In this article Andrew Sayer revives some concepts – ‘unearned income’, ‘rentiers’, ‘functionless investors’, and ‘improperty’ – to explain why the very rich are unjust and dysfunctional. We need to challenge the myth that the rich are specially-talented wealth creators, he argues.

In this article Andrew Sayer revives some concepts – ‘unearned income’, ‘rentiers’, ‘functionless investors’, and ‘improperty’ – to explain why the very rich are unjust and dysfunctional. We need to challenge the myth that the rich are specially-talented wealth creators, he argues.

In light of the news that the richest 80 people in the world have as much wealth as the poorest half of the world’s population, all 3.5 billion of them, and at the time of the plutocrats’ World Economic Forum in Davos, many people are talking about the extraordinary concentration of wealth at the top.

Here in the UK, the combined wealth of the richest 1,000 people is £519 billion (up from $450 billion in 2013). That’s over 4 times the size of the annual NHS budget (£127 billion), 12 times the size of the education bill (£42 billion), and 9 times the size of the welfare bill (£58 billion). We might well ask which of these figures can’t we afford? Given the tendency of the rich to portray themselves as specially-talented wealth creators we have to ask whether these inequalities are justified. In my new book Why We Can’t Afford the Rich, I argue they are unjust and dysfunctional.

To show why, we need to consider what economists call ‘the functional distribution of income’ – the different sources of income such as work, rent, interest and profit that go to different people. We can best do this by reviving some concepts which tend to have fallen out of use over the last 40 years – just at the time they were becoming more relevant: ‘unearned income’, ‘rentiers’, ‘functionless investors’, and ‘improperty’.

Unearned income is derived from control of an already existing asset, such as land, buildings, technology, or money, that others lack but need or want, and who can therefore be charged for its use. Those who receive it are ‘rentiers’. Mere ownership or possession produces nothing, and so any return to an owner merely for access or use is something for nothing. Compare the owner of ‘human capital’, or labour-power, who can only get an income by working – exercising that power to produce things that users want and that don’t already exist, whether it’s a loaf of bread, a computer app, or a school maths lesson.

If you buy some shares in M&S or BP on the stock market, the money you pay goes to the previous owner, not the company. You are what Keynes called a ‘functionless investor.’ When such so-called ‘investments’ pay off they extract wealth from the economy without creating anything in return. They are parasitic. As with rent, interest and profit from ownership of technology, the money gained can only have value if there are goods and services to buy with it, which means that those who have to produce these in order to make a living have also to produce extra to provide the rentier with unearned income. Rentiers free-ride on the labour of others. Since it’s a payment for nothing that didn’t already exist, it’s a deadweight cost, and so not only unjust but also dysfunctional for the economy. With the dramatic increase in shareholders’ power over companies during the last four decades, Keynes’ functionless investor has escaped the euthanasia he recommended and is thriving on unprecedented flows of unearned income in dividends and speculative gains from trading shares and other securities. Could speculation at least perhaps make markets work more efficiently? Possibly, though we have to ask which markets: are they for rentier opportunities in securities, property, the latest bubble? Rent-seeking needs to be cut back, not made more ‘efficient’.

Many imagine the era of the rich rentier is over: don’t ‘the working rich’ make up majority of the wealthy now, getting most of their income from salary, not capital gains, or interest payments or rent, etc.? They do indeed, though inherited wealth is considerable (28 per cent of wealth in the UK) and getting bigger as wealth concentrates at the top, as Thomas Piketty has shown; and it mainly provides the children of the rich with huge windfalls. But the working rich in the top 0.1 per cent mostly either work for rentier organisations that collect and seek rent, interest, dividends, capital and speculative gains, or control key positions where they can determine their own pay. This is most obvious in the financial, insurance and property sectors where many rich people work, but companies in the non-finance sector have made an increasing share of their profits in finance too by ‘investing’ in securities. (The scare quotes for ‘investment’ are intended to distinguish it from real investment in new infrastructure, products, technology or training). In the UK in 2008, 69 per cent of the top 0.1 per cent worked in finance and property, 34 per cent were company directors in this and other sectors, and 24 per cent of those in the rest of the 1 per cent were too.

