Talented individuals are often excluded from leadership positions if they belong to a group that faces discrimination. Such discrimination is, of course, extremely hurtful and unfair to the individuals. But is it also costly in a more general sense?

In particular, do corporations become less profitable when they adopt discriminatory attitudes and exclude highly qualified individuals from leadership roles? How much do entire economies suffer when governments enact discriminatory policies against certain groups?

Recent political events have underscored the importance of these questions. For example, the American travel ban on citizens of several Muslim-majority countries raised fears among US corporations (including Amazon, Nike and MasterCard) that increasing discrimination will leave them unable to recruit and retain talent. In Turkey, several thousand executives who follow the cleric Fethullah Gülen have been arrested or have fled overseas since 2016, fuelling concerns of an economic collapse.

History is rich with examples of such discrimination. For example, the US government gave in to ‘race prejudice’ and forcibly interned Japanese-Americans during the Second World War. The entrepreneurial Huguenots had to flee seventeenth century France due to religious persecution. The economic costs of discrimination are also important if we want to assess the benefits of government policies that help discriminated groups to break the ‘glass ceiling’ to reach leadership positions.

Despite the importance of the issue, we currently have little evidence on how costly discrimination against highly qualified individuals in leading positions can be. Our research breaks new ground by measuring the economic losses caused by such discrimination.

Specifically, we analyse discrimination against senior managers with Jewish origins in Nazi Germany. Using this unique setting and new data on individual managers and corporations, we study how the share prices and profitability of firms evolved when the Jewish managers were removed from the German economy due to rising anti-Semitism.

The exclusion of Jewish managers from firms in Nazi Germany

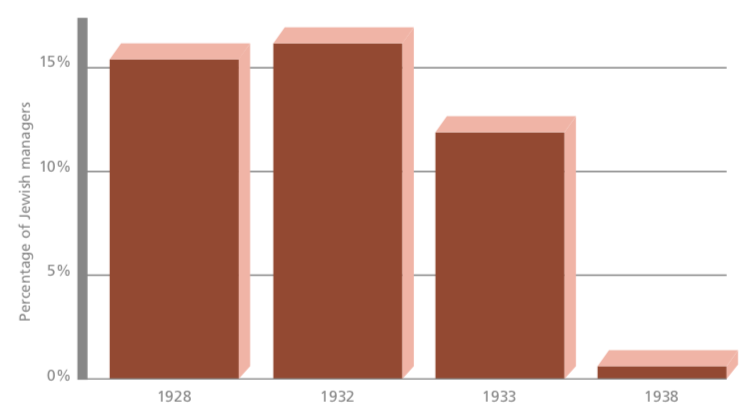

We collect new data on almost 30,000 managerial positions in German firms listed on the Berlin Stock Exchange. Managers of Jewish origin (either practicing Jews or Christians with a Jewish ancestor) held around 15 per cent of senior management positions in 1928 and 1932 (see Figure 1).

After the Nazis gained power on 30 January 1933, discrimination against Jews became commonplace in Germany. Many firms voluntarily dismissed managers of Jewish origin or were coerced into removing them by Nazi officials. Deutsche Bank, for example, forced chief executive Oscar Wassermann and executive board member Theodor Frank to resign their positions by 1 June 1933. By 1938, virtually no Jewish managers remained in firms listed in Berlin.

Oscar Wasserman, photo by

Oscar Wasserman, photo by

We analyse firms that had employed Jewish managers in 1932 and lost them after the Nazis took power. Many firms that the public did not perceive to be ‘Jewish’ happened to employ managers of Jewish origin (such as Allianz, BMW, Daimler-Benz and IG Farben). We compare these firms to other firms that had not employed any managers of Jewish origin and, therefore, remained unscathed by the removal of Jewish managers due to the Nazi ideology.

The effects on the characteristics of firms’ senior management

In our first set of results, we show that losing the Jewish managers changed the observable characteristics of senior managers at firms that had employed Jewish managers in 1932. The number of managers with managerial experience and university degrees, and the total number of connections to other firms (measured by seats on other supervisory boards) fell significantly.

The effects on all management characteristics persisted at least until the end of our sample period in 1938.

Figure 1. Percentage of Jewish managers over time

Notes: The figure reports the percentage of senior management positions that were held by Jewish managers in firms listed on the Berlin Stock Exchange.

