Over the last three decades, euro area countries have experienced profound economic, financial and institutional changes, plus diverse shocks. Growth has been volatile, and almost missing, in some countries. In this study we have assembled a rich panel to find which factors might have played a role in stirring growth, and/or reducing it in the short and long run.

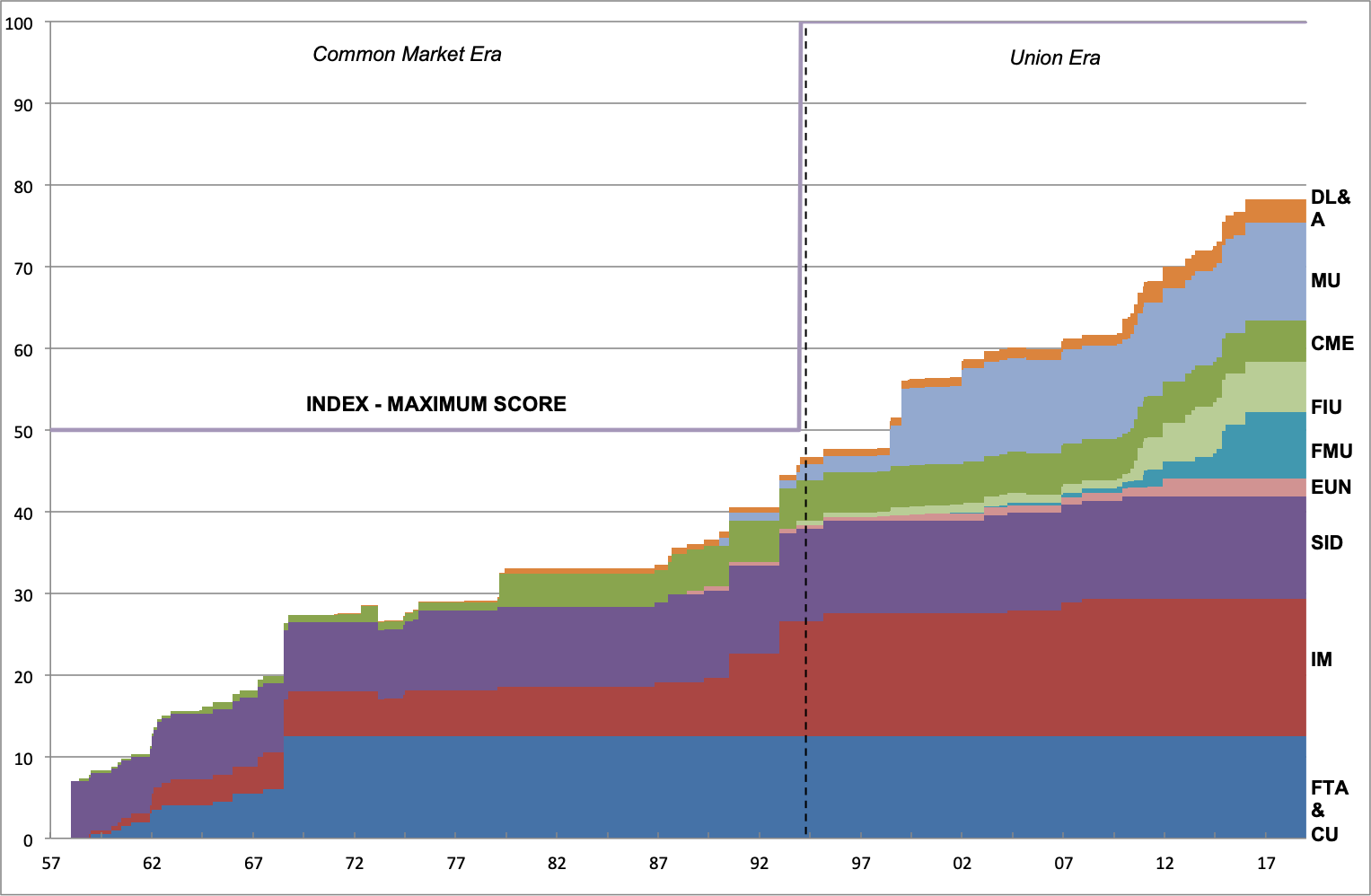

We assemble a large set of real, financial, monetary and institutional variables covering the period between the first quarter of 1990 and the fourth quarter of 2016 for euro area countries. Each of these blocks contains diverse variables. We also make use of an index of EU Institutional Integration (EURII) (Fig. 1). This, we believe, might have been impactful in the last decades, contributing to an increase in trade, investments, capital and labour mobility and innovation, and helping the overall convergence within members. This approach is a novelty in the growth literature, which normally focuses on determinants largely based on the classic Solow exogenous growth model (Solow, 1956) or on the endogenous growth theory pioneered by Romer (1990). Our aim and main contribution is to provide an a-theoretical toolkit looking at the “usual suspects” in the policy debate, but rather “unusual” in the academic literature, as possible factors behind fluctuations and differences in growth rates among euro area countries since 1990.

