Non-Performing Loan (NPL) ratios in countries like Italy, Portugal and Spain have started to decrease sharply, but as Corrado Macchiarelli, Renato Giacon, Andromachi Georgosouli and Mara Monti write, this has received relatively little media attention in comparison to previous fears over the accumulation of NPLs in the EU. They explain that despite the lack of headlines about NPLs, one should not be too quick to draw the conclusion that they are no longer a critical issue for the EU’s future financial architecture. There are several reasons to keep a close eye on NPL policy management and legal developments both at the EU level as well as at the level of existing member states and potential future members in the Eastern periphery.

The assessment of credit risk is a critical part of the macro-prudential analysis, with the aggregate non-performing loan (NPL) ratio serving as a proxy for the economy-wide probability of default of the banking sector’s overall loan exposure. High NPL ratios impact on banks’ balance sheets and profitability, overall slowing down economic growth. Therefore, the factors driving NPL ratios in different EU countries have gained a lot of interest in recent years. NPL ratios in countries like Italy, Portugal and Spain have sharply started to come down, even if this has made less headline compared to the dread over NPLs’ accumulations up until recent. In the context of European Union member states, reducing the stock of NPLs is seen, particularly by Germany, as an essential step before further risk sharing mechanisms, including mutualisation, can be granted and for the very completion of the Banking Union (BU).

In this context, there’s been little progress since the Single Resolution Board guarantee, as there remain significant obstacles weighing against reaching an agreement for a European Common Deposit Scheme, as the third pillar for a fully-fledged Banking Union for Europe. One of the soundest arguments is that the traditional banking system remains destabilised, particularly in the EMU periphery, as evidenced by the persistence of “home bias” and a much uneven distribution of NPLs. The latter is currently seen as the main obstacle for the consolidation of a deposit insurance mechanism which would limit banks’ liquidity and solvency risks, because of moral hazard concerns.

The process of deleveraging of the southern periphery’s banking system is on its way, mainly through outright institutional and government intervention (e.g., in Italy with the help of government guaranteed agencies; see European Parliament, 2018). However, the search for yields in a low-interest rate and low growth environment is pushing banks to increase their holding of home government bonds, adding to the fragility of the banking system in the southern (euro area) periphery, and increase risky lending, which may intensify yet again the possibility of increasing NPLs in the future. This risk may materialise at the point the ECB will have, sooner or later, to pull the plug on the unconventional monetary stimulus.

There is a lot of uncertainty regarding the evidence on the current stock of NPLs, as the Bank for International Settlements (BIS) introduced only a few years ago a framework for the harmonisation of NPLs’ measurement. While discrepancies exist in the actual level of deteriorated loans on the balance sheets of European banks, the BIS and the International Monetary Fund (IMF) data would still agree on the trend. The literature on NPLs in Europe typically identifies several determinants of NPLs, including banks’ specific factors, as well as macroeconomic factors such as real GDP growth with no specific different determinants being identified even when the analysis is carried out in the traditional core-periphery sense across the euro area.

