The relationship between the countries in the EU that use the euro as their currency (‘euro-ins’) and those that do not (‘euro-outs’) is the most important of the four areas in the ‘new settlement’ between the UK and the EU, write Nauro F. Campos and Corrado Macchiarelli. This post presents new econometric estimates showing that, after the introduction of the euro, the UK and Eurozone business cycles became significantly more synchronised. It is likely this upsurge in synchronisation increased the costs of a potential UK exit from the EU.

Four different areas define the ‘new settlement’ between the UK and the EU. These are migration, sovereignty, competitiveness, and governance. Regarding potential economic consequences, there seems to be a robust consensus that the governance of the relationship between the countries that use the euro as their currency (the ‘euro-ins’) and those that do not (the ‘euro-outs’) is by far the most important issue. It is therefore surprising that it has received so little attention. Indeed, the extent to which this issue remains absent in both academic writings and the media is almost shocking. It is certainly complex and technical, but these are neither reasons for why the issue will become less important in the near future nor to avoid trying to organise our thoughts about it.

Our aim here is to redress this state of affairs by trying to encourage further discussion of the relationship between the euro-ins and euro-outs. Although there are many other worthwhile starting points to study this relationship, we choose to concentrate on business cycle synchronisation. The focus on business cycle synchronisation is because the loss of monetary policy autonomy is a major cost of sharing a currency. Such cost is inversely related to the degree of business cycle synchronisation. In what follows, we try to provide a brief general overview of facts and theories and, most importantly, present new econometric evidence. Our estimates indicate that, after the introduction of the euro, the business cycles of the UK and the Eurozone became significantly more synchronised. We conclude with a discussion of the implications in terms of the costs and benefits of a potential exit from the EU (‘Brexit’).

Background

During the negotiations of the 1992 Maastricht Treaty, the UK and Denmark secured rights to not join the European Monetary Union. Every one of the other 26 European Union members is legally committed to using the euro as its currency, when ready (De Grauwe 2016).

In 1997, the new Labour government decided to reconsider the decision to stay out of the EMU. The UK Treasury was charged with the policy analysis which focused on ‘five tests’ (as they were known at the time): business cycle synchronisation, labour mobility, investment, competitiveness of the financial system, and growth and stability. The final verdict from the Treasury was that long-term convergence of UK and EZ business cycles had not reached satisfactory levels and that ‘despite the risks and costs from delaying the benefits of joining, […] a decision to join now would not be in the national economic interest’ (2003).

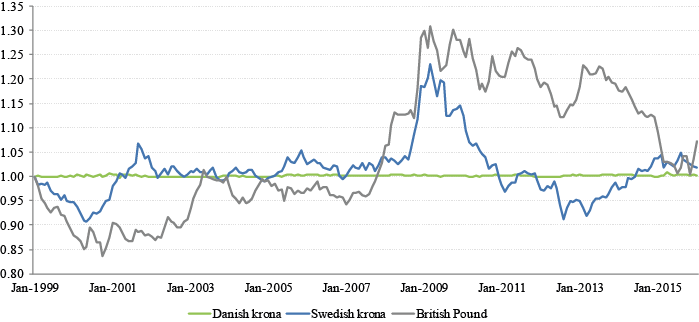

Figure 1. Bilateral nominal exchange rates against the euro (1 Jan 1999 = 1)

Source: OECD Statistics data

As Figure 1 suggests, the UK and Sweden have a floating exchange rate regime (Pesaran et al. 2007) while Denmark participates in the ERM2. The behaviour of the Danish krona is remarkable. The high levels of business cycle synchronisation and large share of exports to the Eurozone suggest the costs of adopting the euro remain small for Denmark (Holden 2009).

