During the COVID crisis, governments around the world have been wondering how to expediently put money in the hands of millions of struggling firms. In an earlier post, we have suggested that one possible way to achieve this goal is for governments to timely pay all receipts due. Paying the private sector on time for work already done is not just about having cash on hand. It also prevents companies from taking up further debt in order to survive. The evidence is clear: the faster the government pays its dues, the fewer firms need a loan.

However, speed is not always characteristic of the public sector when it comes to paying bills. Data from Bosio et al. (2020) show that procuring entities take on average 14 weeks (about 100 days) to process the final payment for public works contracts. Delays vary broadly across countries, from 48 days in Azerbaijan to 760 days in São Tomé and Príncipe. For example, in Angola, it takes on average 180 days for a business to receive final payment from the government. In Guinea, it takes on average 365 days. Only about 28% of countries pay contractors within 45 days from the completion of works.

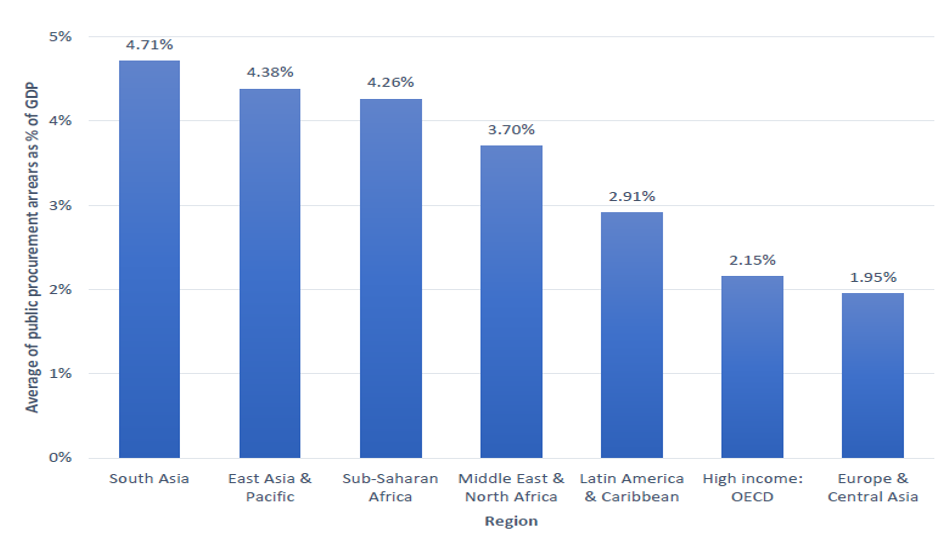

In earlier research, we calculate the size of the accounts payables for countries that delay their payments on completed public procurement projects beyond 45 days. The figure is a staggering $4.65 trillion. This leads to considerable government arrears. We use data on the share of procurement to GDP and data on the average payment time of government invoices to calculate the size of arrears beyond 45 days. Average public procurement arrears as a percentage of GDP in countries processing procurement payments in more than 45 days is 3.39 percent. South Asia, East Asia and the Pacific, and Sub-Saharan Africa are the top three regions with the largest arrears, at 4.71, 4.38, and 4.26 percent respectively. OECD High Income and Europe and Central Asia are those with the lowest, at 2.15 and 1.95 percent respectively (Figure 1).

Figure 1: Average government arrears as % of GDP by region in countries processing procurement payments in more than 45 days

Sources: Nationally reported official government statistics, Bosio et al., 2020a, World Development Indicators GDP (current US$) database, OECD Public Procurement Expenditure database, World Bank’s Global Public Procurement database and other sources. Note: The sample includes 38 countries from Sub-Saharan Africa, 6 countries from South Asia, 6 from East Asia & Pacific, 13 from Middle East

Many countries have tried to incentivise prompt payment of government invoices by introducing penalties for overdues in their procurement law. For the majority of countries, late payments are penalised at the prevailing interest rate for commercial borrowing, specified either at time of occurrence (Namibia), the mid-point of the delay period (Kenya and Tajikistan), the first day of calendar half-year (Hungary), or on the date of contract signing (Tanzania). Occasionally, the penalty interest rate can be specified in the contract itself (Afghanistan, Nigeria, Romania, the Russia Federation and Sierra Leone, for example). Other countries impose a flat interest rate. In Japan, for example, the penalty interest is levied at a 5% per annum rate. That penalty rate is 7% in Oman and 10% in Bhutan. Finally, in Belarus the late payment penalty rate is 0.2% of the overdue payment compounded for each day of delay.

Such incentives, however, have seldom worked, as penalties are rarely paid in practice. Companies may fear it would make it more difficult to win other contracts in the future and typically forego the additional payment. Instead, we propose to automatically fold the overdue interest payments into tax credits after a 3- or 6-month payment delay. Such a step will provide incentive for governments to pay on time, as well as for companies to improve tax reporting. Tax authorities would also benefit from this process as oftentimes they are unaware of the size of overdues that weigh on government coffers.

As a broader step, governments running large overdues to their businesses can issue bonds that cover these overdues, thus putting fresh money in the economy and spurring much-needed economic growth. Such ‘recovery’ bond offerings can be prepared with the help of regional and multilateral development banks to ensure investor interest. With the significant liquidity available in the global financial system due to expansionary monetary policy to fight COVID, timing is propitious for such an initiative.

♣♣♣

Notes:

- This blog post expresses the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by Photo by Erik Mclean on Unsplash

- When you leave a comment, you’re agreeing to our Comment Policy

Erica Bosio is a researcher at the World Bank Group, where her work focuses on public procurement. Previously, she worked in the arbitration and litigation department of Cleary Gottlieb Steen & Hamilton in Milan. She holds a Master of Laws from Georgetown University and a degree in law from the University of Turin (Italy).

Erica Bosio is a researcher at the World Bank Group, where her work focuses on public procurement. Previously, she worked in the arbitration and litigation department of Cleary Gottlieb Steen & Hamilton in Milan. She holds a Master of Laws from Georgetown University and a degree in law from the University of Turin (Italy).

Greta Polo is a private sector development analyst at the World Bank. She holds a master’s degree from Columbia University and a B.S. in applied mathematics from the Florida Institute of Technology.

Greta Polo is a private sector development analyst at the World Bank. She holds a master’s degree from Columbia University and a B.S. in applied mathematics from the Florida Institute of Technology.

Vinay Sharma is global director of solutions and innovations in procurement at the World Bank’s governance global practice.

Vinay Sharma is global director of solutions and innovations in procurement at the World Bank’s governance global practice.