How would leaving the EU affect the UK’s economy? Gianmarco Ottaviano, João Paulo Pessoa, Thomas Sampson and John Van Reenen outline findings from a new report on the economic consequences of a ‘Brexit’. They indicate that if the UK left the European Union there would likely be a significant negative impact on the economy, with the most important cost emerging as a result of lower trade with the EU due to greater non-tariff trade barriers.

Since a speech by the Prime Minister in January 2013, the Conservative party has been committed to holding a referendum on the UK’s membership of the European Union (EU) in 2017. So what would be the consequences of a majority vote in favour of leaving? Our new report finds that so-called ‘Brexit’ is likely to have a significant negative impact on the UK economy.

Eurosceptics emphasise greater national sovereignty from leaving the EU, while Europhiles talk about the longstanding benefits of ever closer unity to reduce the risks of military conflict. These are important considerations, but our work focuses on the more mundane (but quantifiable) economic effects of Brexit.

Leaving the EU would bring home about half a percentage point of national income, since the UK would transfer fewer resources to subsidise poorer EU members. This would be the main economic benefit of Brexit. The most important cost would be lower trade with the EU. Higher trade barriers would reduce the UK’s ability to specialise in industries where it has a comparative advantage, leading to a fall in income. Our analysis uses a state-of-the-art quantitative model of international trade to estimate the effects of Brexit on trade and quantify the consequences for national income.

Estimating the effects of Brexit on trade and national income

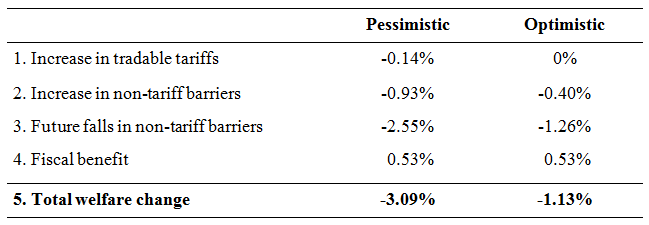

It is not known what relationship the UK would have with the EU following Brexit, so we consider two scenarios: an optimistic scenario in which the UK continues to have relatively easy access to EU markets; and a pessimistic scenario with higher trade barriers. In the pessimistic scenario, we assume that there will be some tariffs on UK-EU goods trade. This seems reasonable immediately following withdrawal, but some argue that the UK may be able to negotiate a better tariff deal in the medium term. Hence, in our optimistic scenario, we assume tariffs continue to be zero.

Another important source of trade costs lies in non-tariff barriers such as regulations and other legal obstacles that affect not only goods but also services trade. Nowadays, such barriers are more important than tariffs in most developed economies. In fact, the main goal of the proposed Transatlantic Trade and Investment Partnership between the EU and the United States is to reduce non-tariff barriers. In our analysis, we assume that such barriers would increase after Brexit, with a larger rise in the pessimistic case than in the optimistic one.

Finally, intra-EU trade costs have been steadily falling over time – approximately 40 per cent faster than in other OECD countries. A decade from now, non-tariff barriers inside the EU are likely to be smaller and the UK would not reap these benefits after Brexit. In our pessimistic scenario, we assume that such barriers continue to fall 40 per cent faster than in the rest of the world, while in the optimistic case, we assume that intra-EU barriers fall only 20 per cent faster, implying that the UK has less to lose in the event of Brexit.

Taking account of all these effects, we find that Brexit would decrease UK income by 1.13 per cent in the optimistic case and 3.09 per cent in the pessimistic case. Thus, the costs of lower trade far outweigh the fiscal savings. Most of the impact comes from changes in non-tariff barriers, which are particularly important in services where the UK is a major exporter. In cash terms, the loss is £50 billion in the pessimistic scenario and a still substantial £18 billion in the optimistic one. These findings are illustrated in the Table below.

Table: Welfare changes in the UK if the UK leaves the EU (static model)

Note: Welfare measured by change in real consumption in the UK Source: Ottaviano, Pessoa, Sampson and Van Reenen (2014)

Growth

But the numbers in the Table above underestimate the costs of Brexit as they do not consider other consequences of reduced trade that are likely to reduce income, but are harder to quantify numerically. In particular, they do not allow for the ‘dynamic’ effects of trade on growth, boosting productivity via more competition, innovation and adoption of technologies.

Using a different approach that factors in more realistic dynamic losses from lower productivity growth, a conservative estimate would double losses to 2.2 per cent of GDP even in the most optimistic case. In the pessimistic case, there would be income falls of 6.3 per cent to 9.5 per cent of GDP. These estimates are much higher than the costs obtained from the static trade model, implying that the dynamic gains from trade are important. To put these numbers in perspective, during the 2008/09 global financial crisis, the UK’s GDP fell by around 7 per cent.