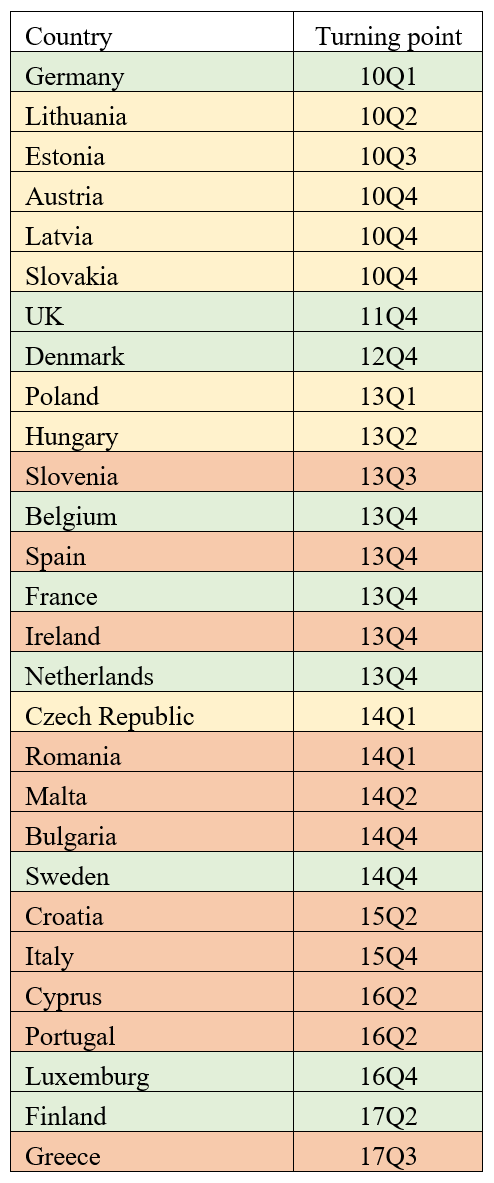

In looking for evidence about the extent of NPL accumulation and distribution across the EU, we construct quarterly NPLs series from the IMF quarterly Financial Soundness Indicators, which we compiled over the period 2007:Q1– 2018:Q3, by cross-checking them with the European Bank of Reconstruction and Development (EBRD) quarterly data and the IMF/World Bank Financial Indicators Annual data. By comparing the euro area with EU non-euro area countries, starting from high NPL levels, credit quality has continued to improve in many countries, with different turning points in the negative spiral of NPL accumulation (Table 1). The turning point has to be understood as the period after which deleveraging has started.

Among these, one can identify three groups of countries (see also European Parliament): a first group (Group 1) with no significant accumulation in NPLs during the last decade (Belgium, Germany, Denmark, Finland, France, Luxemburg, the Netherlands, Sweden, UK), a second group (Group 2) in which low levels of initial NPLs have been accompanied by moderately high increases during the crisis (Austria, Czech Republic, Estonia, Spain, Hungary, Lithuania, Latvia, Poland, Slovakia), and, finally, a third group (Group 3) in which high levels of NPLs were observed since the early pre-crisis and have persisted ever since (Bulgaria, Cyprus, Greece, Croatia, Ireland, Italy, Malta, Portugal, Romania, Slovenia). Interestingly, except Bulgaria and Romania, all countries in Group 3 share the single currency.

As one can see from Table 1, countries with historically low NPLs have kept accumulating those – last, Luxemburg and Finland – with minimal marginal variations on the NPLs ratios (Group 1, in green). Countries who experienced moderate increases, however, started the deleveraging quite early on, with the last EU-country to deleverage being Czech Republic (Group 2, in yellow). Among the third group, the countries that have started the deleveraging late remain the most problematic, with all of them being concentrated in the second half of the sample, hence having started the restructuring process later. Now that the deleveraging has begun, particularly with very steep decreases in countries such as Italy, Portugal and Spain, there seems to be less urge to discuss those experiences, and particularly which lessons, if any, one can learn from Central Eastern European countries. However, despite the general (and in some cases tardy) improvement, NPLs remain very persistent in some EU countries.

Table 1: Turning points in NPL ratio accumulation (ordered by quarter)

Note: The peaks are obtained using the Bry-Boschan (NBER) Business Cycle Dating Algorithm modified by Harding and Pagan for quarterly data.

The experience of the EU ‘Southern periphery’

For some countries of Southern Europe (euro area, in particular), the ratio is still far from the EU average: for instance, in 2018Q3 Italy had a ratio of 9.45% (11.1% at the end of 2017), Greece 43.4%, and Portugal 12% according to the European Banking Authority’s December 2018 Risk Assessment Report. Among the Southern Periphery countries, with Spain having started the deleveraging early after an all-time high of 13.6% in Dec 2013, Spanish NPL ratio came down to around 4.1% in 2018 Q3 from 4.5% at the end of 2017. The reason for the recent decrease was due to the selling of distressed debt.

In 2018Q3, the NPL ratio among Europe was at 3.4% or 714.3 billion euro compared to 4.1% and 814.5 billion euro in 2017Q4. The ratio was the lowest since 2014 when the total volume was EUR 1.17trn, and the NPL ratio was 6.5%, according to the European Banking Authority’s December 2018 Risk Assessment Report.

