Ahead of the May 2018 interest rate decision of the Bank of England’s Monetary Policy Committee, more than two-thirds of leading economists surveyed by the Centre for Macroeconomics (CFM) agree that in a period of great uncertainty and after a prolonged period of weak real wage growth, monetary policy-makers can afford to wait for greater certainty about real wage developments and building inflationary pressures before raising interest rates. The experts are more divided on whether a strong labour market is a good indicator of building inflationary pressures: just over half agree while just under a third disagree.

Background

The May 2018 survey by the CFM and the Centre for Economic Policy Research (CEPR) asked the panel of top UK and continental European economists two questions about the labour market and monetary policy that are relevant to current policy discussions. Respondents were first asked whether they believe that in today’s economy, a strong labour market is less of a signal of growing inflation risks, as would be consistent with the recently expressed view that the Phillips curve has weakened permanently.

The second question asked whether uncertainty might allow central banks greater space to wait before raising interest rates further. Directly related to this second question, after the survey was launched, Mark Carney (Governor of the Bank of England) cast doubt on the need to raise interest rates at the next meeting of the UK’s Monetary Policy Committee (MPC). He appeared to suggest that uncertainty might support more gradual increases in interest rates than were previously expected.

Labour markets and inflation

In the UK, as in other advanced economies, the recovery in economic activity since the financial crisis has been characterised by a marked decline in unemployment, but both nominal and real wage growth have been surprisingly weak. Two reasons for this weakness, highlighted in the May 2017 CFM-CEPR survey, are the relatively weak labour protection afforded to UK workers and the weakness of productivity growth since the crisis.

Some economists have suggested that the Phillips curve – the negative relationship between inflation and unemployment – has weakened. This view would suggest that strong labour market data need not be taken as an indicator of building inflationary pressures.

There are many suggested reasons for a permanent shift in the relationship between prices and labour market activity:

- Labour market changes, such as de-unionisation, may have reduced the capacity of many workers to extract substantial wage increases even if the labour market is displaying signs of an excess of demand over supply.

- An increasingly global marketplace and openness to foreign competition may have weakened the ability of firms to raise prices and, hence, reduced their capacity to increase wages when faced with tighter domestic conditions.

- Migration may also have played a role in dampening wage growth.

- Central banks may now have become so effective at anchoring inflation expectations that they have directly weakened the relationship between the economic cycle and inflation.

- In addition to anchoring inflation expectations, the Phillips curve may appear to be flat in economies in which the central bank keeps inflation in a very narrow range (though in the UK it has moved between 0 and 5 per cent in the last ten years).

Others argue that the relationship remains relevant. Monetary policy-makers continue to expect that a tight and tightening labour market will lead to increasing pay growth above the recent subdued trends. Higher pay is then expected to knock on to higher inflation.

As Mario Draghi (President of the European Central Bank) has said, ‘As the labour market tightens and uncertainty falls, the relationship between slack and wage growth should begin reasserting itself. But we have to remain patient.’

Writing in the Financial Times, Gavyn Davies has argued that the relationship is merely hiding due to both international forces dampening inflation and the fact that headline figures may be the wrong indicators to use to assess the relationship.

Related to this debate, the first question in the latest CFM-CEPR survey asked panellists:

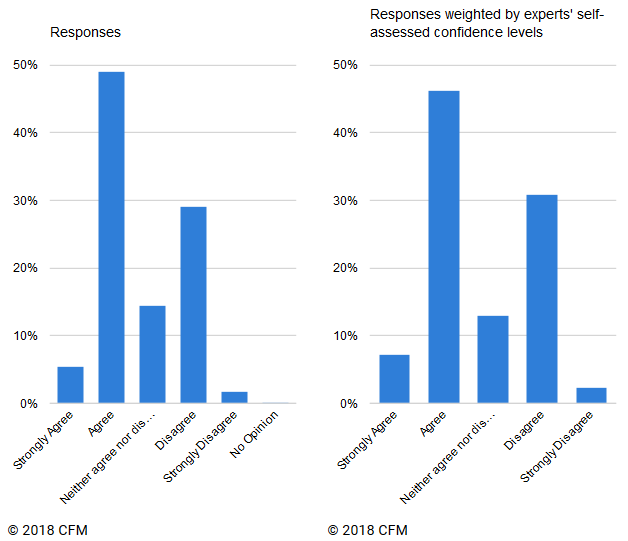

Question 1: Do you agree that a strong labour market is a good indicator of building inflationary pressure?

Fifty-five panel members answered this question. On balance, the experts agree with the statement: 55 per cent either agree or strongly agree; 31 per cent either disagree or strongly disagree; and 15 per cent neither agree nor disagree.

