (i.e. low transition cost) and is found to have potential distortionary effects on the welfare at least in the short-term, as the effects of climate change are perceived to be medium to long-term, thus making it difficult to capture all the benefits such taxes would yield in the short-term.

Furthermore, as highlighted in the IPCC reports, in order to offset the negative effects of CO2 emissions, it might prove necessary that the efforts needed exceed those of the reduction targeted in our baseline scenario (10 per cent tax) and those pledged in the Paris Agreement. Moreover, as shown in Figure 1 above, climate change could have major impacts on risk premium levels, thus altering the monetary policy transmission, which suggests a monetary and/or macroprudential intervention.

By investigating the role monetary and macroprudential policies can play, we find that a macroprudential policy favourable to a ‘green’ sector (where a ‘green’ sector is defined as a sector with lower carbon intensity than the ‘dirty’ sector), boosts green capital and output, implying a lower emissions-to-output ratio. An example of this would be to lower the weights on green loans in regulatory constraints, which would give an incentive to banks to finance green firms rather than the dirty ones. Meanwhile, if a quantitative easing policy is favoured, we find that a carbon tax improves the benefits of both ‘green’ and ‘dirty’ asset purchases. However, macroprudential policy is needed to provide an incentive to central banks to engage in green QE, that is, purchasing bonds of green businesses. Choosing between dirty and green QE then implies a trade-off between higher output and lower emissions. This trade-off would disappear in the event that the green sector grows enough to be as big as or bigger than the dirty sector.

Since the Rio Conference in 1992, a debate has raged in academic and political circles over the growth-environment trade-off. Discussions focus on the means by which economic activities could align with environmental concerns instead of being hindered by assumed mutual exclusivity. In practice, especially in the short and medium terms, however, financial and economic activity on one side, and environmental policy on the other, are in tension. A need for short-term policies aimed at bridging environmental quality and economic efficiency, as well as addressing financial stability, in order to foster economic sustainability, are in dire need. In this climate, so to speak, our research seeks to shed light on the role short-term policy tools could play in transitioning to a greener economy.

♣♣♣

Notes:

- This blog post is based on Policy interactions and the transition to clean technology, Working Paper 337 of LSE’s Grantham Research Institute on Climate Change and the Environment.

- The post expresses the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by Anne Nygård on Unsplash

- When you leave a comment, you’re agreeing to our Comment Policy

Ghassane Benmir is a PhD researcher at the LSE. His research interests span macroeconomics, monetary economics, asset pricing theory, and climate change economics.

Ghassane Benmir is a PhD researcher at the LSE. His research interests span macroeconomics, monetary economics, asset pricing theory, and climate change economics.

Josselin Roman is a PhD researcher at PSL Research University – Paris Dauphine. His research interests span macroeconomics, monetary economics, financial economics, and climate change economics.

Josselin Roman is a PhD researcher at PSL Research University – Paris Dauphine. His research interests span macroeconomics, monetary economics, financial economics, and climate change economics.

This article is much appreciated. MayI suggest that the more progressive economists at the LSE consider looking at a proposal called “Carbon Quantitative Easing” or CQE. CQE is not the same a Green QE, but it is a proposed kind of QE that at least three fundamentally new features: (1) it involves asset purchases of a new carbon currency, that is coupled to mitigated carbon, and as such CQE will invoke the direct purchase of mitigated carbon by central banks—or at least the promise of buying the mitigated carbon; (2) CQE does not actually require much in the way of central bank purchases, because the carbon currency will behave as a financial asset, and thus CQE will transfer private wealth into climate mitigation; (3) CQE supports a new market-based policy for carbon rewards that can tackle the various factors of the Kaya Identity and carbon removal at speed and scale; and (4) the framework of the CQE approach is consistent with a need to manage systemic risks from within the economy (endogenous) and without the economy (exogenous). A justification is available based on an expanded theory for market externalities that points to new mandates for central banks. The new mandate for central banks is to provide a floor price guarantee for the carbon currency, and thus provide scalable climate finance for the mitigation of the climate crisis upstream of the financial system. Currently, central banks are stuck in a conceptual model that assumes that central banks should only address systemic risks in the financial system, and downstream of the climate crises and ecological crisis.