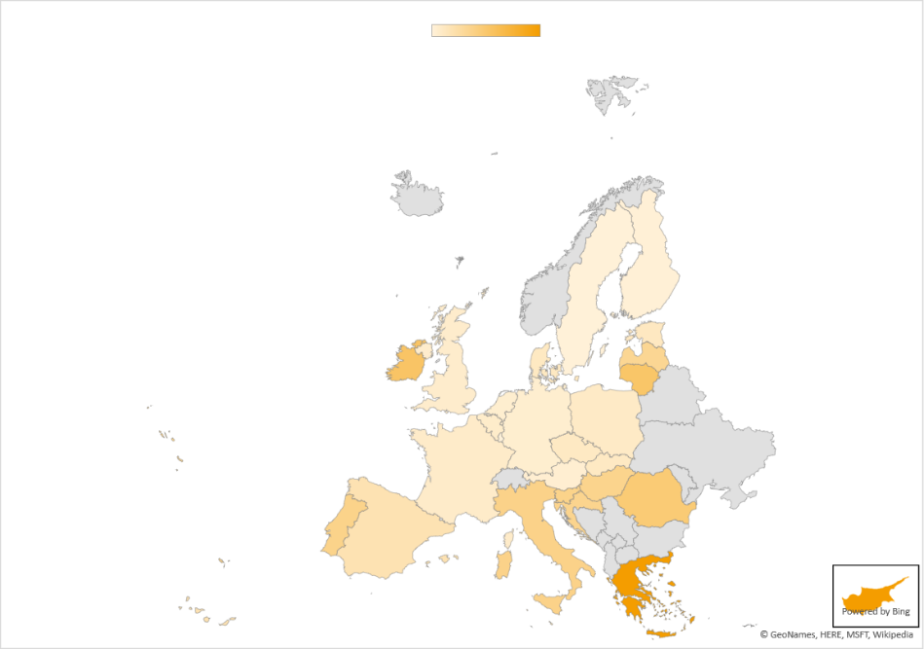

Despite the recent progress in the EU, the NPL ratio remains high compared to other developed economies such as Japan (1.2%) and the US (1.1%), and we expect the disposal of NPLs in the EU to continue (Figure 1).

The channel through which Southern European countries have decreased their NPLs ratio has been via forcing a comprehensive restructuring of the whole banking sector such as it has been the case in Spain, Cyprus and Greece (in the latter case, 12 banks were liquidated).

Figure 1: (a) NPL ratios at peak value

(b) NPL ratios in 2018

Note: Authors’ computations based on the results in Table 1 and IMF quarterly data

Out of a total market for NPLs disposals of 205.1 billion euro in gross book value and 142 transactions in 2018 – a record year compared with 144 billion euro in 2017 and 107 billion euro in 2016 – Italy led the region with 64 NPL sales with a gross book value of 103.6 billion euro. In Italy, almost half of these transactions were via securitisations within the government’s Garanzia sulla Cartolarizzazione delle Sofferenze (GACS) scheme, which had only until 6 March 2019 to run.

Spain followed with 43.2 billion-euro NPLs disposals in 27 deals; Greece with 8 NPLs dispositions for a total volume of 13.9 billion euro, Portugal 16 NPLs deals totalling 8 billion euro and Cyprus 2 deals worth 2.9 billion euro. Spain, in particular, set up a system-wide bad bank (SAREB) where non-performing assets were transferred from banks under restructuring inspired by Ireland’s NAMA bad bank.

The experience of the EU ‘Eastern periphery’

The experience of the EU Eastern Periphery has been only in part similar to its Southern peers, with Bulgaria, Romania Croatia and Slovenia being in the same bracket of – mostly Southern – EU countries with high levels of NPLs pre-crisis and post-crisis, while most countries in the EU Eastern Periphery were in the group with low levels of initial NPLs (Czech Republic, Estonia, Hungary, Lithuania, Latvia, Poland and Slovakia).

In absolute terms, the share of banks’ subsidiaries in the Eastern Periphery, indicating an increase in their NPL ratios in 2017, fell to below 10% compared to 60% in 2013, when countries including Romania, Slovenia and Bulgaria recorded NPLs above 20% of the total, while in Hungary and Croatia figures reached the high teens. However, tackling NPLs remains a priority in the EU Eastern Periphery. The substantial reductions in stocks over the last four years have led to a significant variation within the region as most countries have currently achieved low NPLs ratios while the only market where NPL ratios remained double-digit in 2018 was Croatia (11.3%)

NPLs reductions have been driven by legislative and regulatory changes (such as in Romania), boosting write-offs and the disposal of bad debts, as well as by increasing market appetite for impaired assets. Also, sales of NPLs in secondary markets have kicked off in countries such as Hungary mainly in the mortgage sector, Croatia (UniCredit sold a 448 million-euro portfolio of Croatian NPLs to Czech distressed-debt specialist APS Holding), Romania (a consortium of Deutsche Bank, AnaCap and APS bought a 360 million-euro NPL portfolio from Alpha Bank Romania).