Some of the respondents who agree with the statement stress a continued relationship between labour market strength and inflationary pressure: as Francesco Giavazzi (IGIER, Università Bocconi) puts it, ‘The Phillips curve is still alive’.

Others argue that even though it has weakened, it remains a strong and important link. Fabien Postel-Vinay (University College London) writes that ‘The fact that Phillips curves seem to be getting flatter doesn’t necessarily imply that the inflation/labour market link has been severed.’ He points out that in a world of imperfect worker-job matching, there is slack when average match quality is low. Workers in a poor match are unlikely to be in a position to demand higher wages even if the unemployment rate is low.

Many respondents felt that the link remains between the labour market and inflation, but that it cannot necessarily be measured by the unemployment rate as in the Phillips curve. Wouter Den Haan (London School of Economics, LSE) captures this view, saying ‘A low unemployment rate may not be sufficient to talk about a “strong” labour market.’

Potential alternative labour market metrics include measures of ‘participation rates, non-standard jobs, part-time jobs’, according to Philippe Martin (Sciences Po); and ‘the number of workers that are involuntarily part-time employed or working shorter hours than they would like’, according to Stefan Gerlach (EFG Bank).

Christopher Martin (University of Bath) worries that even some alternative labour market indicators may be less useful now. He cites US evidence that the vacancy yield (the number of hires per vacancy) has fallen and rendered vacancies per unemployed worker a less reliable indicator of inflationary pressures. He hypothesises that a similar change may also have occurred in the UK.

Other respondents also emphasise that low unemployment is not a good indicator but actually disagree with the statement. They include Etienne Wasmer (Sciences Po), Panicos Demetriades (University of Leicester), Pietro Reichlin (Università LUISS G. Carli) and Sir Christopher Pissarides (LSE), who writes ‘low unemployment… is not a good indicator of inflationary pressures because in the old days the inflationary pressures originated in manufacturing and unionised workers, which have become too small a group to matter.’

Roger Farmer (University of Warwick) and Ramon Marimon (European University Institute) both disagree with the idea of the Phillips curve. Farmer argues that even the expectations-augmented Phillips curve is ‘an irrefutable theory that contains an unmeasurable concept’, and that central banks and most practicing macroeconomists are currently working with a flawed theory. Marimon thinks that ‘even with a better measure, the causality effect on “inflationary pressure” is weak theoretically and empirically.’

By contrast, Ricardo Reis (LSE) considers the link between the labour market and inflationary pressure, interpreted as capturing ‘a structural relation that encapsulates the strength of nominal rigidities, monetary non-neutrality, or deviations from the classical dichotomy’, as ‘one of the most powerful, effective, and useful pieces of applied economics’.

Monetary policy and the labour market

Notwithstanding this debate, the March 2018 report of the Office for National Statistics on UK labour market statistics (released 21 March) was received positively by financial markets. In the three months to January, employment in the UK stood at 32.25 million, which is 168,000 more than in the previous three months and 402,000 above the same period in 2017, a larger increase than markets had expected.

The unemployment rate also declined from 4.4 to 4.3 per cent in January, which reversed an unexpected rise from 4.3 to 4.4 per cent in December. Since August 2016, the unemployment rate has been below the pre-crisis value of 5.2 per cent in January 2007.

Most interest focused on the fact that we are now seeing the first signs of an impending pick-up in real wages. First, nominal wage growth rose to 2.8 per cent in the three months to the end of January, which is up from 2.5 per cent in the previous three months. Moreover, the Bank of England’s February Inflation Report cited evidence from its agent surveys that are consistent with increasing pay growth.

Second, inflation, which has been outstripping nominal wage growth for most of the last eight years, has actually shown signs of weakening. The February Consumer Prices Index (CPI) indicated that inflation has fallen to 2.7 per cent on a year earlier. This compares with 3.0 per cent in January, a fall that is a little more than was expected in the Inflation Report. Comparing the January nominal wage growth with the equivalent CPI inflation data suggests that real wages may have actually grown slightly.

These labour market data moved markets such that they have now priced in an interest rate hike with more than 90 per cent likelihood at the next MPC meeting in May. The view is that the Bank of England should further increase interest rates before wage pressures build further.

But there is also cause for some caution. In the February Inflation Report, the Bank of England highlighted that ‘Three-month regular pay growth relative to the previous three months has remained around 3 per cent on an annualised basis’. This measure has actually fallen from 3 to 2.5 per cent in the most recent release.

In addition, numerous other surveys paint a picture of stable rather than accelerating wage growth. For example, measures of expected pay for the year ahead from Confederation of British Industry surveys averaged 2.5 per cent in the second half of 2017, which is the same as the survey for the first half of 2017. And in the second half of 2017, the British Chambers of Commerce survey of the percentage balance of companies currently facing pressures to raise prices due to pay settlements was below where it was in the first half of 2017.

