Judgment and reporting of a company’s ability as a going concern (a company that has the resources needed to continue operating indefinitely until it provides evidence to the contrary) have become one of the major focuses of standard setters in both US and UK in recent years (for example, FASB 2014-15, IAASB 2015, PCAOB 2017). During difficult times such as the 2008 financial crisis and the recent pandemic, it became very relevant as more firms are subject to substantial doubt regarding their ability to continue as a going concern.

Audit reports provide third-party certification of a company’s overall financial situation. If a company’s continued survival is in doubt, an auditor issues a separate note in the report reflecting the doubt, and this is commonly referred to as a going concern audit opinion. From the market participants’ view, as auditors have unique access to their clients’ business, a going concern opinion provides useful new information to the market. However, there is no universal criterion for auditors’ evaluation standards. The severity of the doubt and the possibility of recovery depend on auditors’ assessment. There is mixed evidence regarding the market reaction to going concern disclosures, and uncertainty persists regarding whether firms with going concern opinions may fail versus endure.

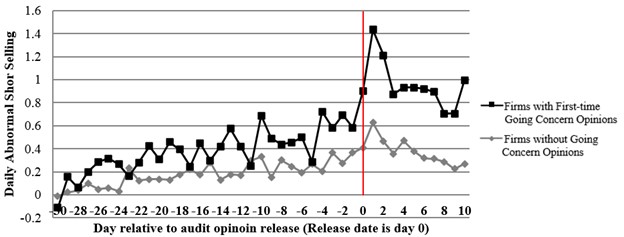

In a forthcoming paper, we investigate going concern opinions based on the trading of some well-documented sophisticated investors—short sellers. The market reaction can be affected by investor sophistication. Short sellers are regarded as “informed” investors in capital markets. In Figure 1, we show that short sellers view going concern opinions as informative negative news and the level of short selling increases sharply in the days leading to going concern disclosures, especially during the nearest five days; and the shorting reaches its peak in the two days immediately following the release.

Figure 1. Short selling around audit opinion release

Next, we investigate the trading pattern to understand whether short sellers take advantage of private information, or make a better interpretation of readily available public information. First, we find that the increase in short sales concentrates in a very narrow window (five days) immediately before disclosures, which implies that short sellers have at least some private information on the imminent going concern announcement. Otherwise, the increase in the shorting would be distributed more evenly over time. Second, we decompose short selling into expected versus unexpected components. We measure the expected short sales based on public information and find that this expected short selling has predictive power on the occurrence of going concern disclosures. This finding supports that short sellers process public information and implement it in trading. Therefore, it suggests that short selling reflects both the privately informed trading and the processing of public information by short sellers.

Finally, we investigate the relation between the pre-going-concern-announcement short selling and the post-announcement market reaction. If short sellers are sophisticated enough and unconstrained, they should be able to not only predict an impending event, but also trade based on the severity of the event and profit by shorting more heavily on companies with a greater post-announcement return decline. We find a significant negative association between pre-announcement abnormal short selling and post-announcement returns in the high-priced subsample; but such negative relation is missing in the low-priced subsample. It appears that short sellers predict the adverse news in low-priced firms but do not incorporate efficiently to the degree of market reaction of going concern disclosures. This is consistent with the view that low-priced stocks suffer from high transaction costs in the equity loan market, and thus becomes the major short selling constraint.

Our research adds to the understanding of how the market processes going concern opinions based on the trading of a group of well-documented “sophisticated” investors—short sellers. We also provide insights into the information sources of short sellers. We show that short sellers benefit from both private and public information. The finding contributes to both the accounting practitioners by documenting the availability of private accounting information to a group of investors before such information is released to the public. The group of investors can take advantage of private information, and front-run other participants in the capital market. Meanwhile, we show consistent evidence that short sellers are constrained to impound the severity of the negative information effectively. Due to such constraints, the degree of short selling prior to going-concern-announcement is not aligned with post-announcement price declines in the short run, which potentially leads to long-run price drift.

♣♣♣

Notes:

- This blog post is based on Short Sale Prior to Going Concern Disclosures, forthcoming in Accounting and Business Research.

- The post expresses the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by Jamie Street on Unsplash

- When you leave a comment, you’re agreeing to our Comment Policy

Jian Huang is an associate professor of finance at Towson University. Prior to joining TU, he taught at the University of Kansas where he also obtained a Ph.D. in Finance. His research involves corporate finance and investments, with more than 10 refereed journal articles to his credit.

Jian Huang is an associate professor of finance at Towson University. Prior to joining TU, he taught at the University of Kansas where he also obtained a Ph.D. in Finance. His research involves corporate finance and investments, with more than 10 refereed journal articles to his credit.

Lei Wang is a professor in Finance at Shanghai University of International Business and Economics. He received his Ph.D. degree from Xiamen University. His research interests include empirical asset pricing, behavioural finance, and market microstructure.

Lei Wang is a professor in Finance at Shanghai University of International Business and Economics. He received his Ph.D. degree from Xiamen University. His research interests include empirical asset pricing, behavioural finance, and market microstructure.

Han Yu is an associate professor of finance at Southern Connecticut State University. She holds a Ph.D. in finance from the University of Kansas. Her research interests span corporate finance, corporate governance, financial accounting, and asset pricing.

Han Yu is an associate professor of finance at Southern Connecticut State University. She holds a Ph.D. in finance from the University of Kansas. Her research interests span corporate finance, corporate governance, financial accounting, and asset pricing.

Zhen Zhang is an assistant professor of accounting at Towson University, Towson, MD. She holds a Ph.D. from Georgia State University, Atlanta. She worked in public accounting and had a Master of Accounting and a Master of Taxation before her Ph.D. study. Her research focuses on organisational behaviour. She works on managerial and financial accounting studies using archival or experimental methods.

Zhen Zhang is an assistant professor of accounting at Towson University, Towson, MD. She holds a Ph.D. from Georgia State University, Atlanta. She worked in public accounting and had a Master of Accounting and a Master of Taxation before her Ph.D. study. Her research focuses on organisational behaviour. She works on managerial and financial accounting studies using archival or experimental methods.