Another reason for the original progress in the NPLs performance in the EU Eastern periphery is attributable to a critical step, the Vienna and NPL Initiative platforms, representing a joint undertaking of which the EBRD is a founding member together with the European Investment Bank (EIB) and other international financial institutions. The goal of the Initiative was to support financial stability in emerging Europe, including help the NPLs’ resolution and sale. One of the key reasons behind the Vienna Initiative was the realisation that three characteristics typical of the funding structure of the EU Eastern Periphery were likely to threaten financial stability in the region and necessitated the ad hoc establishment of policy actions. Those characteristics are (i) the foreign bank ownership structure, (ii) the systemic importance of a few banking actors and (iii) a funding structure mainly reliant on short-term wholesale markets. More in detail, recent research has highlighted the quirks of the EU Eastern periphery whereby it is the reliance of the banking system on wholesale markets, more than the ownership structure dependent on large foreign groups, to determine the banking stability of the region, with apparent effects on credit reduction and financial distress.

Despite the success of the Vienna Initiative, the pace of NPLs sales in the Eastern periphery has most recently slowed down with volumes falling from the 2016 record high of 7 billion euro to around 3.3 billion euro and are expected to decline further. Part of the slow-down of the decline in NPLs disposal in the EU Eastern Periphery is due to the demand side factors, as international buyers have been focusing on the EU Southern peers (NPL stocks in Greece and Cyprus, standing at 124 billion euro amount to more than twice the whole of the EU Eastern Periphery, with just 46 billion euro), and in part to supply-side factors as stocks of NPLs have been shrinking in the region due to the end of the local banks’ balance-sheet cleaning.

In order to revive interest in Central Eastern Europe, as well as South-Eastern Europe, Greece, Cyprus and Turkey, the EBRD approved in 2017 300 euro millions of financing for co-investment in NPL projects – in the form of an NPL Resolution Framework – in particular to take direct equity stakes of up to 15% in NPL servicers, make equity investments in NPL portfolios in partnership with private-sector buyers, and provide debt financing to an NPL acquisition structure. The first two joint-investment projects among the EU periphery have for now focused on Greece, as we shall discuss later.

Looking ahead

For most EU countries (both participating and non-participating in the BU), the accumulation of NPLs started in between the last quarters of 2009 and the first quarter of 2010 mainly due to fiscal constraints with ballooning budgetary deficits in the euro area periphery which fed into the negative feedback loop between sovereigns and the banks to the point that, in the case of Spain, European money became necessary. Since then, the attitude has changed, and the European framework moved in the direction of bail-in clauses and expected more mutual guarantees.

In the meantime, however, national and EU policymakers did not recognise promptly enough the creeping deterioration in NPLs and their effect on lending and the broader economy. Thus, the situation continued to deteriorate in several countries mainly belonging to the EU Southern periphery, where deleveraging started relatively late, related mostly to the leftovers of the previous crisis. Luckily enough, markets have worked out their solutions (see European Commission’s State Aid Scoreboard). National governments have also stepped up their efforts, also via quantitative targets on the resolution of NPLs (Ireland), codes of conduct between banks and indebted customers (Greece and Cyprus), a review of banks’ management of NPLs (which led, among other things, to the establishment of internal restructuring units in all large Greek banks), as well as reforms to guarantee a smoother functioning of markets for collaterals (auction mechanisms) and the creation of out-of-court procedures (Italy and Greece).

At the EU level, the regulatory approach to the treatment of NPL has certainly evolved in recent years. For instance, in the euro area, the Single Supervisory Mechanism aims to ensure that banks have adequate resources for the management of their NPLs.

Even though, in principle, there has been a definite shift of policy towards the creation of a comprehensive legal and institutional framework for the long term management of NPLs at EU level with the extensive involvement of EU institutions and agencies, banks and Member States are still thought to be primarily responsible for the reduction of NPLs and the prevention of future build-ups, as the recent experience suggests.

