In the Covid-19 crisis, many businesses are rapidly running out of cash. In our earlier blog we reported that in the United States half of small firms – those with less than 500 employees – have cash reserves for less than a month. Restaurants, for example, have only 16 days of cash on hand.

Firms in rich countries are not alone in facing liquidity problems. Our analysis of twelve high-income and middle-income economies (Colombia, Greece, Italy, Jordan, Kazakhstan, Kenya, Morocco, Peru, Portugal, Russia, Turkey, and Ukraine) shows that in a hypothetical scenario where firms have no revenues due to a lockdown or collapsed demand, the median firm has retained earnings and other sources of financing to last 8 (in retail) to 19 weeks (in other manufacturing).

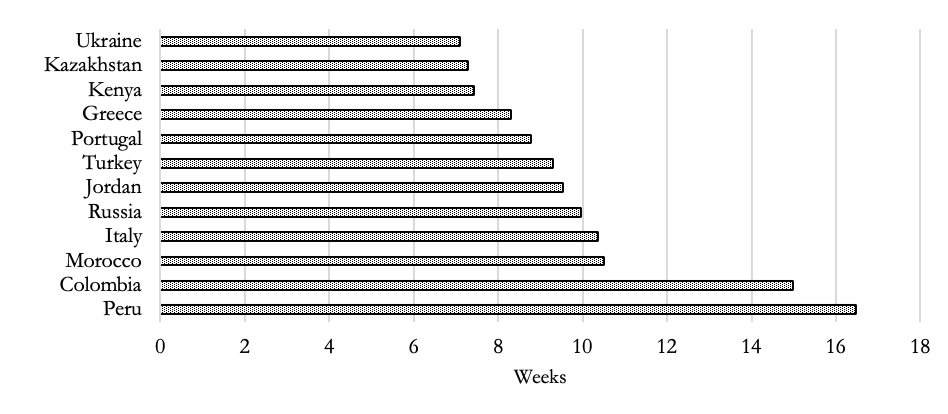

Across all countries, the median Ukrainian firm is the most liquidity constrained, while the median Peruvian firm has the most breathing space. The former has a seven weeks’ buffer in retained earnings and other sources of financing, the latter 16 weeks.

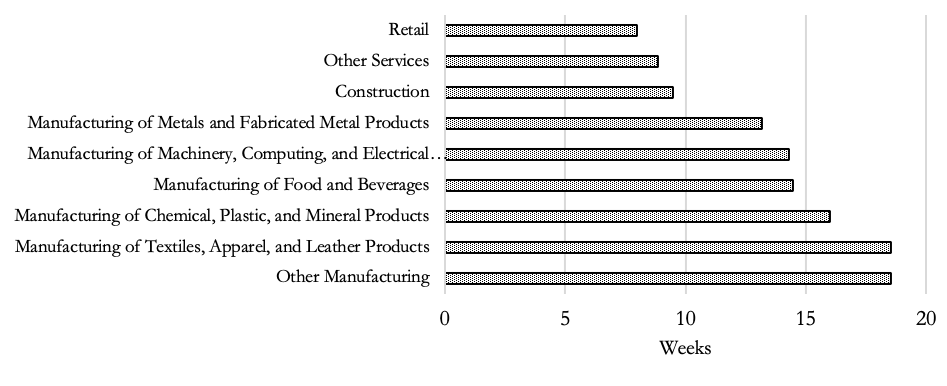

Retailers have the shortest survival time in this hypothetical scenario, whereby the median business runs out of savings in about eight weeks of no revenues (Figure 1). The median firm in the construction sector has liquidity to last nine weeks, while firms in the manufacturing of chemical, plastics and mineral products can last 16 weeks.

Figure 1. Median survival time based on fixed costs by sector

Note: Data is extracted from the World Bank Enterprise Surveys. Number of observations: 6,345.