Figure 1. The EURII index

Source: Authors’ updated series from Dorrucci et al. (2015). Free trade area (FTA) and customs union (CU), Internal market (IM), Co-ordination of monetary and exchange rate policies (CME), Supranational institutions and decision-making (SID), Economic Union (EUN), Financial Markets Union (FMU), Fiscal Union (FIU), Monetary Union (MU), Democratic legitimacy and accountability (DL&A).

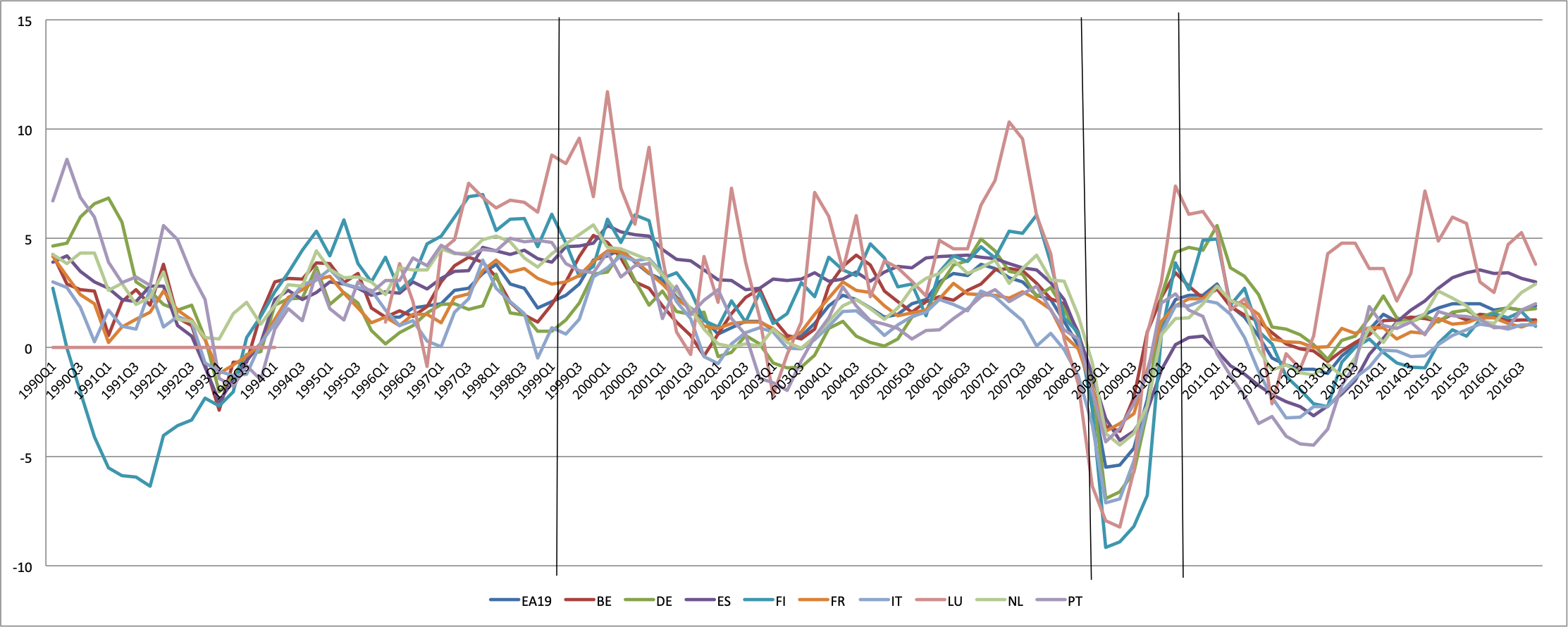

We also look at two sub-groups of euro area countries, defined as euro area “core” (Belgium, Germany, Finland, France, Luxembourg and the Netherlands) and “periphery” (Spain, Italy and Portugal). The core countries exhibited high growth rates before the launch of the euro. Later on, GDP growth in the euro area core recovered faster and then stabilised at around 2 per cent. Within the periphery group, Italy exhibited stagnating GDP growth since the beginning of the 90s and the weakest recovery after the global financial crisis and the sovereign crisis (Papadia, 2017). Spain, on the other hand, had a boom period lasting a decade, from the mid-90s to the mid-00s fuelled by reforms and an increase in the magnitude of the credit cycle (Comunale, 2017). Overall, the drop-in growth for the periphery was less substantial during 2008-2009. Only after 2014 we can see a further increasing growth trend for the periphery as well. We expect therefore differences in the changes of growth rates (Fig. 2) and in their volatilities over time.