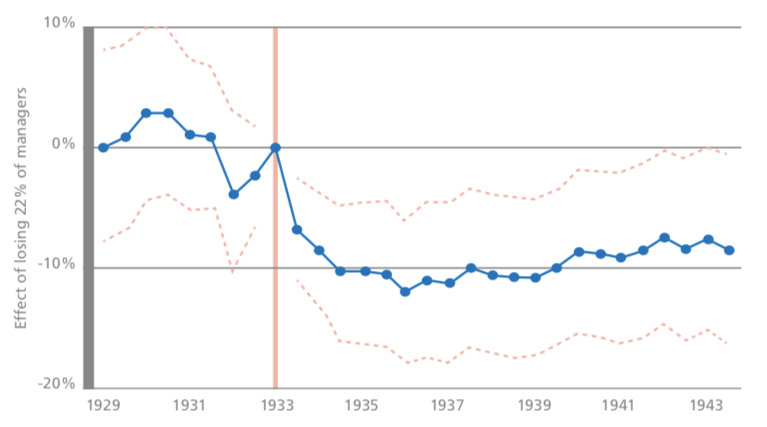

The effect on share prices

In our second set of results, we show that the share prices of firms with Jewish managers fell sharply after the Nazis grabbed power in 1933, when the Jewish managers started to leave their firms (see Figure 2). These losses persisted until the end of the share price sample period in 1943, ten years after the Nazis had gained power. The share price of the average firm that had employed Jewish managers in 1932 (where 22 per cent of managers had been of Jewish origin) declined by about 12 per cent after 1933, relative to a firm without Jewish managers in 1932.

It is striking that our estimated short- run effect of losing Jewish managers is close to the initial share price responses to the exits of prominent managers in recent times. For example, after Apple chief executive Steve Jobs took permanent medical leave in 2011, his company’s shares fell by 6 per cent. When Fiat Chrysler chief executive Sergio Marchionne stepped down due to surgery in 2018, the company’s shares lost 5 per cent.

Our data allow us to investigate the channels through which the loss of the Jewish managers affected share prices. Share prices declined only for firms where the removal of the Jewish managers led to large losses in the number of university-educated managers and managerial connections (measured by seats on other supervisory boards). Share prices did not fall significantly when the removal of the Jewish managers hardly affected these two measures.

The effect on dividends and returns on assets

In our third set of results, we analyse the effects of losing Jewish managers on two additional measures of firm performance: dividend payments and returns on assets. We find that after 1933, dividend payments fell by approximately 7.5 per cent for the average firm with Jewish managers in 1932 (which lost 22 per cent of its managers). We also find that after 1933, the average firm that had employed Jewish managers in 1932 experienced a decline in its return on assets by 4.1 percentage points. These results indicate that the loss of Jewish managers also led to real losses in firm efficiency and profitability.

Aggregate implications and conclusion

Our findings inform our understanding of how the rise of a discriminatory ideology can cause real economic harm. A back- of-the-envelope calculation suggests that excluding the Jewish managers reduced the aggregate market valuation of firms listed in Berlin by 1.8 per cent of German gross national product, a first-order economic loss.

Arguably, our study focuses on the most severe form of discrimination against a particular group of individuals, but even less severe forms of discrimination can lead to a loss of talent. As highlighted above, the US travel ban and the persecution of Turkish executives are current examples of rising discrimination that are likely to affect firms.

Even the perception of not being welcome in a country may lead to the outflow of high-skilled individuals. For example, there are many reports of highly paid continental Europeans planning to leave the UK in the coming years as a consequence of Brexit. The results in our study indicate that such an exodus could significantly hurt firms and the economy.

Figure 2. The effect of losing Jewish managers on share prices

Notes: The blue dots show the effect of losing Jewish managers for the average firm with Jewish managers, relative to a firm without Jewish managers. The average firm with Jewish managers lost 22% of its managers after 1933. The pink, broken lines represent 95% confidence intervals.

♣♣♣

Notes:

- This blog post appeared originally on CentrePiece, the magazine of LSE’s Centre for Economic Performance (CEP). It summarises ‘Discrimination, Managers, and Firm Performance: Evidence from “Aryanizations” in Nazi Germany’ CEP Discussion Paper No. 1599

- The post gives the views of its authosr, not the position of LSE Business Review or the London School of Economics.

- Featured image courtesy of DesignRaphael Ltd. NOT under Creative Commons. All rights reserved.

- When you leave a comment, you’re agreeing to our Comment Policy.

Kilian Huber is a research fellow at the Becker Friedman Institute, University of Chicago. In 2019 he will be an assistant professor of economics at the Booth School of Business, University of Chicago. He is a research associate in CEP’s labour markets programme.

Kilian Huber is a research fellow at the Becker Friedman Institute, University of Chicago. In 2019 he will be an assistant professor of economics at the Booth School of Business, University of Chicago. He is a research associate in CEP’s labour markets programme.

Volker Lindenthal is a postdoctoral researcher at the Ludwig Maximilian University of Munich. Previously he worked as postdoctoral researcher at the University of Freiburg. Volker holds a PhD in economics and finance from Bocconi University in Milan. His research interests are in labour economics and economic history.

Volker Lindenthal is a postdoctoral researcher at the Ludwig Maximilian University of Munich. Previously he worked as postdoctoral researcher at the University of Freiburg. Volker holds a PhD in economics and finance from Bocconi University in Milan. His research interests are in labour economics and economic history.

Fabian Waldinger teaches economics at the University of Munich. He was previously associate professor of management at LSE. His research interests are the economics of innovation, economic history, and labour economics.

Fabian Waldinger teaches economics at the University of Munich. He was previously associate professor of management at LSE. His research interests are the economics of innovation, economic history, and labour economics.