Studies of many leading capitalist countries show striking declines in the share of output going to labour in recent decades. In the US, the top 1 per cent of those with employment incomes took a rising share of net value-added of US business from the 1980s to 2008. As long as they kept shareholders well-fed with unearned income, CEO incomes were allowed to soar away from average incomes: in the US, 7 CEOs are paid more than 1,000 times average pay. Top corporate officers may not be owners but, particularly with the weakening of organized labour, financial deregulation and globalisation, they have been able to take an increasing share of value-added.

A house used to live in is property. A house used as a way of extracting unearned income in the form of rent and capital gains is what J.A. Hobson, writing in the 1930s, called ‘improperty’. Many people are part-time rentiers, supplementing their earned income by renting out some improperty. Some may borrow money from big-time rentiers to do this. Buy-to-let is a means by which those with money can make still more money from those with little. We need to tax unearned income like inheritance, rent, interest, dividends, capital gains much more.

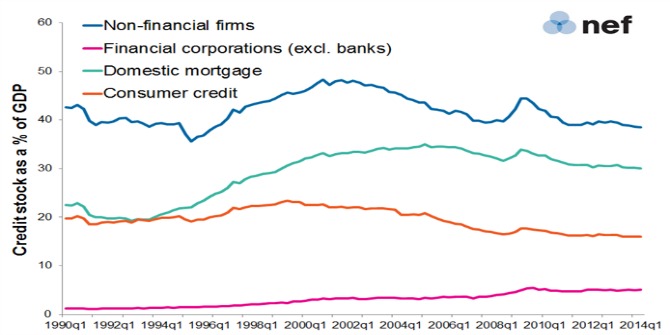

We need a finance sector that is fit for purpose as a servant to the economy instead of a master. Currently, most of what it funds is not productive industry but lending against existing assets: in the UK lending by the financial sector to productive businesses declined from 30 per cent in 1996 to 10 per cent in 2008, and has stayed low since, while lending to other financial institutions and the property market grew. But then, to the financial sector, £1 million profit from useless speculation is no different from £1 million from any other source. Yet the difference matters to the economy as a whole and hence to us.

There are other reasons why we can’t afford the rich: their undemocratic and indeed antidemocratic influence in politics (witness Davos and TTIP), their excessive and wasteful consumption, their bloated carbon footprints and the fact that many are in effect betting on unsustainable economic growth in the rich countries and have interests in continued fossil fuel use. I deal with all these in my book, but above all, we need to challenge the myth that the rich are specially-talented wealth creators; it is time to halt the flood of unearned income that goes to the top and reassert democracy in facing the challenge of organising economies that stop rather than accelerate global warming.

Note: This article gives the views of the author, and not the position of the British Politics and Policy blog, nor of the London School of Economics. Please read our comments policy before posting. Featured image credit: Images money CC BY 2.0

Andrew Sayer is Professor of Social Theory and Political Economy at Lancaster University. His main interests are inequality and ‘moral economy’– the assessment of justifications for particular economic institutions and practices. Previous books include The Moral Significance of Class (2005), and Why Things Matter to People (2011) (both Cambridge University Press). He blogs at http://asayer25.com.

Owning buildings or technology does not constitute rentierism, since buildings and technology require maintenance and become obsolete with competition and depreciation. True rent — truly unearned income — is land rent, the value realized from controlling economic land. Land is fixed an supply — cannot be created — and is necessary for all life and production. And land rent is rightfully common property, owed by land users to the people they’re excluding from the site — not to a legally privileged few freeholders. (The fact that the privilege was bought doesn’t make it any more just.) With guaranteed access to land, a.k.a. existence, people will have no problem creating their own housing and, if they want, competing in the tech field.

Of course, in the real world, there are effective entry monopolies on house-building and tech enforced via building codes and IP (over-)protections. But mere *ownership* of any type of man-made capital, independent of these monopoly protections, does not constitute rentierism.

A fascinating topic for debate, although the arguments appear quite flawed to me. Hopefully the readership can recognise the same. I’d struggle to get through his book if this is the strength of the rationale.