Tooling up – theoretical perspectives

The main research question driving the scholarship on optimal currency areas regards the costs and benefits of sharing a currency (Alesina and Barro 2002). The main cost is the loss of monetary policy autonomy. Benefits are mostly in terms of reduction of transaction costs and exchange rate uncertainty, and of increasing price transparency, trade, and competition. Recent econometric evidence reporting ‘no substantive reliable and robust effect’ of currency unions on trade qualifies some of these benefits (Glick and Rose 2016).

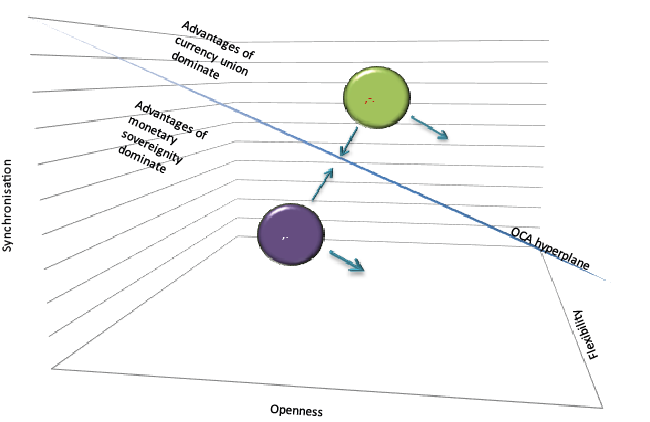

One insightful way of framing the issue of optimum currency areas is that of De Grauwe and Mongelli (2005). They study the interactions between symmetry, flexibility, and integration. The downward-sloping optimal currency area plane in Figure 2 shows the minimum combinations that countries must observe in order for a monetary union to generate positive net benefits.

Figure 2. The open currency area trinity: Symmetry, openness and flexibility

De Grauwe and Mongelli (2005) place the Eurozone (EU) to the outside of (within) the optimal currency area plane, suggesting those countries are (not yet) sufficiently integrated to generate efficiency gains that can compensate for the macroeconomic costs of the union. The degree of economic integration and the symmetry change over time. The arrows from the EU and euro circles illustrate different views of this evolution. Even before the European Monetary Union, there was debate about the extent to which a monetary union affects symmetry (Krugman 1993). Focusing on the symmetry openness dimension, one can see that increased integration may raise income correlation. The EU would move along the upward arrow. In another scenario, specialisation will bring about less symmetry and thus countries move downwards along the optimal currency area plane.

There are at least two recent developments in optimal currency area theory that should also inform this debate. The original optimal currency area formulation stressed labour mobility, product diversification, and trade openness as key criteria and explored the possible endogeneity of currency unions. Recent work calls attention to the role of credibility shocks. If there are varying degrees of commitment (furthering time inconsistency problems), countries with dissimilar credibility shocks should join currency unions (Chari et al. 2015). A second relevant recent strand highlights situations in which optimal currency area criteria are thought of as interdependent by focusing on the case of interactions between openness and mobility (Farhi and Werning 2015).

Synchronising is hard to do

Business cycle synchronisation played an important role in the turn-of-the-century UK debate about joining the EMU. Indeed, it was one of the ‘five tests’. In 2003, the UK Treasury decided the level of business cycle synchronisation was not sufficiently high. Yet, several studies show that the convergence between the Eurozone and the UK has increased since 1999 (e.g. Canova et al. 2005, Giannone et al. 2010).

