“Europe is uninvestable,” a fund manager declares, while carving a slice of roast lamb over dinner in Mayfair, London. “With Marine Le Pen in France, Brexit and populists all over the place, we prefer to avoid any Eurozone risk.” The other fund managers in the room nod, in silence. The case for investing in Eurozone assets has never been harder to make. Equipped with sophisticated macro models but sometimes lacking confidence in the EU’s political intricacies, investors often decide to give up on Europe altogether. We haven’t.

The year 2017 indeed looks like a political minefield. Anti-euro candidates are gaining ground in the Netherlands and France, both of which have upcoming elections. The UK is about to start its split from the EU and is threatening to implement aggressive tax-cuts to counter investment uncertainty during the negotiating process. Greece’s Syriza government is again struggling to agree on a deal with creditors. Germany will hold elections too, in September, while Italy’s caretaker government is trying to kick the can down the road.

But beyond the political uncertainty, we believe there are opportunities.

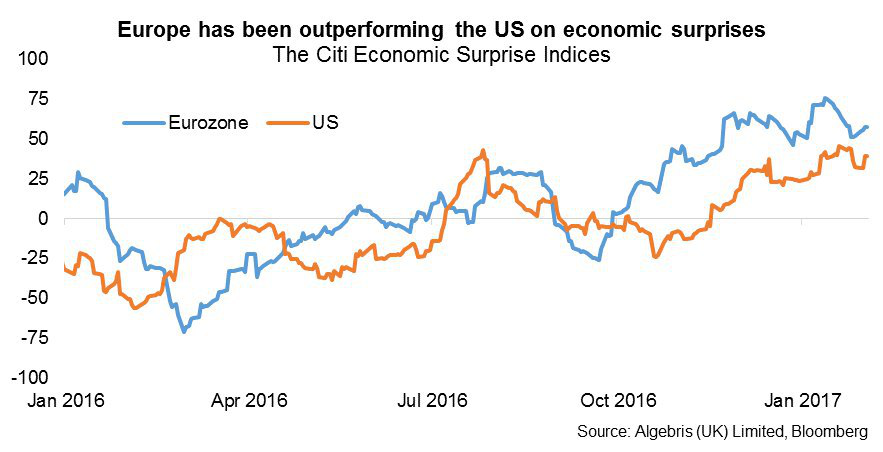

Figure 1

First, growth and inflation continue to accelerate, and in the latest indices of economic surprises – which track how economies are performing compared to predictions – Europe has been faring better than the US. While Italy, France and Portugal are lagging, other countries – including Spain and Ireland – are steaming ahead at well over 2 per cent growth. Reflating policies from the Trump administration and a stronger dollar will likely lift Eurozone exports further. Unemployment remains high at 9.7 per cent, but there are some signs of a slow reduction. Consumer confidence is rising accordingly, with more spending in cars and durable goods. Banks are starting to lend again, as we discuss below. Corporate balance sheets are healthier, with less highly levered or loss-making firms.

Figure 2

Second, there is still a potentially positive outcome for European politics. Populist candidates Geert Wilders and Le Pen have gained ground in the Netherlands and France, yet they remain head-to-head with rivals. In France, both Emmanuel Macron and François Fillon support domestic reforms and want more, not less European integration. Our estimates show a high probability of Le Pen passing the first round, but a very low probability of victory in the final round. A potential victory of Macron or Fillon over Le Pen, combined with the re-election of Angela Merkel in Germany, would create a strong pro-reform Franco-German coalition. At that point, the EU could finally focus on building stronger ties (which will be easier after the departure of Britain, always lukewarm about the European project). After elections, Germany could also abandon some of its pro-austerity rhetoric and increase domestic spending – whether for infrastructure or defence, as its allies have asked.

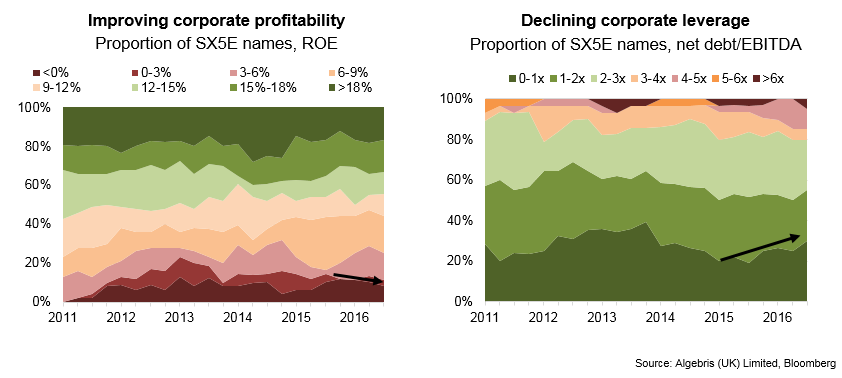

Figure 3

Third, the European Central Bank’s monetary policy stimulus is finally starting to benefit the real economy, not just financial markets.

Since last summer, the central bank started to focus on the banking system as its transmission channel for quantitative easing. This is key in Europe, where contrary to the US, banks provide three-quarters of credit to firms, and loan-funded small businesses create 80 per cent of new jobs. It means we should see a boost in lending to the real economy, which could turn into much-needed investment and job creation.

Until now, the biggest obstacle to credit transmission was the poor health of Eurozone banks, still encumbered by €1 trillion of bad loans and overblown balance sheets of around €31 trillion (which is three times the size of the economy, compared to an average of one to two times elsewhere in the world). But today banks are on the mend, having added over €260 billion of capital since 2010, and the ECB’s plan is now starting to bear fruit. Having signalled less rather than more purchases of bonds, the central bank steepened the long-end part of the yield curve, boosting profitability and equity valuations of banks, which borrow short term and lend long term. The supply of loans to non-financial firms, which had been falling for several years, is now gaining pace, and had risen by 2 per cent year-on-year in December.