A comparison of wealth – a measure of capital – with annual expenditure on public services is inappropriate – I guess it’s just an attempt to generate an emotive response. Obviously, if the former is used to pay the latter, then neither will remain – if you remortgage the house to pay your bills, in time you’ll have nowhere to live!

“Mere ownership or possession produces nothing…any return for access or use is something for nothing”. Actually, rent represents a return on capital, in the most literal sense. The owner has invested or otherwise tied up capital in that asset, capital which was itself earned in some way. For nothing?

Buying a share in a company on the secondary market does, as Mr Sayer observes, require a cash transfer from the buyer to the prior shareholder, and not the company itself. But consider a scenario where there is no possibility of a secondary market transaction – any equity capital funders would be required to hold that share indefinitely. Clearly, the pool of people willing and able to invest capital on those terms is much smaller (if any). Ironically these investors would be ‘the Rich’ that Mr Sayer decries. And in order to entice this smaller pool of investors to tie up their capital indefinitely, the company must pay more than it would otherwise need to. The simple fact is, a secondary market in equities (in any asset) allows a cheaper cost of capital for companies. And the public benefit of that is a lower hurdle for investment – more stuff gets done.

Well said. It’s almost as if the author hasn’t taken Economics 101. Unless there is exactly 0 time discounting, savings must have a positive expected return. The idea that a receipt of savings is transferable doesn’t make it corrupted or evil to save money.

Yes, rent is a return on capital. But it still produces nothing; it is still an extraction from the wealth created by the on renting from the rentier. All of this would still be possible if, instead of allowing the base capital to be privately owned, it were managed democratically.

So let’s get this right: If I own a company that produces medicines, employs 10,000 people world wide and invest billions in new cures I’m a parasite whereas every person in that company is an oppressed prole whose blood I suck? Have you ever considered that the workers couldn’t possibly have got to the state where production is possible without risk from investors and the guiding hand of the people who formed the company, and that in a competitive market my capital is at risk daily from legislation, legal liability and the govts who read guff like this and decide to tax business out of existence?

Business pays for everything you see, eat, the fresh water you drink and the NHS when you’re ill. It pays for the roads you drive on and the University you lecture in. Never forget that.

This comment contains so many non-sequiturs and begs so many questions that it’s difficult to know where to start. The simplest response would be “read Sayer’s book to understand why the current system is unsustainable at so many levels – not least in relation to capitalism’s own goals, which are currently self-defeating.”

But me just list some of the questions:

1. How did you get to “own” that company?

2. Are all your employees paid a wage that enables them to live a comfortable and fulfilling life abd bring upp their families in security? Do they have job security and rights?

3. OK. So we can agree that the production of medicines is worthwhile – you have chosen a deliberately skewed product. But what if your company was producing cigarettes or weapons or high-salt/high-sugar foods? Would the story sound so apple-pie?

4. Wouldn’t it be better if things like medicines were produced for the public good rather than profithich leads to all sorts of distortions – e.g. mis-selling of drugs, denial of drugs to poorer peoples, etc).

5. Why should peoples’ investments be prone to risk? Most particularly, why should people’s pensions – the only investment that most people have – be prone to risk? The prioritising of share value simply distorts the rational distribition of goods and services.

6. It is nonsense that only “business” produces wealth. What about education? Education contributes fundamentally to the production of wealth, as well providing the educated workforce that business needs for its profits.What about the millions of invisible, unpaid carers who sustain the invisible infrastructure of society? They are contributing to wealth production, but get to see very little of it. Business does not pay for the fresh water I drink – I do.

7. Business contributes some of the costs of the NHS or the roads we drive on, but indvidual taxpayers also contribute massively (and are unable to evade taxes in the way that businesses such as Amazon do). There is very little evidence that governments are “taxing businesses out of existence”.

8. Who could possibly deny the need for regulation of businesses after the catastrophe of 2008/9 – the direct result of the derugulation of the financial sector.

Congratulations, Nicholas Till. As good a demolition of a flawed polemic as I’ve read in a long time. Though I think you were a little generous to the pharmaceutical industry, which has been known to do a spot of price gouging and has occasionally failed the product safety test. Like that well-known “medicine” thalidomide.