Hopes are high in the Department for International Trade that Britain can quickly negotiate its own free trade agreements (FTAs) with countries like South Korea. The EU already has a very comprehensive FTA with the East Asian state, so is the UK in a position to negotiate a better one? Simon Hix and Hae-Won Jun examine the factors at play. They conclude that it will not be in South Korea’s interests to negotiate a deal more favourable to the UK – not least because it probably cannot give Britain more access to the market in services without offering the same deal to the EU.

Hopes are high in the Department for International Trade that Britain can quickly negotiate its own free trade agreements (FTAs) with countries like South Korea. The EU already has a very comprehensive FTA with the East Asian state, so is the UK in a position to negotiate a better one? Simon Hix and Hae-Won Jun examine the factors at play. They conclude that it will not be in South Korea’s interests to negotiate a deal more favourable to the UK – not least because it probably cannot give Britain more access to the market in services without offering the same deal to the EU.

On 17 January the British Prime Minister set out her vision for the UK outside the EU. A central theme of her speech was that the UK would become a “Global Britain”, “always acting as the strongest and most passionate advocate for free trade right across the globe”. The next day, the Foreign Secretary, Boris Johnson declared that “countries are queuing up for trade deals with the UK”. Then, writing in The Daily Telegraph, the International Trade Secretary, Dr Liam Fox, declared that: “All along we have made it clear that we want Brexit to have no disruption to global trading. Important trading partners, from Korea to Mexico, will be guaranteed the same market access to the UK that they have today”. In short, some key assumptions of the government’s Brexit plan are that the UK will be able to agree new free trade deals with countries outside Europe, that these deals could be agreed quickly – particularly with countries that already have trade deals with the UK via the EU – and that these deals would reap new economic benefits for the UK.

To assess how realistic these assumptions are we consider some global trade data as well as the trade relationship between the UK and South Korea, which has an existing free trade agreement (FTA) with the EU, which covers the UK as an EU member state.

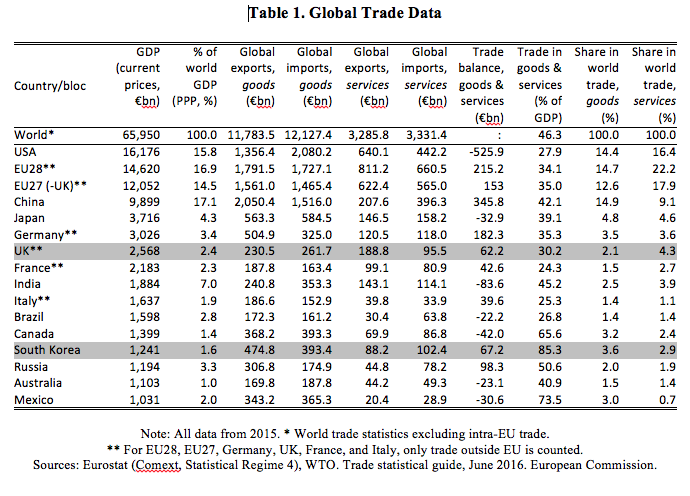

Table 1 shows some of the main measures of global trade in 2015, the most recent year for which comprehensive data are available. The EU either with or without the UK is the world’s second largest economy, and together the USA, EU27 (minus the UK), and China command 48% of the global economy, 42% of global trade in goods (not counting internal EU trade), and 43% of global trade in services. The UK outside the EU would be the fifth largest economy, but would only command 2.4% of global GDP, 2.1% of global trade in goods, and 4.3% of global trade in services. In short, the UK would not be in the “premier league” as a global trading power. This is not to say that the UK could not be a successful economy outside the EU, but does suggest that the UK is unlikely to be in a strong bargaining situation when negotiating free trade agreements, particularly with the world’s dominate trading powers: the US, the EU, and China.

