In Capital and Ideology, Thomas Piketty proposes a vision for a fairer economic system grounded in ‘participatory’ socialism. This encyclopaedic, rewarding work merits thoughtful engagement and is essential reading, writes Ewan McGaughey.

Capital and Ideology. Thomas Piketty (translated by Arthur Goldhammer). Harvard University Press. 2020.

Find this book (affiliate link):![]()

Thomas Piketty’s Capital and Ideology is an encyclopaedic, rewarding work that merits thoughtful engagement. ‘I think this is a much better book than the previous one,’ said Piketty, referring to Capital in the Twenty-First Century (2014). ‘So if you read only one, please read this one!’ Personally, I would read both: while Capital in the Twenty-First Century has a positive thesis that with our current laws, the rate of return to capital exceeds the rate of growth (r > g), Capital and Ideology builds a normative thesis, driven by this data, that we should adopt democratic or ‘participatory socialism’. Piketty argues all societies use ideology to legitimise inequality; this ‘dominant narrative’ leads to rules and rules entrench inequality (1). Our era ‘wants to see itself as postideological but is in reality saturated by ideology’ (961). So, if things are going wrong, we should have a better ideology.

Thomas Piketty’s Capital and Ideology is an encyclopaedic, rewarding work that merits thoughtful engagement. ‘I think this is a much better book than the previous one,’ said Piketty, referring to Capital in the Twenty-First Century (2014). ‘So if you read only one, please read this one!’ Personally, I would read both: while Capital in the Twenty-First Century has a positive thesis that with our current laws, the rate of return to capital exceeds the rate of growth (r > g), Capital and Ideology builds a normative thesis, driven by this data, that we should adopt democratic or ‘participatory socialism’. Piketty argues all societies use ideology to legitimise inequality; this ‘dominant narrative’ leads to rules and rules entrench inequality (1). Our era ‘wants to see itself as postideological but is in reality saturated by ideology’ (961). So, if things are going wrong, we should have a better ideology.

This review engages three key ideas in Capital and Ideology: first, what democratic socialism involves; second, how votes in our economic constitution are even more unequal than wealth inequality; and third, how laws build markets and power sets prices.

Democratic Socialism

With inequality out of control, Piketty’s answer is democratic socialism. First, Piketty calls for extending the right to vote to workers in all enterprises. Workers should have ‘half the board seats in all private firms, large or small’ and we should create ‘true social ownership of capital’ (972). We must overhaul ‘the labor code and, more generally, the entire legal system’ to achieve ‘a just wage’ for everyone and ‘a more equal distribution of economic power’ (1003).

Second, Piketty calls for fair tax, including ‘progressive taxation of wealth’ based on ‘ability to pay’ (996). With this we can create ‘a universal capital endowment, and an ambitious social state’ (1000-16). This goes to the heart of Piketty’s definition of a ‘just society’ where all members have access to fundamental goods like ‘education, health, the right to vote’, so that even the least advantaged can ‘enjoy the highest possible life conditions’ (678-79). Thus, Piketty emphasises both predistribution to get things right (that is, ensuring law doesn’t drive inequality in its construction of the market or the state), and redistribution to undo the wrong.

Third, international trade needs to be balanced by fiscal cooperation, such as pledging at least 1 per cent of GDP for developmental assistance (1022-24). For the climate crisis, Piketty favours carbon taxes at €100 per tonne of carbon. However, fundamentally all reserves of fossil fuels ‘would be better kept in the ground to prevent global warming’ (654).

Image Credit: Crop of ‘Thomas_Piketty_2086’ by LSE in Pictures

Image Credit: Crop of ‘Thomas_Piketty_2086’ by LSE in Pictures

The value in Piketty’s work is that ‘socialism’ is well tested, but the ‘democratic’ part less so. A good contrast is Albert Einstein’s ‘Why Socialism?’ (1949). Einstein argued that capitalism means we are ‘unceasingly striving to deprive each other of the fruits of their collective labor […] in faithful compliance with legally established rules’. Law makes productive capacity the private property of individuals, workers don’t share fairly in the value they create and private capital becomes concentrated. The ‘crippling of the social consciousness of individuals’ is the ‘worst evil of capitalism’ and one from which ‘our whole educational system suffers’. But if there were a more ‘socialist economy’, asked Einstein, how do we ‘prevent bureaucracy from becoming all-powerful and overweening’ to protect ‘the rights of the individual’? With 70 years of experience, we can now provide a better answer to this question.