Figure 2. Growth rates of considered euro area countries and EA 19

Source: Eurostat, IMF IFS and authors’ calculations. These are the real growth rate compared to the same quarter of previous year. The vertical lines are for the introduction of the euro and the starting of the sovereign debt crisis and the starting of the recovery/low inflation period.

Given these heterogeneities, we make use of several techniques to select the relevant factors, which may have influenced growth based on the events and situations mentioned above. The Weighted-Average Least Squares (WALS) is a statistical method by Magnus et al. (2010) and Magnus and De Luca (2016) which provides us with clues about the variables to select. Then we apply a heterogeneous panel Error Correction Model (ECM) to quantify their contributions to growth in the short and long run (more details in Comunale and Mongelli, 2019 forthcoming).

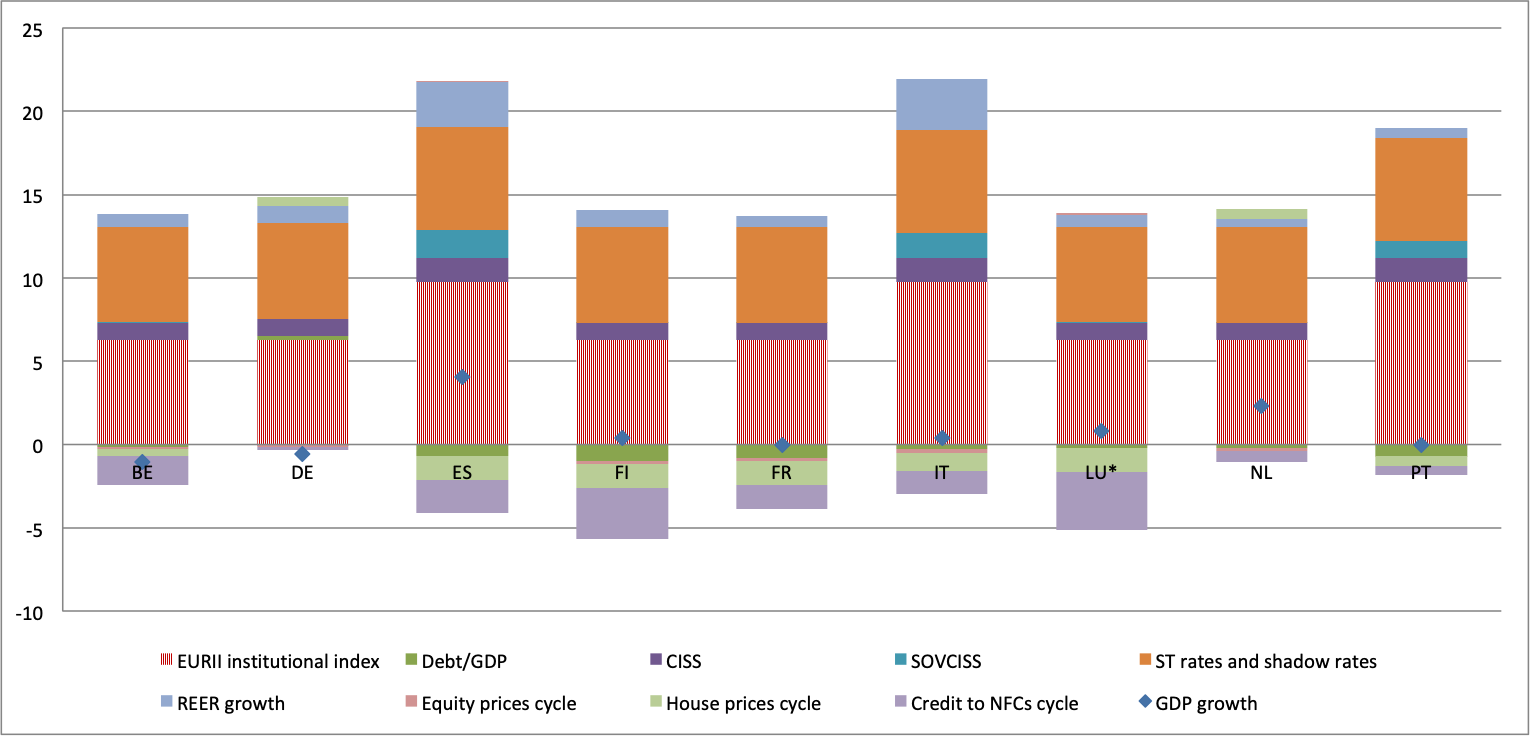

Our main finding is that further institutional integration at EU level supports long-run growth for all countries, and in particular, in the periphery. This finding is robust across specifications and setups: a fact for which there might be diverse complementary explanations. One possible explanation might be a rising confidence in the evolving European governance and institutional framework. Another explanation might lie in a convergence of policy preferences and lesser policy activism, and greater financial stability (until the sovereign crisis!). The contribution is bigger in magnitude in the first period, given the major advancement in EMU design between the 90s and the 2000s (Fig. 3), however the positive contribution for an increase in GDP growth is evident also after the sovereign debt crisis (Fig. 4). If we further split our institutional index in its components, we see a big and significant positive role for financial and political integration, while economic and financial integration are ineffective in boosting growth. Deeper financial integration seems to have beneficial effects on the core only, while it is not significant in the periphery. The opposite holds for political integration, as an increase in the latter boosts long-run growth only for the periphery.

Figure 3. Contribution of factors to growth up to 2009

Source: Authors’ calculations. The REER growth has been recalculated here to the reader convenience and an increase means a better competitiveness performance.

Figure 4. Contribution of factors to growth from 2010 onwards

Source: Authors’ calculations. The REER growth has been recalculated here to the reader convenience and an increase means a better competitiveness performance.

We also find that an improvement in competitiveness matters for sustained growth in the long-run. A decline in systemic stress is also associated with growth. An increase in global GDP is also positive for growth, generally in the medium run. The debt over GDP has a negative influence for the periphery but only in the short run. Surprisingly, the deficit plays no role. Instead, higher sovereign stress is associated with lower growth. Prior to the zero lower bound, higher monetary policy rates are associated with growth. These relations turn past the zero lower bound and when using the shadow rate that capture exceptional standard and non-standard monetary policies. The equity price cycle affects positively GDP growth only pre-crisis and only in the very short-run, while the loans to non-financial corporations (NFCs) had a positive impact for core euro area.