To shed more light on the free trade prospects for the UK outside the EU, let us look at the situation from the point of view of South Korea, which will be a similarly-sized trading power to an ‘independent’ UK. South Korea is the world’s 9th largest economy (counting the EU as a single bloc), and in terms of global trade (not counting internal EU trade), South Korea’s combined trade volume (exports plus imports) in goods and services was larger than the UK’s in 2015, at €1,059bn compared to the UK’s €777bn.

South Korea already has an FTA with the EU, which hence currently covers the UK. So, South Korea is likely to be near the “front of the queue” for a new free trade agreement with the UK, as Liam Fox has suggested. Could this agreement be concluded quickly? What would the terms of such an agreement be? And would these terms be more or less beneficial for the UK than the current EU-South Korea FTA?

To answer these questions, let us look in more detail at the EU-South Korea FTA, which entered into force on 1 July 2011. Because the EU and South Korea had been working on a series of mutual assistance and trade agreements for some time, the EU-South Korea FTA was concluded relatively quickly. Negotiations started in May 2007 and were concluded in October 2009. It then took a further 2 years for the deal to be adopted and implemented. The European Parliament did not ratify the EU-South Korea FTA until February 2011, and only after South Korea had made several further concessions, including a new “safeguard” clause to protect European industry and a guarantee that new Korean car emissions limits would not be detrimental to European car manufacturers.

Two issues make the EU-South Korea agreement particularly interesting from a trade point of view. First, the agreement is the most ambitious of the 30 or so trade agreements that the EU has signed so far, in that it covers a larger volume of bilateral trade than any other agreement between the EU and a third country. For example, in 2015 EU-South Korea trade was €90bn, whereas EU-Canada trade was only €64bn. The EU trades more with the United States and China, but the EU does not yet have free trade agreements with either of these countries.

Second, the EU-South Korea agreement is interesting because it is the most comprehensive agreement the EU has implemented to date, and is one of the most comprehensive trade agreements signed between any two partners anywhere in the world. Import duties (tariffs) are eliminated on almost all products. The agreement also goes far beyond the liberalisation of services market that both parties have already implemented under their GATS (General Agreement on Trade in Services) commitments. For example, the treaty includes stronger intellectual property rights (including geographical indications), regulatory co-operation, sustainable development provisions, aims to open up public procurement, as well as specific commitments to reduce non-tariff barriers in many sectors, including cars, pharmaceuticals, and electronics. As a result, the EU-South Korea agreement is often seen as a model “second generation” trade agreement.

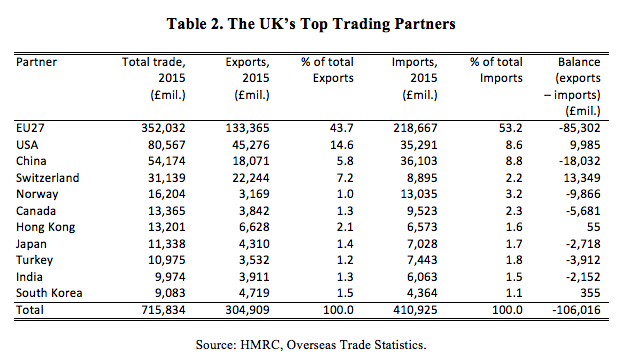

From the UK’s point of view, a comprehensive FTA with South Korea would also be attractive. As Table 2 shows, South Korea is the UK’s 11th largest trading partner (treating the EU27 as a single trade entity). In fact, South Korea is the third largest trading partner of the UK outside the EU with which the UK currently has a trade status as a member of the EU. Norway is in the single market via the European Economic Area (EEA), and Turkey is part of the EU’s Customs Union, so these two states would be covered by any FTA with the EU/EEA. The US, China, Hong Kong, Japan and India will be high on the UK’s priority list, but any negotiations with these states would need to start from scratch, whereas potential agreements with Switzerland, Canada and South Korea could start from the terms of the current EU (and hence UK) agreements with these three countries. Also, as the final column shows, the UK currently has a positive trade balance with South Korea.