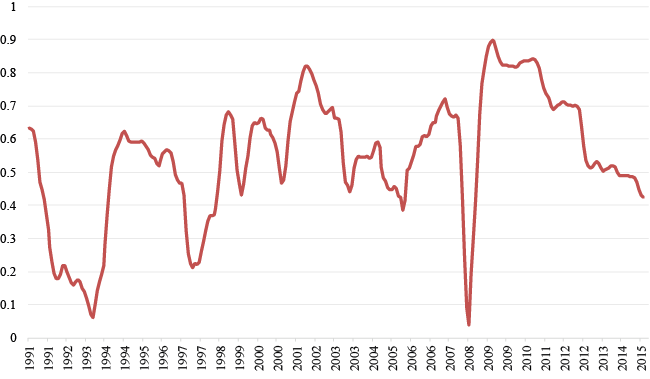

The extent of synchronisation between the Eurozone and the UK can be determined by the conditional correlation of the cyclical components (i.e. the gap) in industrial production. Figure 3 shows our estimates for the conditional correlation (Engle 2002) between the UK and EZ business cycles (Harding and Pagan 2006.) The series clearly shows both the consequences of the 1992 exit of the British pound from the European Monetary System and the 2007-09 run up to the crisis. Overall, there has been an increase in synchronisation. The point estimates of the correlation coefficients between industrial production growth in the UK and Eurozone are clearer. The average for the full period (1991-2015) is 0.54. It started from 0.37 in 1991-1998, increased to 0.77 in 1999-2006, and again to 0.81 in 2007-2015 during the Great Recession.

Figure 3. Conditional correlation in the UK vs. Eurozone cycles

Source: Datastream data. Authors’ calculations.

Note: Computed using conditional correlation analysis. This recovers the estimated innovations for the cyclical component of industrial production and generates a measure of this correlation that is conditional on cyclical features. We use the exponential smoother from Engle (2002) and obtain cycles using a Kalman filter (Harvey 1989). Given possible structural breaks, the specification for the trend-cycle decomposition is augmented with standard interventions. To detect influential residuals, we use the Harvey and Koopman (1992) two steps auxiliary regression procedure. In the first step, the focus is on outliers and break detection. The second step involves estimating the model with those interventions which were found significant in the first step.

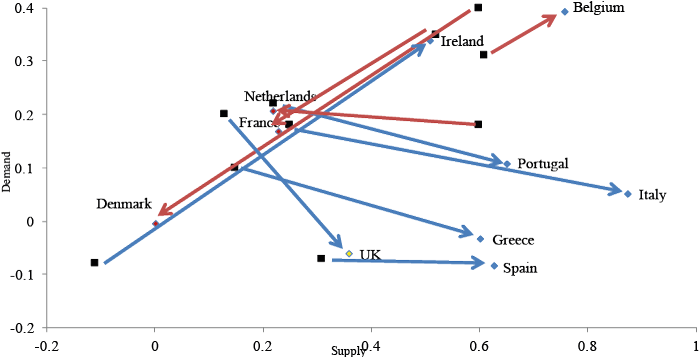

An important additional consideration regards differences between supply and demand shocks (Ramey forthcoming). Bayoumi and Eichengreen (1993) famously argue that, based on the degree of supply shocks synchronization, one can identify a ‘core’ (Germany, France, Denmark and Benelux) where shocks are highly correlated, and a ‘periphery’ where synchronisation is much lower. They also note that demand shocks correlations are much lower, even for those countries in the ‘core’.

The European Monetary System may have eliminated autonomous monetary policies as a source of idiosyncratic demand shocks, but national fiscal policies remain independent so the cross-country correlation in movements in demand may persist. Hence, we decided to update this influential Bayoumi and Eichengreen (1993) exercise to assess to what extent the European Monetary Union has reinforced the core-periphery pattern they identified with data up to 1988, that is, pre-European Monetary Union. Figure 4 shows our results suggesting that the European Monetary Union has considerably weaken this core-periphery pattern (Campos and Macchiarelli 2016). The European Monetary Union has fostered integration in the EU as a whole and the UK economy was not immune to these changes. UK business cycles become more synchronised after the euro and, hence, its economy much more integrated.