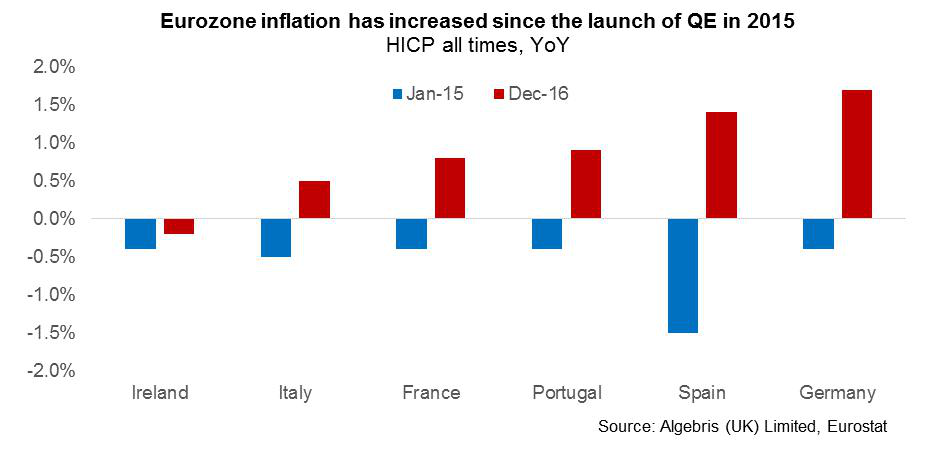

Figure 4

Despite these improvements, investors are showing Europe tough love in financial markets. European stocks cost $12.75 for every $1 of future earnings, vs nearly $16-17 in the US and Japan. German and French government bonds yields offer 1 per cent below inflation over 10 years, a negative real return, while bonds perceived as risky, like the ones issued by Greece or by banks, price in some of the highest risk premium in bond markets.

In other words, financial markets are factoring in discounts based on a near-certain scenario of high growth and inflation in the US, based on the policies set by the Trump administration, and a high chance of break-up risk in Europe. We think the future will be different.

Yes, Eurozone leaders need to draw a clearer version of their future strategy, as European Council President Tusk suggested recently. One option is a “variable-geometry” union, championed by German Finance Minister Wolfgang Schäuble. This would allow for an easier potential exit for countries like Greece or Portugal – but it would also be interpreted as a weaker, looser version of Europe. The alternative is of a stronger Europe, with more integration and a common fiscal policy – an option supported by France and Italy and by German opposition leader Martin Schulz. With the German opposition gaining in polls and the UK starting its exit process, the odds may favour consolidation, rather than variable geometry.

Whichever new strategy is chosen, Eurozone institutions still have plenty of dry powder, including the €500 billion-strong European Financial Stability fund. What’s more, citizens remain supportive of the European Union project, even in countries hard-hit by recessions: 73 per cent were either positive or neutral as of mid-2016, according to the European Commission’s Eurobarometer.

In the decades before the financial crisis, Eurozone countries lagged behind the US and the UK, held back partly by higher taxes, less flexible labour markets and more generous welfare policies. But the financial crisis taught us that this pre-crisis growth cycle built on credit, rising asset prices and stagnant productivity is neither replicable nor sustainable.

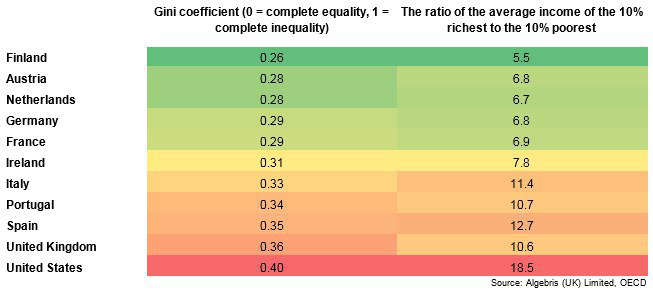

Figure 5

What is left today of this asset-rich, wage-poor model is widespread inequality, a disenfranchised generation of young people with no jobs and no assets, and rising populism. Both the US and the UK rank among the top Western countries for inequality, according to OECD data. Against this backdrop, Europe’s social safety net and its inclusive welfare policies could turn into strengths, giving it more social and political stability than investors expect; in a historical twist of events, state leaders in Germany and France have recently reminded the US of the importance of civil rights.

Many have been predicting a breakup of the Eurozone and the European Union since 2008. I believe they will be wrong again in 2017.

♣♣♣

Notes:

- This blog post appeared originally on the World Economic Forum’s Agenda.

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Madrid, by falco, under a CC0 licence

- Before commenting, please read our Comment Policy.

Alberto Gallo is portfolio manager and head of macro strategies at Algebris Investments. Before joining Algebris, Alberto set up and headed the Global Macro Credit Research team at RBS, leading idea generation across credit markets. Previously, he was a Global Credit Strategist at Goldman Sachs in New York. Prior to that, he initiated and ran the Global Credit Derivatives Strategy team at Bear Stearns.

Alberto Gallo is portfolio manager and head of macro strategies at Algebris Investments. Before joining Algebris, Alberto set up and headed the Global Macro Credit Research team at RBS, leading idea generation across credit markets. Previously, he was a Global Credit Strategist at Goldman Sachs in New York. Prior to that, he initiated and ran the Global Credit Derivatives Strategy team at Bear Stearns.