Figure 2 shows the median survival time by country, which ranges between 7 (Ukraine) and 16 weeks (Peru). Kazakh and Kenyan firms are as cash-constrained as Ukrainian firms (also at 7 weeks) and have a survival time that is less than half that of the median Colombian firm (15 weeks). The median business in Italy, Jordan, and the Russian Federation can last ten weeks, one week longer than the median business in Portugal and Turkey (nine weeks).

Figure 2. Median survival time based on fixed costs by country

Note: Data is extracted from the World Bank Enterprise Surveys. Number of observations: 6,345.

The median survival time has significant variation across countries within a given sector. The median Portuguese firm in the manufacturing of food and beverages, for example, has a survival time of 7.6 weeks, whereas the median firm in the same sector in Colombia can last 26.3 weeks. Variation in this hypothetical scenario is even larger in the manufacturing of metals and fabricated metal products. The median Ukrainian firm can survive for just a little over eight weeks, while the median Turkish firm has sufficient liquidity for more than ten months (44.1 weeks). Great variation is also present across sectors within a given country. In Kenya, for example, the median firm in the manufacturing of chemical, plastic and mineral products cannot even last a week, while a firm in the manufacturing of food and beverages can last for 16.8 weeks.

We next test two hypotheses: either economic distress periods like the Covid-19 crisis are associated with an exit of inefficient firms or with a mass exit of firms due to collapsed demand and increased uncertainty. We find evidence for the latter. There is no association between size of firms, their age, their productivity and their survival times in the twelve-country sample.

In the analysis by country, larger firms have longer survival times in Colombia. In Kenya, larger, older and higher productivity firms have longer survival times. In Greece and Peru, high productivity firms also have higher survival times. As regards firms’ age, there is a positive correlation with survival times in Jordan and Morocco, but negative in Kazakhstan.

Governments everywhere have already done a lot to keep the economy going, while dealing with the health crisis. The evidence here suggests that efforts have to be redoubled.

Recent posts by Erica Bosio and Simeon Djankov:

♣♣♣

Notes:

- This blog post expresses the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by Wounds_and_Cracks, under a Pixabay licence

- When you leave a comment, you’re agreeing to our Comment Policy

Erica Bosio is a researcher at the World Bank Group, where her work focuses on public procurement. Previously, she worked in the arbitration and litigation department of Cleary Gottlieb Steen & Hamilton in Milan. She holds a Master of Laws from Georgetown University and a degree in law from the University of Turin (Italy).

Erica Bosio is a researcher at the World Bank Group, where her work focuses on public procurement. Previously, she worked in the arbitration and litigation department of Cleary Gottlieb Steen & Hamilton in Milan. She holds a Master of Laws from Georgetown University and a degree in law from the University of Turin (Italy).

Simeon Djankov is policy director of the Financial Markets Group at LSE and a senior fellow at the Peterson Institute for International Economics (PIIE). He was deputy prime minister and minister of finance of Bulgaria from 2009 to 2013. Prior to his cabinet appointment, Djankov was chief economist of the finance and private sector vice presidency of the World Bank. He is the founder of the World Bank’s Doing Business project. He is author of Inside the Euro Crisis: An Eyewitness Account (2014) and principal author of the World Development Report 2002. He is also co-editor of The Great Rebirth: Lessons from the Victory of Capitalism over Communism (2014).

Simeon Djankov is policy director of the Financial Markets Group at LSE and a senior fellow at the Peterson Institute for International Economics (PIIE). He was deputy prime minister and minister of finance of Bulgaria from 2009 to 2013. Prior to his cabinet appointment, Djankov was chief economist of the finance and private sector vice presidency of the World Bank. He is the founder of the World Bank’s Doing Business project. He is author of Inside the Euro Crisis: An Eyewitness Account (2014) and principal author of the World Development Report 2002. He is also co-editor of The Great Rebirth: Lessons from the Victory of Capitalism over Communism (2014).

True – efforts have to be redoubled, if not trebled. Otherwise, instead of leading to a painful few months, the damage could be much longer-lasting. Very useful findings!