Other economic effects: regulation, immigration, foreign direct investment

Brexit will not only affect trade, but also foreign direct investment (FDI), immigration and new regulations. The UK received the most FDI of any European country in 2011, and was second only to the United States in terms of the stock of inward FDI around the world. Part of the attraction is as an export platform to the rest of the EU, so if the UK is outside the trading bloc, this position is likely to be threatened. This matters because foreign multinationals tend to be high productivity firms and they bring new technologies and management skills with them.

Outside the EU, the UK could restrict immigration from the rest of the EU and vice versa. In economic terms, migratory flows act much like trade as people tend to move to where they can be more productive and earn higher incomes. Studies find that restricting mobility will, just like restricting trade, reduce UK overall welfare. Moreover, other evidence suggests that there have been no negative effects on jobs and wages of native Britons from waves of EU immigration. So even on distributional grounds, immigration does not seem to have been damaging.

Currently, the UK is able to influence the regulations governing the EU single market. Even if the UK maintained full access to the single market, it would be in the same situation as Switzerland: UK exports would have to follow these regulations without being party to setting them.

In sum, our current assessment is that leaving the EU would be likely to impose substantial costs on the UK economy and would be a very risky gamble. The dream of splendid isolation may turn out to be a very costly one indeed.

For more details see the authors’ full report, ‘Brexit or Fixit? The Trade and Welfare Effects of Leaving the European Union’

Please read our comments policy before commenting.

Note: This article originally appeared at our sister site, British Politics and Policy at LSE, and gives the views of the author, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/Rb1WoA

_________________________________

Gianmarco Ottaviano – LSE

Gianmarco Ottaviano – LSE

Gianmarco Ottaviano is Professor of Economics at the London School of Economics and Globalisation Research Programme Associate at the Centre for Economic Performance.

João Paulo Pessoa – LSE

João Paulo Pessoa – LSE

João Paulo Pessoa is an occasional research assistant in CEP’s productivity and innovation programme. He started his MRes/PhD in economics at LSE in 2009. Before coming to LSE he worked as a financial products analyst for three years at BBM Bank.

Thomas Sampson – LSE

Thomas Sampson – LSE

Thomas Sampson is a Lecturer in Economics at the London School of Economics. Globalisation Research Programme Associate at the Centre for Economic Performance.

John Van Reenen – LSE

John Van Reenen – LSE

John Van Reenen is Professor in the Department of Economics London School of Economics and the Director Centre for Economic Performance, London School of Economics. He is also Fellow of the British Academy, Econometric Society and the Society of Labour Economists.

Absolute tut, the EU is a plague! it is spreading like an incurable cancer that needs to be cut off point blank like a gangrene limb instead of having EU subsidy junkies leeching off us on a continuous basis. The UK was a net contributor to the EU budget from day one even when we were on an IMF program in the 1970’s with our lights going out & the nation working 3 day weeks because we had no power. Its time these subsidy junkies got off their backsides & made something of themselves. The only time the EU takes notice of the UK is when they need our military & then suddenly we are on even the Polish leaders Christmas card list

I really don’t understand where this desire to reduce everything down to the EU budget comes from. Our net budget contributions aren’t even half a percent of GDP and they’re factored directly into the analysis here. Yet you’re writing a study like this off on the basis that we make a net contribution to the budget.

That doesn’t make even the slightest bit of sense – it’s a bit like quitting your £40,000 a year job because you don’t like paying the train fare into the office. If something benefits our economy then it benefits our economy – it doesn’t matter why or how, it is what it is. If we want to live in the real world then it requires accepting facts, even when they don’t match your agenda.

Well we could start with everyone else being net contributors instead of being leeches & as to saying its like quitting your job because you dont like the bus fare is quite wrong, its more like quitting going to the casino or betting shop to lose your money. You might not have noticed we lose money every year with EU trade because even after 40 years of trying to get services included in the single market & giving up a substantial lump of our rebate to grease the wheels we still are kept out of the markets that matter.

This study seems to miss another set of potentially larger economic impacts, which might be positive or negative for the UK economy: namely the freedom to follow economic and social policies and negotiate trade deals on its on behalf, and behavioural changes, such as a less Eurocentric focus on our exports and trade partnerships, which might increase our attention to faster growing markets. In short, this seems to be a very narrowly-focussed study, with concomitantly limited value in predicting the true total costs or benefits of leaving the EU.

“Moreover, other evidence suggests that there have been no negative effects on jobs and wages of native Britons from waves of EU immigration. So even on distributional grounds, immigration does not seem to have been damaging.”

A very interesting and informative analysis but I wish the author could have gone into more detail regarding the sentences above. I would like to know what evidence supports no negative impact. I thought it was a given that increased immigration drove down wages, especially among low skilled jobs due to supply and demand. Surely an increased supply of cheap labour is going to drive down wages? Isn’t this an economic basic? I would be very interested in seeing the evidence that refutes this.