♣♣♣

Notes:

- This blog post is based on the authors’ chapter which is forthcoming in N. Campos, P. De Grauwe and Y. Ji (eds.), Structural Reforms and Economic Growth in Europe, Cambridge University Press.

- The post gives the views of its authors, not the position of the Bank of Lithuania, the ECB, ESCB, LSE Business Review or the London School of Economics.

- Featured image by vdugrain, under a Pixabay licence

- Before commenting, please read our Comment Policy

Mariarosaria Comunale is principal economist at the Bank of Lithuania, in the applied macroeconomic research division, economics department. Recently she was a visiting researcher at the Oesterreichische Nationalbank and economist at the European Central Bank in the directorate general, international and European relations. Her main area of research pertains to applied international macroeconomics, for analysis on EU integration, growth, macroeconomic imbalances, financial cycles and exchange rate pass-through.

Mariarosaria Comunale is principal economist at the Bank of Lithuania, in the applied macroeconomic research division, economics department. Recently she was a visiting researcher at the Oesterreichische Nationalbank and economist at the European Central Bank in the directorate general, international and European relations. Her main area of research pertains to applied international macroeconomics, for analysis on EU integration, growth, macroeconomic imbalances, financial cycles and exchange rate pass-through.

Francesco Paolo Mongelli is a senior adviser at the European Central Bank’s directorate general, monetary policy, and honorary professor at the Johann Wolfgang Goethe University of Frankfurt. He holds a BA in economics from the Free University for Social Studies (LUISS) in Rome, and also a master’s degree and a Ph.D. in economics from Johns Hopkins University, Baltimore. He has worked at the ECB since 1998. Prior to that, he spent several years as an economist at the International Monetary Fund in Washington. He also teaches economics of monetary unions, and central banking and monetary union.

Francesco Paolo Mongelli is a senior adviser at the European Central Bank’s directorate general, monetary policy, and honorary professor at the Johann Wolfgang Goethe University of Frankfurt. He holds a BA in economics from the Free University for Social Studies (LUISS) in Rome, and also a master’s degree and a Ph.D. in economics from Johns Hopkins University, Baltimore. He has worked at the ECB since 1998. Prior to that, he spent several years as an economist at the International Monetary Fund in Washington. He also teaches economics of monetary unions, and central banking and monetary union.