What effect has the financial crisis had on pension systems in EU countries? Aaron G. Grech notes that prior to the crisis there was a significant divergence in pensions across the EU, with some states having relatively generous systems in comparison to others. He writes that following the crisis, southern European states have had to substantially cut back on pensions, while other states in northern Europe have remained relatively unscathed. He argues that although it should still be possible for these systems to keep pensioners out of poverty, European policymakers will need to ensure a properly functioning labour market that provides opportunities for young Europeans.

What effect has the financial crisis had on pension systems in EU countries? Aaron G. Grech notes that prior to the crisis there was a significant divergence in pensions across the EU, with some states having relatively generous systems in comparison to others. He writes that following the crisis, southern European states have had to substantially cut back on pensions, while other states in northern Europe have remained relatively unscathed. He argues that although it should still be possible for these systems to keep pensioners out of poverty, European policymakers will need to ensure a properly functioning labour market that provides opportunities for young Europeans.

While EU countries entered the financial crisis with very different pension systems, the crisis has enhanced convergence, at least in two aspects. Eastern European countries which had sought to lessen the role of the state and set up mandatory private pensions ended up unwinding most of these reforms. Meanwhile, Southern European countries which traditionally had relatively generous state pension schemes cut them back.

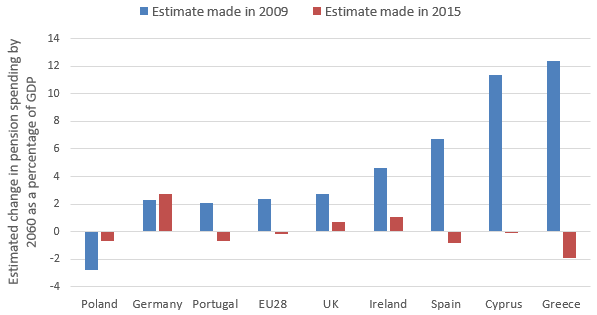

The European Commission’s 2015 Ageing Report suggests that despite a doubling of the dependency ratio, pension spending in the EU will decline by 0.2 per cent of GDP by 2060. A comparison with the projections made in 2009 shows that those countries least affected by the crisis, such as Poland and Germany, have had an upward revision in their spending projections. Conversely, those economies that were severely affected have made substantial cuts. For instance, instead of rising by 12 per cent of GDP by 2060, as had been projected in 2009, in Greece pension spending is now forecast to decline by 2 per cent. Chart 1 below illustrates changes in estimated future pension spending in selected countries since the crisis.

Chart 1: Estimated change in pension spending by 2060 as a percentage of GDP in selected countries

Note: For more information, see the author’s recent paper in the International Social Security Review.

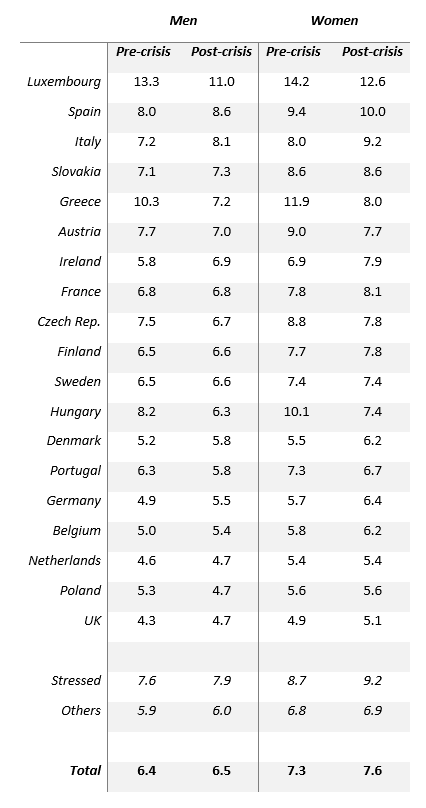

The reduction in projected spending implies lower generosity and adequacy of state pensions. The OECD’s Pensions at a Glance report includes estimates of pension wealth (i.e. total pension flows during retirement as a multiple of the average wage). These estimates can be compared with estimates made before the crisis in 19 EU countries (comprising 92 per cent of the EU’s population). Since state pensions are of key importance to those with low-to-average incomes, it is best to focus on estimates for those in that part of the wage distribution. Besides showing results for individual countries, Table 1 also shows figures (weighted by population size) for the group of ‘stressed’ countries most affected by the sovereign debt crisis, Greece, Ireland, Italy, Portugal and Spain.

