Both fiscal and monetary authorities have engaged in ‘unconventional’ policies over the past few years in order to bring the Great Recession under control. But, have these actions been intentionally coordinated, and what has been their economic impact? More fundamentally, has there ever been a systematic or regular coordination between fiscal and monetary policy in the US? Eddie Gerba and Klemens Hauzenberger find sufficient evidence for an implicit coordination of policies, and demonstrate how it has changed over the past three decades. They find that spending and tax stimuli have notably been more efficient in expanding the economy during the Volcker chairmanship (1979-84) and the Great Recession (2008-12). Taking into account that the current interest rate is constrained by the zero lower bound, fiscal authorities have an unprecedented window of opportunity to pursue activist policies aimed at expanding output, if and only if they carefully manage the expectations of private agents.

Both fiscal and monetary authorities have engaged in ‘unconventional’ policies over the past few years in order to bring the Great Recession under control. But, have these actions been intentionally coordinated, and what has been their economic impact? More fundamentally, has there ever been a systematic or regular coordination between fiscal and monetary policy in the US? Eddie Gerba and Klemens Hauzenberger find sufficient evidence for an implicit coordination of policies, and demonstrate how it has changed over the past three decades. They find that spending and tax stimuli have notably been more efficient in expanding the economy during the Volcker chairmanship (1979-84) and the Great Recession (2008-12). Taking into account that the current interest rate is constrained by the zero lower bound, fiscal authorities have an unprecedented window of opportunity to pursue activist policies aimed at expanding output, if and only if they carefully manage the expectations of private agents.

Locating the appropriate degree of interaction between fiscal and monetary policy plays a crucial role in ensuring economic stability. This has been most evident during the Great Recession in the US, when the US Federal Reserve reduced the Federal Funds rate by more than 500 basis points and injected a vast amount of liquidity into the financial system through 3 tranches of Quantitative Easing and executed 2 ‘Operation Twists’. In parallel, the Congress passed two fiscal packages, the $125 billion dollar Economics Stimulus Act in 2008, the American Recovery and Reinvestment Act of $787 billion in early 2009, and a fiscal reform in March 2012 intended to encourage the funding of small businesses by relaxing a number of regulations. The joint economic impact of the fiscal and monetary measures is, however, still unclear. The theoretical and empirical literature on fiscal-monetary interactions is equally inconclusive and points in multiple directions. While Fragetta and Kirsanova (2010) on one end argue that the two authorities simply ignore each other, Muscatelli, Tirelli and Trecroci (2004) show that depending on the shocks considered the nature of fiscal-monetary interactions differs.

We examined the interactions from a new angle by allowing for changes in the US’ economic structure and jointly studied the effectiveness of fiscal and monetary policy in stabilizing the economy. More specifically, we examined the fiscal transmission mechanism and monetary pass-through and provide empirical evidence on the structural shocks that have been most important in explaining fluctuations in the US economy.

What do we find? First, our results point toward an overall high degree of interaction between fiscal and monetary policy. However, the nature of interactions differs depending on the shocks considered. For spending and monetary policy shocks, a fiscal expansion (contraction) is followed by a monetary contraction (expansion). For a tax shock, on the other hand, a fiscal expansion (contraction) is followed by a monetary expansion (contraction), thus complementing each other’s responses. Moreover, we find that tax revenues largely influence decisions on spending, while spending does not influence tax decisions.

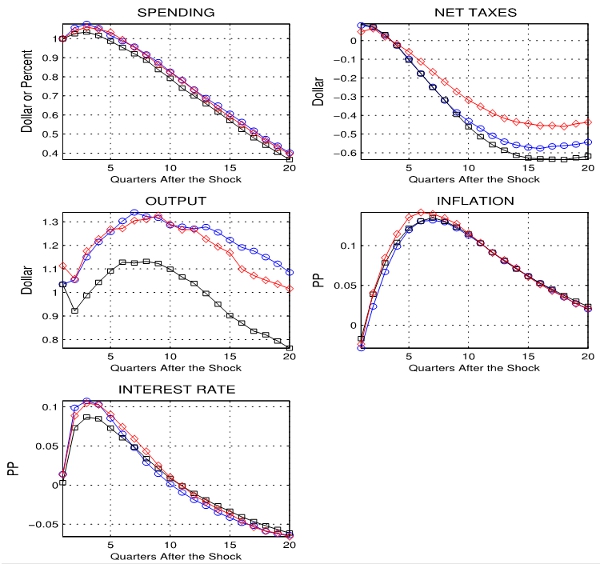

Which policy is more efficient in expanding the economy, a spending rise or a tax cut? Analyzing the impulse response of output to a 1-dollar spending increase in Figure 1, we find that the spending multiplier lies above 1 in all time periods but magnitudes differ considerably. While the multiplier is ‘only’ 1.1 during the Great Moderation (1985-2007), it reaches as high as 1.35 during Volcker Chairmanship (1979-1984) and the Great Recession (2008-2012). Moreover, the difference in the size of the multiplier persists also over the medium-run.