Nevertheless, as Table 2 shows, the volume of UK exports and imports between the UK and any of these states is tiny compared to the current volume of trade between the UK and the EU. Hence, the overwhelming top priority for the UK must be a comprehensive trade agreement with the EU. Theresa May has tried to claim that “no deal is better than a bad deal”. But, given the dependence of UK industry and UK consumers on trade with the EU, this claim must be treated with some scepticism. For example, even if the UK could sign quick agreements with the 10 other countries in Table 2 – and this is a big “if” – this would only cover 37% of the UK’s current exports and 33% of the UK’s current imports, compared to the current 44% of exports to and 53% of imports from the EU27.

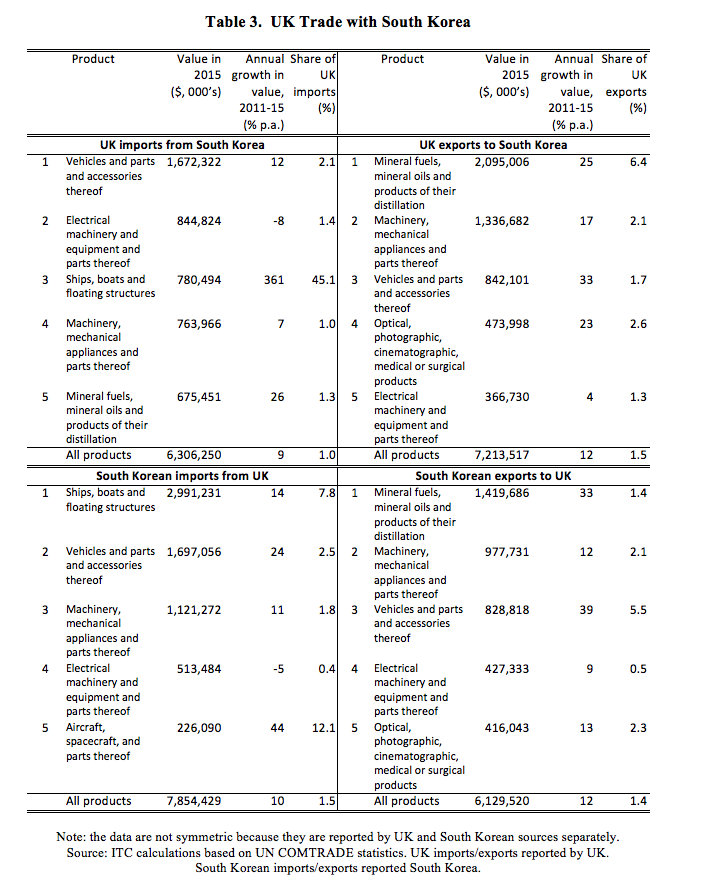

Assuming the UK could do a deal with South Korea, what would it cover? Table 3 shows the main products traded between the UK and South Korea in 2015. As the data show, the removal of tariffs has led to a significant year-on-year increase in trade in several sectors. Producers in these sectors, and consumers of these products will be eager not to reintroduce tariffs once the UK leaves the EU, and hence the current EU-South Korea FTA.

At face value, a quick cut-and-paste of the terms of the EU-South Korea FTA into a new UK-South Korea FTA seems like the simplest, least disruptive, and quickest solution. However, this is not as simple as it sounds. The precise terms of the EU-South Korea FTA were the result of a delicate compromise between a very large and powerful economy, the EU, and an economy and trading power less than one-tenth of the size of the EU. As a result, the EU had a much stronger negotiation position than Korea, and, as discussed, Korea had to make even more concessions to secure an agreement in the European Parliament. In contrast, the South Korean economy is about half the size of the UK economy. Because of this, Seoul will be reluctant to simply replicate the terms of the EU-South Korea FTA in a new UK-South Korea FTA, as South Korea will expect a more equal ‘partnership’ with an independent UK.