Table 1: Pension wealth for men and women in the bottom half of the wage distribution before and after the crisis

Source: OECD

On the face of it, the crisis appears not to have weakened entitlements substantially. Even in stressed countries, pension wealth appears to be higher. Pension entitlements fell in just seven countries, with the largest falls in Greece. Meanwhile, the five biggest nations boosted generosity.

Eurostat data on the proportion of elderly poor indicate that the latter in stressed economies are 14 per cent of men and 17 per cent of women, in comparison to 11 per cent and 15 per cent, respectively, in the non-stressed economies. Yet, Table 1 implies that pension generosity is higher in stressed countries. This paradox is explained by the fact that pension wealth estimates assume individuals have a 40-year career. However, only men in Denmark, the Netherlands, Sweden and the UK work this long. The average Greek and Italian man works 35 years whilst, on average, women in Italy and Greece have a 25 and 28 year career, respectively.

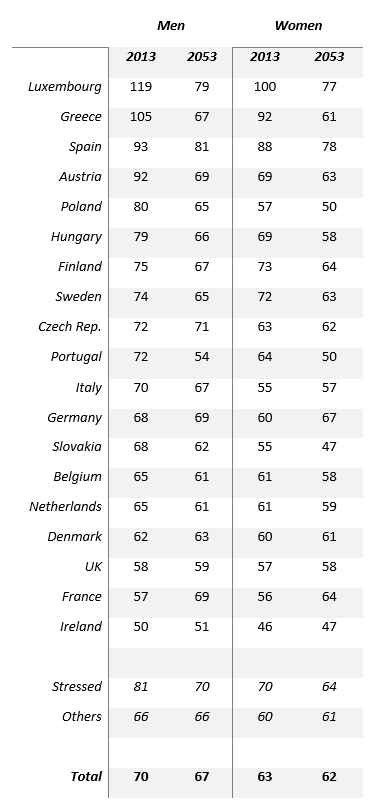

Since reforms have tightened the link between entitlements and career length, estimates such as those in Table 1 are deceptive. To address this, it is possible to compute alternative estimates using data on current and projected working lives, and convert the resulting pension wealth estimates as a proportion of the median disposable income in that country to benchmark the effective generosity of state pensions.

Table 2 suggests that whereas pension entitlements are now enough to sustain, on average across the EU, an income equal to 71 per cent of the median disposable income throughout retirement for men, over the coming decades this will fall to 67 per cent: still above the 60 per cent relative poverty threshold. Outcomes for women are less generous.

Table 2: Average annual pension benefits as a proportion of median income for men and women in the bottom half of the wage distribution

Note: For more information, see the author’s recent paper in the International Social Security Review.

The picture that emerges is that while Mediterranean countries tend to have generous systems on paper, due to limited labour participation, actual outcomes are not that rosy. Consequently, while today the Greek, Italian and Portuguese systems are more generous than the French and German ones, over the coming decades the situation could be reversed.

The financial crisis has led to increased convergence amongst countries, with the gap between the most and least generous pension systems more than halving. However, the crisis has led to increasingly different labour outcomes. Before the crisis the gap in unemployment rates between the country with the least unemployment and that with the highest stood at 8 percentage points. Now the gap is three times larger. The gap is even more worrying when looking at youth unemployment rates: 58 per cent in Greece against 8 per cent in Germany.

This development, combined with the tightening of the link between pension entitlements and contributory records introduced by recent reforms, poses serious risks for young generations’ future retirement incomes. This enhances the importance of policies, such as the youth guarantee, intended to increase employability and ease access to the labour market for the young. Now, more than ever before, European policymakers need to ensure a properly functioning labour market that provides opportunities to young Europeans.

Please read our comments policy before commenting.

Note: For more information on this topic, see the author’s recent paper in the International Social Security Review. This article gives the views of the author, not the position of EUROPP – European Politics and Policy, the London School of Economics, or the Central Bank of Malta. Featured image credit: Derek Mindler (CC-BY-SA-3.0)

Shortened URL for this post: http://bit.ly/1Mh8POe

_________________________________

Aaron G. Grech – LSE

Dr Aaron G. Grech is a Research Fellow at the London School of Economics in the Centre for the Analysis of Social Exclusion. He currently heads the Modelling and Research Department of the Central Bank of Malta.