Finally, the most recent decline in the unemployment rate occurred despite an increase in the number of people unemployed. There was, at the same time, a more-than-offsetting increase in the labour force. This indicates that more people are actively seeking work now than recently, but it also suggests that there may be further room for increases in the labour force.

An alternative view is that the MPC can wait. There remains heightened uncertainty about the outcome of the negotiations surrounding the UK’s withdrawal from the European Union. Given the fragile nature of the recovery since the financial crisis, and especially the incredibly weak growth in real wages over the past eight years, the Bank of England can allow wage pressures to build further and to become more certain of the strength of the recovery and general conditions in the UK economy.

In November 2017, two Deputy Governors on the MPC voted against the increase in the interest rate. The MPC minutes state that they saw ‘insufficient evidence so far that domestic costs, in particular wage growth, would pick up in line with the Inflation Report’s central projection’ and that ‘recent experience suggested that wage growth could continue to be less responsive to falling unemployment than past experience would suggest.’

Motivated by this recent UK data, the second question of the CFM-CEPR survey asked about the correct response of monetary policy-makers to signs of building wage pressures in the context of a weak recovery of wages since the financial crisis and continued elevated uncertainty:

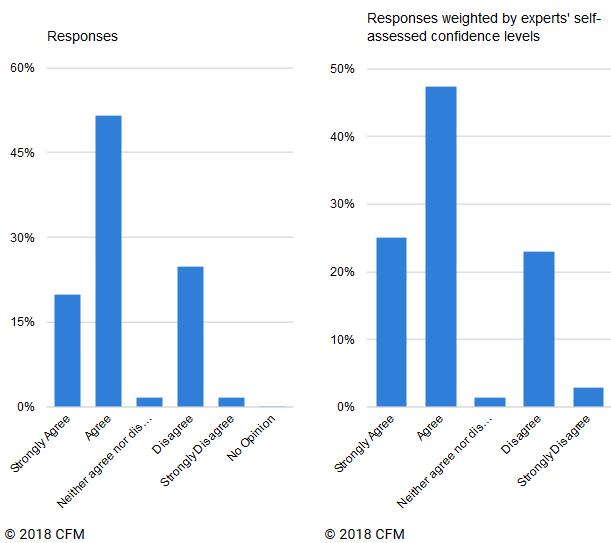

Question 2: Do you agree that in a period of great uncertainty and after a prolonged period of weak real wage growth, monetary policy-makers can afford to wait for greater certainty about real wage developments and building inflationary pressure before raising interest rates?

Sixty panel members answered this question. The experts overall agree with the statement: 71 per cent either agree or strongly agree: 27 per cent either disagree or strongly disagree; and only one respondent neither agrees nor disagrees.

David Cobham (Heriot-Watt University) would wait as he questions the underlying strength of real wage growth. Panicos Demetriades (University of Leicester) stresses the Brexit uncertainty and the fact that a good Brexit deal would actually lead to an appreciation of sterling, which will help to reduce inflationary pressures.

Tony Yates (CFM associate), Martin Ellison and Simon Wren-Lewis (both University of Oxford) all agree with the statement and argue that the downside of not raising now is small as central banks can move more aggressively once inflation starts to pick up in a more certain and sustained way.

Gianluca Benigno (LSE) thinks that there is ‘room to wait to be certain that the real wage developments are indeed consistent’. His own recent work suggests that the MPC should wait for ‘a sustained pick-up in business investment that would result in higher productivity growth’.

Costas Milas (University of Liverpool) notes that recent work suggests that ‘In the presence of elevated economic uncertainty, monetary policy tightening becomes less effective’, but he feels that waiting ‘until we have a clearer picture about the economy’ is justified.

While agreeing with the statement, Jordi Galí (CREI, Universitat Pompeu Fabra) adds a cautionary note: ‘it would be a mistake to wait too long and be forced to increase rates too rapidly.’ Ray Barrell (Brunel University London) makes the same point, but it is enough for him to dismiss the need to wait: ‘today looks less uncertain than, say 2008-09, and no worse than average’ and ‘Uncertainty is not a reason for inaction.’

Joseph Pearlman (City University London) agrees with the idea of waiting but actually sees the pressure for a rate increase coming from a Schumpeterian motive. He argues that ‘it is highly likely that we need poorly performing firms to drop out of the market, and they will only do so once their rates of return are below the interest rate.’

Concerns about asset price inflation are enough to convince Kate Barker (British Coal Staff Superannuation Scheme) and Etienne Wasmer that rates should start to rise, gradually but immediately. As Barker says, ‘we learned about the dangers from credit imbalances in the 2000s’. Fabrizio Coricelli (Paris School of Economics) also worries about the effects of expansionary policy on asset prices, as well as the possibility that credibility could be damaged by waiting.

