Why firms engage in corporate social responsibility (CSR) is widely debated, particularly in the context of the 2019 Business Roundtable statement by US chief executives, which redefined the purpose of a corporation as promoting an economy that serves not only shareholders but all stakeholders, including customers, employees, suppliers and communities. Despite these debates, there is surprisingly little direct evidence of the motivations for firms to engage in CSR. One school of thought argues that CSR is an investment in the long-term reputation of the firm, driven by considerations such as preferences of customers and other stakeholders. An alternative view is that managers use CSR for their own benefit, even if it is wasteful for the company.

In our research we use product-wise exports of Indian companies to different countries to examine whether socially responsible practices are transmitted through international trade. We examine Indian companies’ CSR expenses following exogenous export-shocks to the stakeholder preference for CSR. We hypothesise that positive demand shocks from export markets with a higher stakeholder preference for corporate social practices will be associated with an increase in affected firms’ CSR expenses. In contrast, similar shocks from countries with a lower stakeholder preference for corporate social practices should not affect the CSR expenses.

This set up also allows us to examine the motives for incurring CSR expenses. If Indian companies increase CSR expenses depending on the stakeholder preference to gain a larger share of the export market, it will imply an investment motive. On the other hand, if CSR expenses increase, irrespective of the stakeholder preference in the export market, it will suggest that managers undertake these expenses for their own benefits. For a sample of large Indian firms in the period 2006-2012, we use product-level information from the Global Antidumping Database on antidumping against Chinese exporters to examine how competing Indian exporters of the same product adjust their CSR expenses. Antidumping is known to negatively (positively) affect exports of targeted (competing) country’s exporters.

We use an example from our data to highlight the effect of antidumping on exports. PET-products exported by Chinese firms faced antidumping investigations in 2004 by the US. Figure 1 shows that the Chinese exports of PET-products were double that of Indian exports in the pre-2004 period. After 2004, Indian exports of PET to the US overtook China’s, doubling that of Chinese exports by 2008.

Figure 1. Indian and Chinese exports of PET products to the U.S

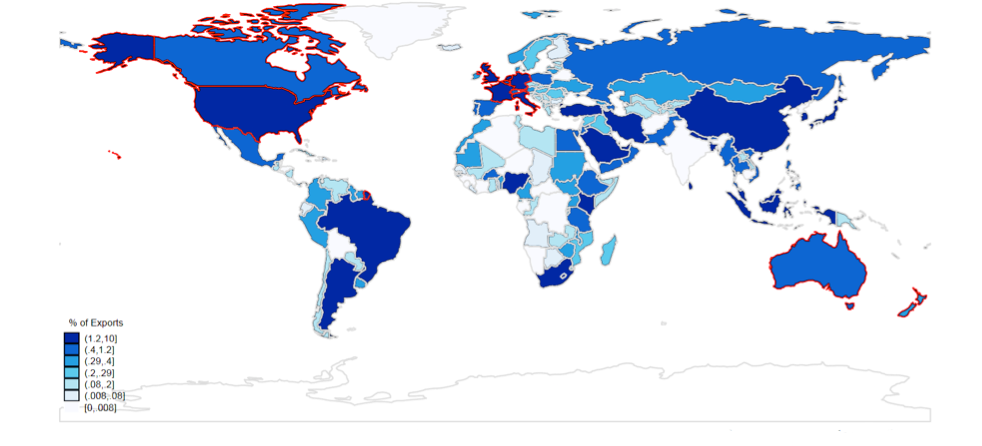

To test our central hypothesis that the CSR response to the export shock will vary with the level of stakeholder preference for corporate philanthropy, we group the main export destinations of Indian firms by stakeholder preference for CSR. We use the 2010 World Giving Index to classify the stakeholder preference for corporate philanthropy. We classify countries with a higher rank, such as the US (rank 5) and the EU (the UK ranked 8th, the Netherlands 7th, and Germany 18th), as countries with a high stakeholder preference (high preference) for CSR. India’s other largest export destinations with lower ranks in the index (UAE ranked 50th, Mexico 67th, Brazil and South Africa 76th) are classified as countries with a low preference for CSR (low preference). Figure 2 shows the variations in stakeholder preference for CSR among India’s main export destinations.

Figure 2. Customer preference for corporate philanthropy in India’s export markets

Note: Red borders indicate geographies with high customer preference for corporate philanthropy.

Using a difference-in-difference setup, we find that Indian firms affected by antidumping against competing Chinese products from high preference countries increase CSR expenses in subsequent years. However, there is no statistically significant effect on CSR for Indian firms affected by antidumping initiations on Chinese products from low preference countries. The impact on Indian firms’ CSR expenses of antidumping measures imposed on Chinese products is economically meaningful; affected Indian firms increased CSR expenses by 20% in the period following the antidumping investigation of competing Chinese products. Additionally, we find that Indian firms increase large capital expenditure and R&D expenses in response to antidumping measures on Chinese products from both high– and low preference countries. Finally, we find that increased CSR expenses in response to antidumping shocks from high preference countries gain in value, compared to firms that do not increase CSR expenses in similar situations. In contrast, firms that increase CSR expenses when faced with antidumping shocks from low preference countries lose value compared to firms that do not increase CSR expenses in similar situations.

An advantage of our approach is that, even if alternative explanations are plausible for individual results, it is difficult to offer one alternative explanation consistent with all of our results. For example, it can be argued that better export prospects (or the anticipation thereof) can induce managers to spend more on CSR projects, even if it reduces profitability. Such an explanation does not explain why CSR expenses do not increase when A.D. measures on Chinese products are initiated from low preference countries. Additionally, concerns about the relatively more important role the US and the EU play as export markets for Indian products do not explain the increase in Indian firms’ capital expenditure and research and development when antidumping shocks originate from low preference countries.

Overall, our results are consistent with the investment motive of CSR and highlight that socially responsible practices are transmitted through international trade. Companies in emerging market countries, such as India, use CSR as strategic investments to cater to stakeholder preference in the export markets.

♣♣♣

Notes:

- This blog post is based on Trade Shocks and the Role of Stakeholder Preference in Corporate Social Responsibility.

- The post expresses the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by chuttersnap on Unsplash

- When you leave a comment, you’re agreeing to our Comment Policy

Shantanu Banerjee is a professor of finance at Lancaster University. His main research area is empirical corporate finance, with a focus on investment decisions, financing choice, product market strategy, IPO, bankruptcy, executive compensation, and corporate social responsibility.

Shantanu Banerjee is a professor of finance at Lancaster University. His main research area is empirical corporate finance, with a focus on investment decisions, financing choice, product market strategy, IPO, bankruptcy, executive compensation, and corporate social responsibility.

Swarnodeep Homroy is an assistant professor at the University of Groningen. He received a PhD in economics from the University of Lancaster. His main research areas are corporate finance, political economy and the economics of gender.

Swarnodeep Homroy is an assistant professor at the University of Groningen. He received a PhD in economics from the University of Lancaster. His main research areas are corporate finance, political economy and the economics of gender.

Aurélie Slechten is an assistant professor in economics at Lancaster University. She holds a PhD in economics from the Université Libre de Bruxelles. Her main research interests are environmental economics, microeconomics and market design.

Aurélie Slechten is an assistant professor in economics at Lancaster University. She holds a PhD in economics from the Université Libre de Bruxelles. Her main research interests are environmental economics, microeconomics and market design.