In addition, in many specific areas the EU-South Korea agreement goes well beyond Korea’s GATS commitments. For example, in financial services, it allows EU firms the right to offer new financial services as they will develop. It also opens telecommunications markets by reducing local ownership requirements, as well as the legal services and accountant services markets. Markets for medical, education and audio-visual services were excluded on the request of the EU. The level of market liberalisation in this area was similar to that of the US-South Korea FTA.

In terms of services trade, it will not be easy for the UK to get better terms in a future UK-South Korea FTA than the current level of liberalisation. For example, in chapter 7 of the EU-South Korea FTA, on Trade in Services, Establishment and Electronic Commerce, each party is required to extend to the other any market liberalisation that it may grant in any future FTA that it signs with another third country. This implies that South Korea cannot agree any further services market access to the UK, in a future UK-South Korea agreement, without also extending it to the EU. In addition, if South Korea extends market access to the UK, the US may demand a similar level of access under its agreement with Korea. Ever since Korea negotiated the respective FTAs with the EU and the US in parallel, the US has tried to make sure that the US obtain a similar level of market access to Korea to that granted to the EU. As a result, it is unlikely that South Korea would be willing to offer better market access to the UK than that currently granted under the EU-South Korea FTA.

One aspect of the services market is legal services. The terms of the EU-South Korea agreement in this area were almost solely for UK interests, since all of the top 50 law firms in the world are either US or UK based. The agreement allows UK law firms to set up Foreign Legal Consultant offices in Korea. Under the agreement, lawyers licensed in the UK can provide advisory services regarding the jurisdiction in which they are licensed and public international law in Korea. It also provides for cooperation and joint ventures between UK and Korean law firms in order to deal with cases in which domestic and foreign legal issues are mixed. Five EU-based law firms have opened offices in Korea under the agreement, and all 5 of these are British. If the UK leaves the EU without a new agreement with South Korea, the interests of UK law firms, and the millions of Pounds of contracts they have signed will be put in jeopardy.

Finally, and perhaps most significantly, even if the UK and South Korea could agree to apply the current terms of the EU-South Korea FTA, this would not be as beneficial for the UK once it leaves the EU. This might seem counter-intuitive, but the reason for this is because of the way “rules of origin” work in international trade. Under the EU-South Korea FTA, there are two main scenarios for a product to be considered as “originating” in the EU or South Korea. The first scenario is that it has been wholly produced in the EU or South Korea. The second is that it has been sufficiently processed in the EU or South Korea. The criteria for determining “sufficient processing” are described for each product in the product-specific rules in the text of the agreement.

For instance, for cars, base on value added, a car will be deemed to have “originated” in the EU if no more than 45% of the value of the inputs have been imported from outside South Korea or the EU to manufacture it. Under the current agreement, any product originating in the UK is counted as originating in the EU if the component parts are manufactured anywhere in the EU and South Korea (the EU and Korea mutually recognise each other’s origins when calculating rules of origin). But, once the UK leaves the EU, these components from the EU will be considered to be from outside the UK, which will mean that many UK products will not count as “originating” in the UK and so will not be covered by the terms of the deal. Currently, the percentage of UK components in British-built cars is 41% on average, which is short of meeting the required 55% of local contents under a UK-South Korea FTA that replicates the rules-of-origin in the current EU-South Korea FTA. This could mean, then, that cars manufactured in the UK would suddenly be subject to an 8% tariff when exported to Korea (which is the current WTO most-favoured-nation level), even if the UK and South Korea agree to continue to apply the current EU-South Korea agreement!