Ethan Ilzetzki (LSE) feels that inflationary pressure is enough to warrant a gradual approach to interest rate increases. Jagjit Chadha (National Institute of Economic and Social Research) stresses that ‘Rates could be raised a number of times in small increments and still be providing a monetary stimulus.’ Patrick Minford (Cardiff Business School) argues that monetary policy needs to come out of crisis-mode monetary policy and so sees ‘raising rates and reducing QE [quantitative easing]’ as necessary.

♣♣♣

Notes:

- This blog post is based on Labour Markets and Monetary Policy, a survey of the Centre for Macroeconomics (CFM).

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Borough Market, by Marinebugs, under a CC-BY-NC-SA-2.0 licence

- When you leave a comment, you’re agreeing to our Comment Policy

Wouter Den Haan is Professor of Economics at LSE and Co-Director of the Centre for Macroeconomics. HIs main research interests are in macroeconomics, the role of frictions in financial and labour markets for business cycles, business cycle models with heterogeneous agents and computational economics. He holds a PhD in Economics from Carnegie Mellon University.

Wouter Den Haan is Professor of Economics at LSE and Co-Director of the Centre for Macroeconomics. HIs main research interests are in macroeconomics, the role of frictions in financial and labour markets for business cycles, business cycle models with heterogeneous agents and computational economics. He holds a PhD in Economics from Carnegie Mellon University.

Ethan Ilzetzki is Assistant Professor of Economics at LSE. He is an Associate at the Centre for Macroeconomics and the Centre for Economic Performance. His research interests are in macroeconomics, international finance and fiscal policy. He holds a PhD in Economics from the University of Maryland.

Ethan Ilzetzki is Assistant Professor of Economics at LSE. He is an Associate at the Centre for Macroeconomics and the Centre for Economic Performance. His research interests are in macroeconomics, international finance and fiscal policy. He holds a PhD in Economics from the University of Maryland.

Martin Ellison is Professor of economics at the University of Oxford and a Fellow of Nuffield College. He gained his PhD in economics in 2001 from the European University Institute in Florence. Ellison has worked as a consultant for the Bank of England and as a Professor at the University of Warwick before his current affiliation at the University of Oxford. He is specializing in macroeconomics; his PhD thesis was titled “Money Matters: Four Essays on Monetary Economics”. His main research interest is monetary policy and he is editing several journals in the field of economics.

Martin Ellison is Professor of economics at the University of Oxford and a Fellow of Nuffield College. He gained his PhD in economics in 2001 from the European University Institute in Florence. Ellison has worked as a consultant for the Bank of England and as a Professor at the University of Warwick before his current affiliation at the University of Oxford. He is specializing in macroeconomics; his PhD thesis was titled “Money Matters: Four Essays on Monetary Economics”. His main research interest is monetary policy and he is editing several journals in the field of economics.

Michael McMahon is Associate Professor of Economics at Warwick University. He is also a a Research Associate with the Centre for Macroeconomics (CFM), Research Affiliate with the Centre for Economic Policy Research (CEPR) and the Centre for Applied Macroeconomic Analysis (CAMA, ANU), International Consultant Economist at the IMF’s Singapore Training Institute and a Visiting Scholar at the Bank of England. He holds a PhD in Economics from LSE. Dr. McMahon’s research interests are macroeconomics of business cycles; monetary economics; inventories and applied econometrics.

Michael McMahon is Associate Professor of Economics at Warwick University. He is also a a Research Associate with the Centre for Macroeconomics (CFM), Research Affiliate with the Centre for Economic Policy Research (CEPR) and the Centre for Applied Macroeconomic Analysis (CAMA, ANU), International Consultant Economist at the IMF’s Singapore Training Institute and a Visiting Scholar at the Bank of England. He holds a PhD in Economics from LSE. Dr. McMahon’s research interests are macroeconomics of business cycles; monetary economics; inventories and applied econometrics.

Ricardo Reis is Professor of Economics at LSE, on leave from Columbia University. He received his PhD in Economics from Harvard University in 2004. He has published extensively and has had a number of editorial positions in leading academic journals. He is a Research Associate at CFM and NBER, a Research Fellow at the Centre for Economic Policy Research, and is also a member of NBER’s Macro Annual advisory board. Dr Reis is an academic consultant of the Federal Reserve Board of New York and Richmond.

Ricardo Reis is Professor of Economics at LSE, on leave from Columbia University. He received his PhD in Economics from Harvard University in 2004. He has published extensively and has had a number of editorial positions in leading academic journals. He is a Research Associate at CFM and NBER, a Research Fellow at the Centre for Economic Policy Research, and is also a member of NBER’s Macro Annual advisory board. Dr Reis is an academic consultant of the Federal Reserve Board of New York and Richmond.