Figure 4. The dynamics of the correlation of supply and demand disturbances between pre-EMU (1963-1988) from Bayoumi-Eichengreen (1993) and post-EMU (our calculations, 1991-2014)

Note: The figure compares estimates from pre-Maastricht based on Bayoumi and Eichengreen (1992), covering the period 1963-1988, with our equivalent estimates for the period 1991-2014 (post-EMU). For each country, we estimate a bi-variate SVAR using (log) real GDP and the (log) deflator, both in first differences. The structural identification of the shocks follows Bayoumi and Eichengreen (1992) and control for changes in regimes. Red arrows denote movements of the so-called ‘core’ countries, and blue arrows movements of the ‘periphery’.

Implications for Brexit

Our estimates show that, after the introduction of the euro, the UK and EZ business cycles became substantially more synchronised. This result has important yet still poorly understood implications in terms of the net benefits of a possible exit from the EU.

Two qualifications are in order. One is that the net benefits from the increases in synchronicity, trade openness and labour mobility since 1999 are not entrenched or irreversible. They can be reduced by policy inconsistencies and delays (and many argue this happened between 2010 and 2014). Despite the weakening of the ‘core-periphery’ pattern we uncover, irreversibility should not be taken for granted.

The second regards the consequences of this upsurge in synchronisation in the old core of the EU. Our results suggest euro-outs became more integrated, despite not using the euro as their currency. All else equal, an upsurge in business cycle synchronisation leads to an increase in the net benefits of currency union membership. Hence the costs of leaving the EU, even for euro-outs, may have risen (maybe substantially) after and during the introduction of the EMU.

As stressed above, our main goal here is to call attention to the fact that the consensus about the relationship between euro-ins and -outs being the most important aspect of the ‘new settlement’ has not yet translated into proper discussions of the matter. We try to redress this situation by focusing attention on one aspect (business cycle synchronisation). There are various other important issues that deserve empirical scrutiny, such as the interactions among trade openness, labour mobility, and business cycle synchronisation. Moreover, these must be carried out fully acknowledging that the European Monetary Union has changed and will continue to do so. The construction of a genuine European Monetary Union is ongoing and a critically important element in this debate (Begg 2014).

References can be found at Vox.EU, where this article first appeared.

This post represents the views of the authors and not those of BrexitVote, nor the LSE.

Nauro F Campos is Professor of Economics and Finance, Brunel University, a Research Fellow, IZA-Bonn, and a Research Affiliate at the Centre for Economic Policy Research (CEPR). Corrado Macchiarelli is Lecturer in Economics and Finance at Brunel University, London and a Visiting Research Fellow at the LSE’s European Institute.

The authors seem unaware that the Euro-zone is suffering from the unique architecture that has made the “German euro” at least 40% undervalued & that is crippling Southern Europe.

No respectable article on the subject of the euro can just ignore this terrible fact of life.

The article therefore is pointless & worthless.

We use cookies on this site to understand how you use our content, and to give you the best browsing experience. To accept cookies, click continue. To find out more about cookies and change your preferences, visit our Cookie Policy.

The relationship between the countries in the EU that use the euro as their currency (‘euro-ins’) and those that do not (‘euro-outs’) is the most important of the four areas in the ‘new settlement’ between the UK and the EU, write Nauro F. Campos and Corrado Macchiarelli. This post presents new econometric estimates showing that, after the introduction of the euro, the UK and Eurozone business cycles became significantly more synchronised. It is likely this upsurge in synchronisation increased the costs of a potential UK exit from the EU.

The relationship between the countries in the EU that use the euro as their currency (‘euro-ins’) and those that do not (‘euro-outs’) is the most important of the four areas in the ‘new settlement’ between the UK and the EU, write Nauro F. Campos and Corrado Macchiarelli. This post presents new econometric estimates showing that, after the introduction of the euro, the UK and Eurozone business cycles became significantly more synchronised. It is likely this upsurge in synchronisation increased the costs of a potential UK exit from the EU.

The authors seem unaware that the Euro-zone is suffering from the unique architecture that has made the “German euro” at least 40% undervalued & that is crippling Southern Europe.

No respectable article on the subject of the euro can just ignore this terrible fact of life.

The article therefore is pointless & worthless.