Figure 1: Median responses to spending increase during Volcker chairmanship (blue lines with circles), Great Moderation (black lines with squares), and Great Recession (red lines with diamonds).

Note: The spending response represents a one dollar shock to the real variables (response in dollar) and a one percent shock to the nominal variables (response in annual percentage points).

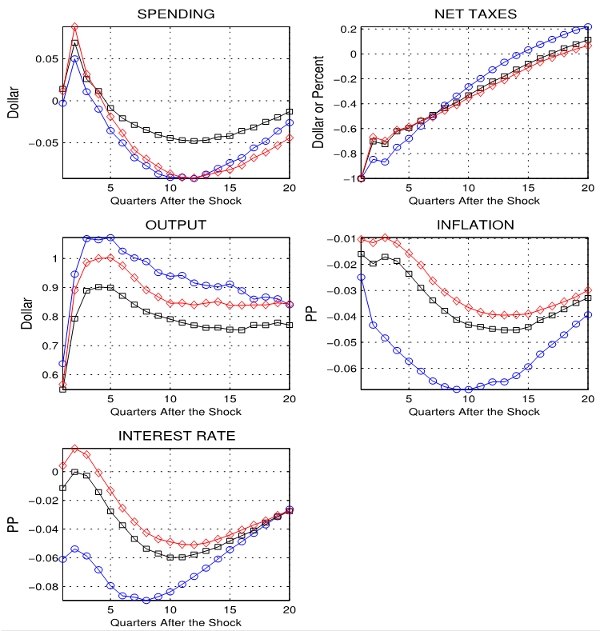

On the other hand, a 1-dollar tax cut results in an expansion of output of between 0.9 and 1.1 dollars (Figure 2). The lower end appears during the Great Moderation, while the higher during the Volcker Chairmanship and the Great Recession. This means that the spending multiplier is a quarter of a dollar (or 20 percent) higher than the tax multiplier during the Great Recession. If we contrast the Great Moderation as a regime with a mainly expansionary economy to the mainly recessionary of the Volcker chairmanship and the Great Recession then our results confirm the general findings of the literature: both multipliers are higher during recessionary (or turbulent) periods than during expansionary (or stable).

Figure 2: Median responses to tax cut during Volcker chairmanship (blue lines with circles), Great Moderation (black lines with squares), and Great Recession (red lines with diamonds).

Note: The tax response represents a one dollar shock to the real variables (response in dollar) and a one percent shock to the nominal variables (response in annual percentage points).

A plausible explanation for the success of the spending stimulus is that private agents do not expect a reversal of the stimulative measures anytime soon, but do anticipate higher taxes or spending cuts in the medium-run to finance the current fiscal expansion. Consequently, this pushes the real rates down but does not alter the expectations of private agents who believe in the commitment of the fiscal authority to balance the budget as soon as the economy is out of the crisis mode. As a result, aggregate demand will expand today without the extra cost of suppressing future demand from rising future inflation.

This articles is based on the paper Estimating US fiscal and monetary interactions in a time varying VAR submitted to the Journal of Money, Credit, and Banking.

Please read our comments policy before commenting.

Note: This article gives the views of the author, and not the position of USApp– American Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/1jcJwiV

_________________________________

Eddie Gerba – LSE European Institute

Eddie Gerba is a Research Fellow at the London School of Economics and holds degrees from Pompeu Fabra, ETH Zurich, LSE, and University of Kent. Eddie’s research interests lie in the fields of macroeconomics and quantitative finance. Of particular interest to his research are financial frictions, liquidity cycles, monetary policy, financial intermediation theory, as well as risk management and macroeconomic stability. Method-wise, his interests and experience lie in DSGE-models, computational methods, time-series econometrics, and derivative pricing models.

Klemens Hauzenberger – Deutsche Bundesbank

Klemens Hauzenberger is a Research Economist in the Macroeconomic Analysis and Projection Division, Deutsche Bundesbank. His research interests include Applied Econometrics, Bayesian Econometrics, Forecasting and Fiscal Policy.