Votes in our economic constitution

With fair tax and trade, Piketty’s democratic socialism turns on who has votes in the economy, but this deserves some unpacking (full disclosure: Chapter Eleven draws on my writings on German, British and US law and history). First, most EU and OECD countries have a system for large corporations to have worker representation, typically one-third in large companies. Some of the best universities have majority-elected governing bodies, such as Oxford, Cambridge and Toronto. A growing body of research shows that we are poorer, more unequal and less innovative if we let shareholders and unaccountable managers monopolise enterprise governance. Piketty’s work could be valuably extended if we collect more systematic data on voting systems and their effect on economic variables.

Second, Piketty’s call for ‘true social ownership of capital’ leaves much to discuss. Most major corporations are nominally controlled by shareholders, who may fire directors. (The big exception is Delaware, USA, where directors tend to be much harder to remove.) Shareholders, however, are not individuals but overwhelmingly asset managers or banks with ‘other people’s money’.

The ‘big 3’ in the US are BlackRock, State Street and Vanguard, and combined they would be the largest shareholder in 435 of the 500 biggest companies. The shareholder votes they control come mostly from workers saving for retirement. About 12 people set all the priorities of corporate America – including wages, fossil fuel use, political lobbying and production decisions – in those asset managers. Much the same goes for Deutsche Bank, Commerzbank, Société Générale and Unicredit: power without responsibility. These middlemen should be strictly tied to the voting preferences of the real investors, who want fair pay, clean air and democratic politics. Similarly, sovereign wealth or national pension funds need to be strictly accountable to the people whose money is at stake. Fair tax, and fair wages, will vastly broaden the equitable distribution of capital.

Third, if competitive markets fail, the public needs a voice too. In education, health, municipal energy and water, and in media organisations, students, patients, residents and users often have voting rights but not in any coherent way. Piketty’s thesis could usefully be extended here: votes at work, in capital and in public services.

Law builds markets, power sets prices

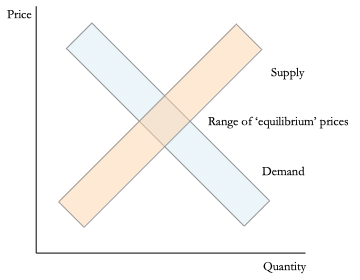

A third key idea is that the ‘level of wages and profits […] depends on prevailing institutions, rules and bargaining power […] as well as on taxes and regulations’ (641). This is groundbreaking and deserves discussion. Micro-economics theory has often asserted that prices are set by supply and demand, and in a competitive market they should reflect the marginal value added to production. However, Adam Smith saw that those with more power can ‘hold out’ longer in negotiations. When the first supply/demand charts were sketched by Fleeming Jenkin for corn, he was adamant that the same logic could not apply to labour, where workers were in a weaker position.

All markets are shaped by inequality of bargaining power, but for workers, tenants, consumers and small investors unequal power is systematic. Unequal bargaining power comes firstly from unequal distribution of resources, protected by our laws of property, contract, corporations, taxes and more. Second, bargaining power is driven by differences in collective organisation. Third, there are differences of information. Supply and demand merely set outer constraints on prices (the lowest a seller will go, the highest a buyer will pay if they can go elsewhere), and the actual place where a deal is struck depends on the actors’ power. If we chart unequal bargaining power with supply/demand, instead of lines and a single equilibrium point, there are bands and a range of ‘equilibrium’ outcomes (in the central diamond):

The result is that when rules set prices, such as a minimum wage, an energy cap or drug costs, or when rules require fair taxes, there is no distortion of efficiency compared to rules that allow a stronger party to impose prices on the weak. Very often there is an improvement of welfare if the rule prevents corporations taking an unjust gain by exploiting their unequal bargaining power. This theory is simple, intuitive and established in law, in contrast to complex explanations that markets are monopolistic or monopsonistic (relating to powerful buyers), dating from John Hicks, helpful as many have found them. It explains why most countries use fair wages, rent and price regulation successfully.

Paul Krugman’s review of Capital and Ideology stated he was ‘not even sure what the book’s message is’. Yet on reading the book, it’s crystal clear that Piketty successfully puts forward a superb, data-driven normative defence of democratic socialism. The principles that Piketty proposes – fair tax, fair trade, clean air and, above all, a democratic economy – have a huge amount to commend them, and make this book an essential read.

Additional Reading

‘From ‘‘Capital to Ideology’’ to ‘‘Democracy and Evidence’’: A Review of Thomas Piketty’, Ewan McGaughey, Œconomia, 2021.

Principles of Enterprise Law: The Economic Constitution and Human Rights, Ewan McGaughey, Cambridge University Press, 2022 (forthcoming).

Note: This review gives the views of the author, and not the position of the LSE Review of Books blog, or of the London School of Economics and Political Science. The LSE RB blog may receive a small commission if you choose to make a purchase through the above Amazon affiliate link. This is entirely independent of the coverage of the book on LSE Review of Books.

Feature image credit: Crop of ‘Thomas_Piketty_2296’ by LSE in Pictures

2 Comments