Wages vary significantly across European countries, but would increasing wages to create more convergence in pay levels have a damaging impact on competitiveness? Drawing on the examples of the Czech Republic, Germany and Romania, Martin Myant argues that there is scope for raising wages in central and eastern European countries to draw closer to western European levels without generating negative economic side-effects.

Wages vary significantly across European countries, but would increasing wages to create more convergence in pay levels have a damaging impact on competitiveness? Drawing on the examples of the Czech Republic, Germany and Romania, Martin Myant argues that there is scope for raising wages in central and eastern European countries to draw closer to western European levels without generating negative economic side-effects.

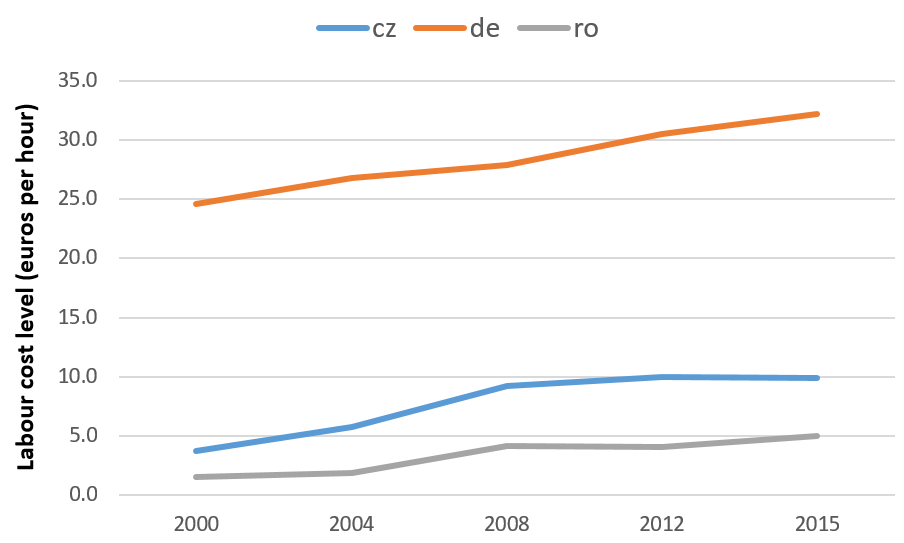

There are huge disparities in wage levels across the EU. As Figure 1 shows, the level in Romania in 2015 was about half that of Czechia, which was in turn less than one third the German level, with the gap actually increasing since 2008. Some differences in pay reflect different kinds of work, but gaps remain enormous even where work tasks are very similar. This applies across many familiar jobs, such as teachers, bus drivers, bar staff or car-assembly workers, for many of which workers can easily move between countries. It is not credible to suggest that German bus drivers take six times as many passengers, or German teachers handle six times as many students as their Romanian colleagues.

Figure 1: Labour cost levels in Germany, Czechia and Romania (euros per hour, 2000-15)

Source: Derived from Eurostat, tps00173

The European Commission and others have argued that such low pay levels are essential for maintaining international competitiveness, a term given apparent numerical precision in the measure of ‘unit labour costs’ (ULC), the labour cost of producing one unit of national income. They warn that even a small increase in wages without a matching increase in productivity will lead to lower exports, GDP and employment.

But changes in ULC are a poor measure of export competitiveness. They are derived from productivity measured across the whole economy, even though much of activity – including most obviously public services – does not enter into international trade. It would therefore seem better to use export prices or labour costs in exporting sectors. Even these, like ULC, prove to be a poor measure of competitiveness for traded goods in economies heavily dependent on outsourcing and inward investment by multi-national companies and with wages so far below the western European level. However, the European Commission sticks with ULC and that is the measure we are considering here.