Currently, the development of an EU level policy for the treatment of NPLs is part of a broader plan of action to complete the Banking Union and to create the Capital Markets Union. Bank supervision including the revision of existing capital adequacy requirements, the creation of secondary markets for NPLs (also known as ‘distressed assets’), the reform of insolvency and debt recovery law and the restructuring of the banking industry stand at the epicentre of the Commission’s work. These operations happen quite often in synergy with other EU institutions and agencies, the Member States and competent national authorities. There are also relevant initiatives for the establishment of Asset Management Companies and steps to enhance the transparency of NPLs in Europe. All these measures mark an approach to the treatment of NPLs that aspires to be both proactive and reactive. Not only do they aim to reduce legacy loans but also to prevent their future accumulation and to avoid fire sales. As it stands, the practical implementation (and cost) of those measures has remained mostly national, however.

In the euro area, the lack of mutual guarantees and the willingness to provide those only to countries who achieve low NPL ratios does not represent a good signal for the Southern and Eastern Peripheral EU countries which are part of the Banking Union, and even less so for the prospective euro area member states, the NPL restructuring of which has gone through external policy support of international financial institutions in the form of the Vienna Initiative. It is interesting to note that such international support has also translated into a different instrument, an explicit NPL Resolution Framework, which is broader in coverage. As a part of this EBRD-led NPL Initiative, the EBRD has made its first disbursement by investing in a non-performing loan portfolio originated by Alpha Bank, a leading Greek lender, with an EBRD’s contribution of 25 million euro. A smaller (15 million euro) contribution has been recently approved in favour of another Greek bank, Piraeus, and there are plans to extend the resolution framework to Cyprus as well.

These transactions are the first EU sub-projects under a broader framework that involves 300 million euro to support efforts aimed at resolving the high levels of NPLs in many of the EBRD’s countries of operations; among which feature Cyprus and Greece. From the markets’ point of view, having a supranational NPL Resolution is fitting, given that Greek banks, together with Cyprus, have the highest non-performing exposure ratios in Europe (Figure 1).

In other words, while markets and the banking sector have adjusted, EU politics has not. This delay arguably is not a good signal for the Banking Union either. As long as the future expansion of the euro area through the acceptance of new members is still considered to be both economically and politically desirable, such a short-sighted NPL treatment is likely to be an obstacle. Although a lot will depend on the future power dynamics between the new president of the ECB and the 23-member Governing Council amongst other things, currently, we witness two policy trends. On the one hand, the Banking Union is seen as a necessary step to prevent future accumulations of NPL; i.e. hence its “pre-emptive” role.

On the other hand, a de facto European Resolution and an agreement on a European Common Deposit Insurance are slowed down by the lack of willpower by some member states in providing mutual guarantees ex-ante. In other words, the EU Banking Union is not given any “remedial” role (along the line of what the NPL Resolution Framework agreed for Greece, for instance) as achieving low levels of credit risk is deemed a necessary step for resource pooling. Given the well-recognised link between NPLs and growth, reducing and mostly keeping flat NPLs will be challenging for countries currently being stuck with lower growth rates, amid the uncertainty of Brexit, the US-China trade war, as well as the low-interest rate environment. This may risk weighing yet again against the European Banking Union completion. The question regarding NPLs remains therefore mostly political and as urgent as ever.

Please read our comments policy before commenting.

Note: This article represents the views of the authors and not those of EUROPP – European Politics and Policy, the London School of Economics, the European Bank for Reconstruction and Development or the National Institute of Economic and Social Research. Featured image credit: b.e.n. (CC BY-NC-ND 2.0)

_________________________________

Corrado Macchiarelli – Brunel University London / LSE

Corrado Macchiarelli – Brunel University London / LSE

Corrado Macchiarelli is a Lecturer in Economics and Finance at Brunel University London and Visiting Fellow at the London School of Economics’ European Institute.

–

Renato Giacon – EBRD

Renato Giacon – EBRD

Renato Giacon is Principal Counsellor, EU Affairs, Policy and Partnerships Vice Presidency, at the European Bank for Reconstruction and Development.

–

Andromachi Georgosouli – Queen Mary University of London

Andromachi Georgosouli – Queen Mary University of London

Andromachi Georgosouli is a Senior Lecturer at the Centre for Commercial Law Studies at Queen Mary University of London.

–

Mara Monti – LSE

Mara Monti – LSE

Mara Monti is Visiting Fellow at the London School of Economics’ European Institute.