To summarise, viewed from Seoul, the prospects for a “Global Britain” can be summarised as follows:

1) The UK outside the EU will be a ‘second tier’ player when it comes to negotiating free trade agreements, considerably weaker than the ‘big three’, of the US, the EU, and China;

2) It will be easier for the UK to sign trade deals with the 53 countries with which the UK already has free trade agreements, via its current EU membership;

3) One of the countries high on this list will be South Korea, which has a very comprehensive FTA with the EU, covering services and non-tariff barriers, which has already reaped important benefits to both the UK and South Korea;

4) But, South Korea will be reluctant to replicate the terms of the EU-South Korea FTA for the UK, because it would expect a better deal with the UK than it managed to negotiate with the EU (because the EU has an economy 10 times larger than South Korea, whereas the UK economy is only twice the size of South Korea);

5) If the UK fails to reach an agreement with South Korea, this would lead to the re-imposition of tariffs on UK-South Korea trade, and would jeopardise the significant services trade that has developed between these two economies; and

6) Even if South Korea and the UK could agree to replicate the terms of the EU-South Korea agreement, the “rules of origin” in the deal could mean tariffs on many manufactured goods from the UK (such as cars) as a result of the large content of parts from elsewhere in the EU, which would count as made in a “third country” once the UK has left the EU.

In short, Global Britain does not look quite as attractive from Seoul as it might initially seem from London!

This post represents the views of the authors and not those of the Brexit blog, nor the LSE.

Simon Hix is Harold Laski Professor of Political Science, in the Department of Government at the London School of Economics and Political Science.

Hae-Won Jun is Assistant Professor, in the Institute of Foreign Affairs and National Security at the Korea National Diplomatic Academy. The views expressed in this article are those of the authors and are not to be construed as representing those of Korea National Diplomatic Academy.

The EU (in the sense of a model of European construction inaugurated by Maastricht in 1992) died along with the Brexit. It is of course a living death since its institutions are still there. The question is: what masters and what visions of Europe will these institutions now serve? There are a priori three possible answers to this question: one or more foreign power(s), hazardous coalitions of states (more or less nationalistic), the European peoples. Unless the third solution is implemented, the greatest dangers will threaten our continent. But it is most probably the second option which will characterise the year 2017… (read more in the latest GEAB bulletin / #geab.eu)

I read elsewhere that the UK is itself a signatory to the EU FTAs, alongside the EC, and that this meant that, as long as the third party agrees, it would be relatively straightforward to port the existing EU-third party FTA to become a UK-third party FTA.

Is this not correct then as you don’t mention it?

Is it actually news to anyone that the UK will not be as powerful on the world stage as the USA, EU or China? None of us expect to be do we? We just want to be free to run ourselves alongside other medium powers like Australia and Canada.

Thank you for the interesting article. Another dimension to explore is fintech and the 22 Jul/16 cooperation agreement the UK and the Republic of Korea signed. The UK is a leader in fintech and perhaps this agreement might make a FTA enticing for South Korea?

I think you are missing an important point. ‘Better’ and ‘worse’ are not absolute terms when talking about trade deals. The current EU-Korea trade deal is set up according to the interests of the 28 constituent countries which include but are not the same as the UK’s interests. A bilateral UK-Korea deal could be tweaked and tailored to our specific industries/interests. Admittedly not as simple as copy-paste of the EU agreement but I think this is what the Tories are hinting at when talking of a ‘better’ deal. Copy-paste the EU-Korea deal and amend it in places where either Korea or the UK stand to gain more (your post already mentions that Korea had to compromise for the EU deal, perhaps they won’t with us).

Hi Linda!

There are snags in the cut and paste option. Obviously 3rd parties might want to renegotiate.

But another more subtle issue is diagonal cumulation of origin. Example: As of now UK can export cars to Korea with parts made anywhere in the EU counting towards EU origin and getting preferences. If we exit EU and sign a cut-and-paste with Korea only UK value added can be counted and most UK made cars (average UK VA about 40%) will not get preferences in Korea.

And since UK VA won’t count towards EU VA, EU firms will relocate sourcing

See our blog https://blogs.sussex.ac.uk/uktpo/2017/09/27/grandfathering-ftas-and-roos/

Also where FTAs include MR of EU systems of testing and certification UK would have to find a way to guarantee its compliance.