The root of the problem lies in the way productivity is measured and compared between countries. In public services, such as education and health, the measure of output is derived from input costs, meaning to a great extent pay levels. Productivity therefore appears low simply because wages are low, without any reference to the content of the work. The outcome can be similar even in manufacturing industries. Firms outsource because wages are lower for making the same products. That is then reflected in lower prices and hence in lower measured productivity. Thus workers producing a car component outsourced to Czechia appear to be less productive than their German colleagues because the product is being sold at a lower price than when it was made in Germany.

Škoda in Czechia, part of the Volkswagen group, pays its employees around a third the German level. The difference does not reflect lower productivity in terms of cars produced. It is reflected in somewhat higher profits in the Czech plants, in a choice to locate production of cheaper models in those plants and probably also in the low transfer prices of components (notably engines and gearboxes) made in Czechia for other parts of the Volkswagen group. If pay were higher for workers producing Volkswagen engines in the Škoda plant, prices would be higher and the productivity of Czech workers would be measured as closer to that of German workers making the same product.

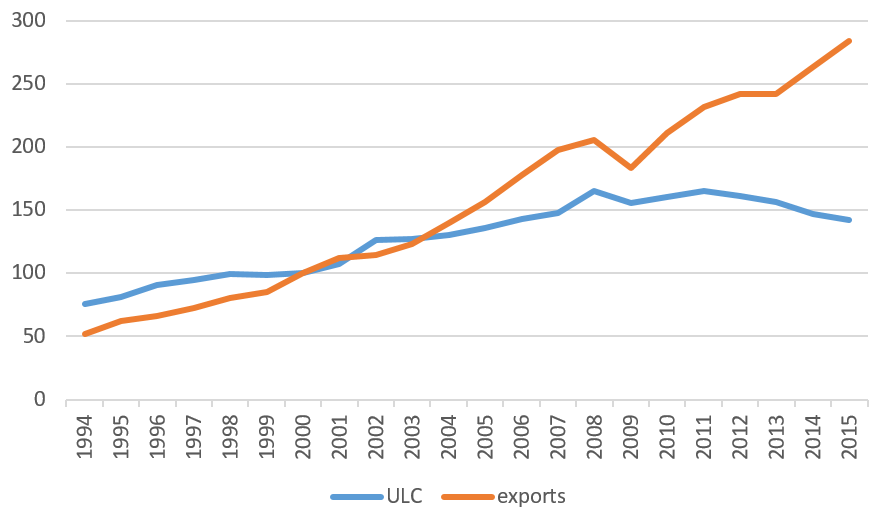

Figure 2: Unit Labour Costs and real export growth in Czechia between 1994 and 2015 (the year 2000 is 100 for all indicators)

Source: Calculated from European Commission data

Past experience shows that rising ULC do not prevent rising exports. Figure 2 shows this for Czechia. Until 2008, ULC were moving steadily upwards due to a rising exchange rate and wage increases in both the public and private sectors. These were then stopped in the post-crisis period. Exports faltered during the economic crisis and then resumed much the same growth as before. It was evidently just as worthwhile for multinational companies to increase production in Czechia whether wages increased or not when they remained so much lower than in western Europe.

There is scope for wages in central and eastern European countries to draw closer to western European levels. This could be achieved by resuming currency revaluation for those countries outside of the Eurozone, by negotiating higher wages through collective bargaining and by increasing minimum wages. Much higher wages might eventually lead multinational companies to relocate elsewhere, but that would currently be difficult, costly and pointless. Labour accounts for only about 6% of Škoda’s total costs while the costs of moving would be enormous. Meanwhile, higher wages would help stem the outflow of skilled and qualified workforces necessary for those activities – research, development and innovation – that support the higher pay levels in western Europe. Higher pay would thereby make possible inward investment and domestic economic activity with a higher technological level.

This article coincides with a conference, Europe Needs a Pay Rise, being held from 14-15 February 2017 by the European Trade Union Confederation (ETUC)

Please read our comments policy before commenting.

Note: This article gives the views of the author, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics.

_________________________________

Martin Myant – ETUI

Martin Myant is Senior Researcher and Head of Unit European Economic, Employment and Social Policy at the European Trade Union Institute (ETUI).